DEFENSIVE

40% equity · 50% bonds · 10% cash

$38,304

−$3,696 · −8.8%

Private banking gives the top 1% elite risk planning, liquidity stress testing, and fiduciary discipline. The remaining 99% are handed cold budgeting apps and opaque robo-advisors. Aureus is a B2C experiment in translating institutional rigour into a wealth-building engine for everyday consumers — keeping the fiduciary sign-off in the user's hands while the AI carries the analyst load.

Aureus translates UHNW private-banking fiduciary logic into a B2C mobile experience. Four AI modules, 31 screens, a working prototype. The thesis: the retail-fintech category serves users who are anxious about spending — Aureus serves the user who has stopped being anxious and is now asking for fiduciary-grade tools.

What's built (concept)

What's deliberately not built

Status & honesty disclosure

Prefer YouTube? Watch it there ↗

UHNW clients of J.P. Morgan Private Bank, UBS Wealth, and Pictet receive personalised risk modelling, liquidity stress tests, multi-generational tax planning, and a relationship manager who absorbs the complexity. The retail investor receives a budgeting app that scolds them for buying coffee, or a robo-advisor that optimises a black-box portfolio they cannot see inside. The structural gap is not the asset class — it's the fiduciary logic. Aureus closes that gap.

01

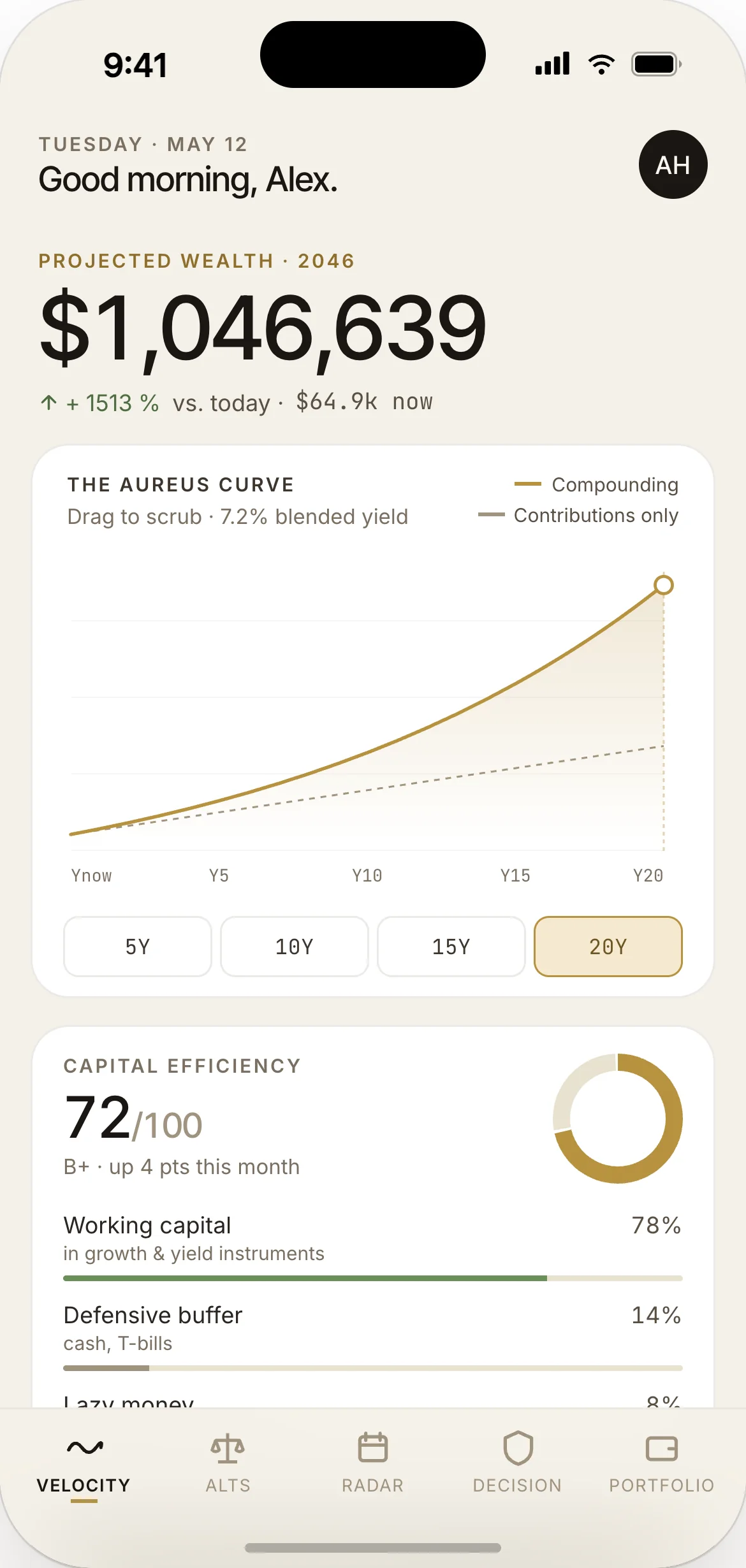

Traditional retail apps surface the static balance — what is in the account right now. Aureus surfaces capital velocity and the compounding engine — how fast that capital is growing, and where it will be in ten or twenty years if the current behaviour persists. Static balance is a savings-account metaphor. Capital velocity is a private-banker's metaphor.

02

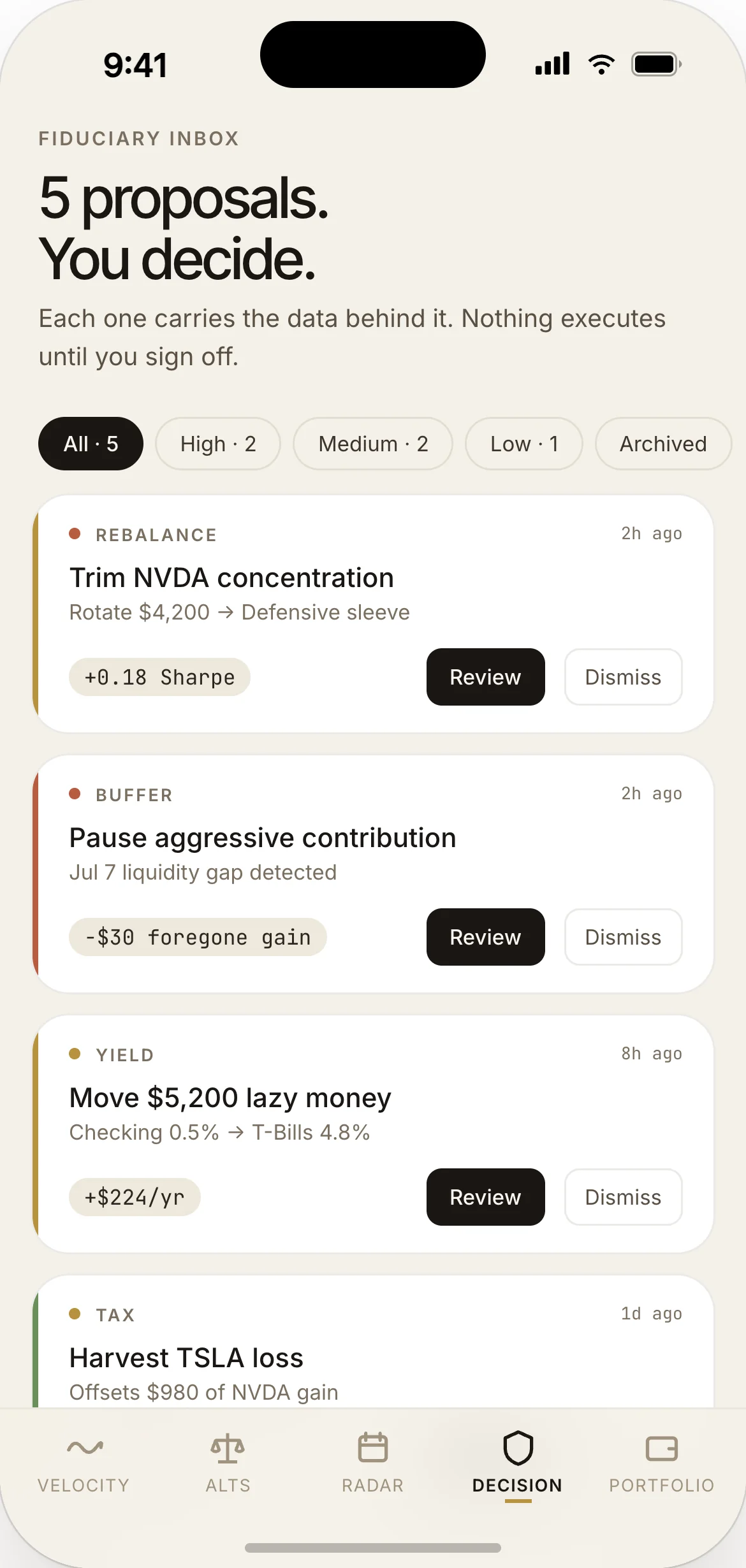

The AI does not execute trades autonomously. It acts as an objective analyst — surfacing data, identifying liquidity gaps, generating probabilistic forecasts, presenting three named scenarios with worst-case drawdowns. The fiduciary sign-off always stays with the user. This extends the compliance-and-control principles I designed at ACY Securities into the retail surface where most products give them up.

03

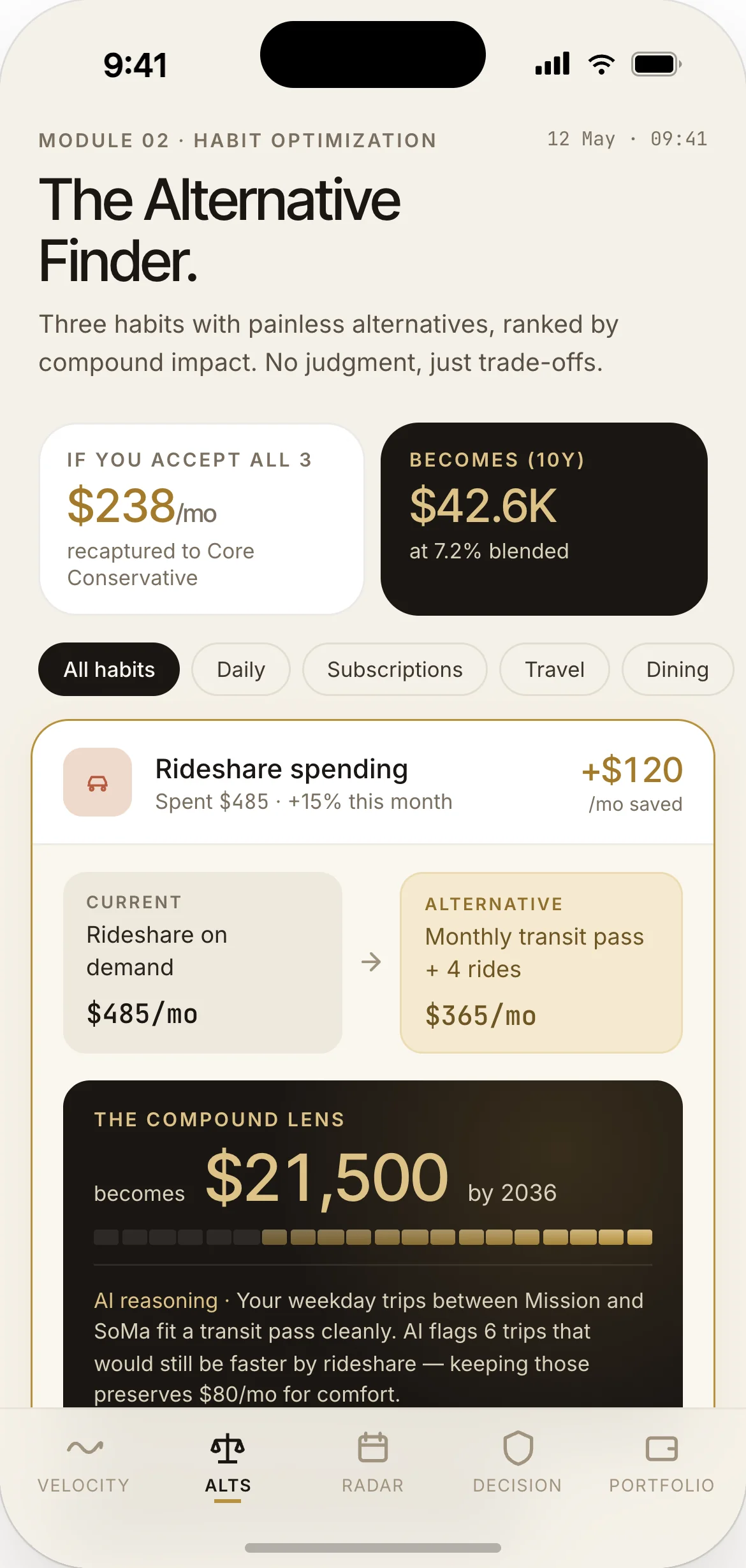

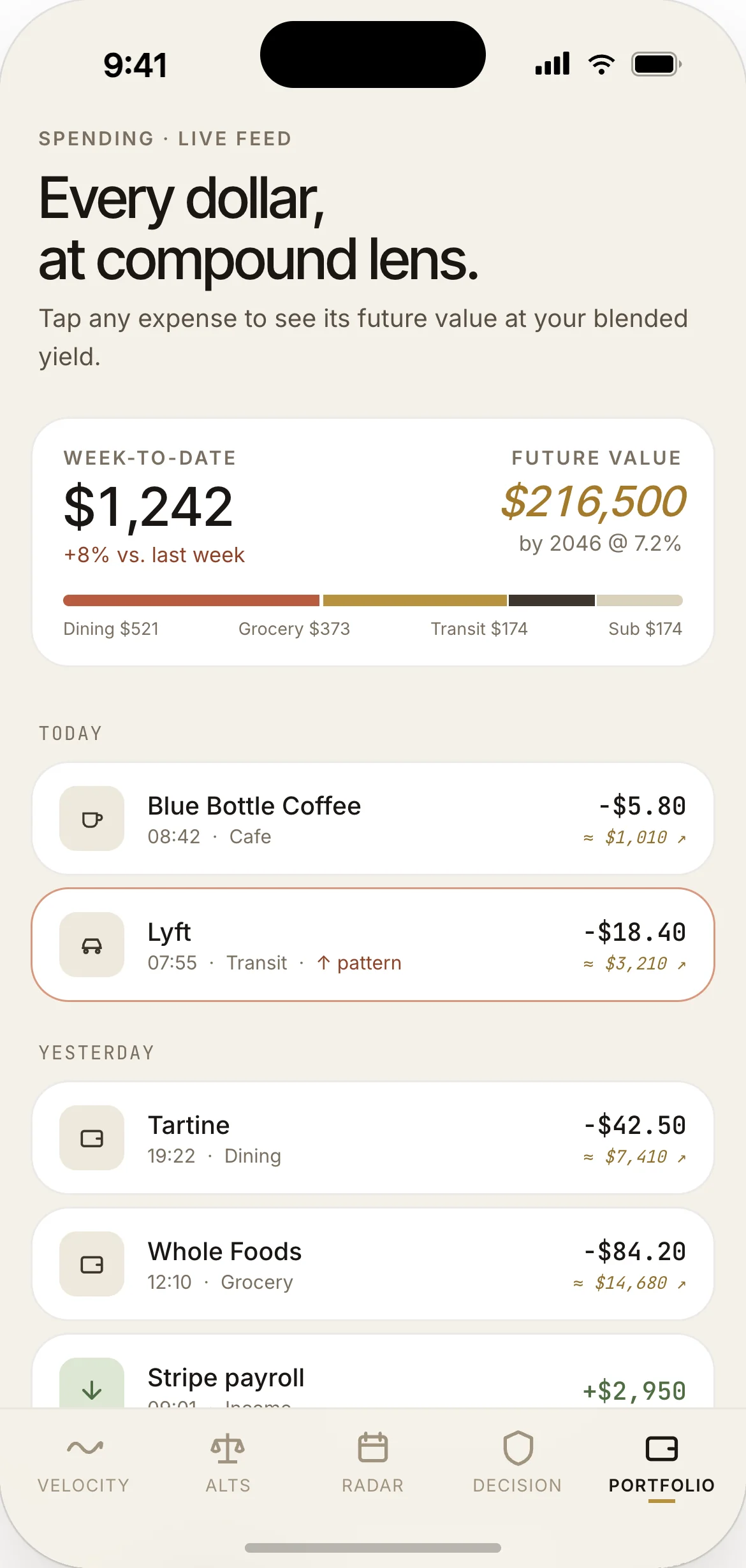

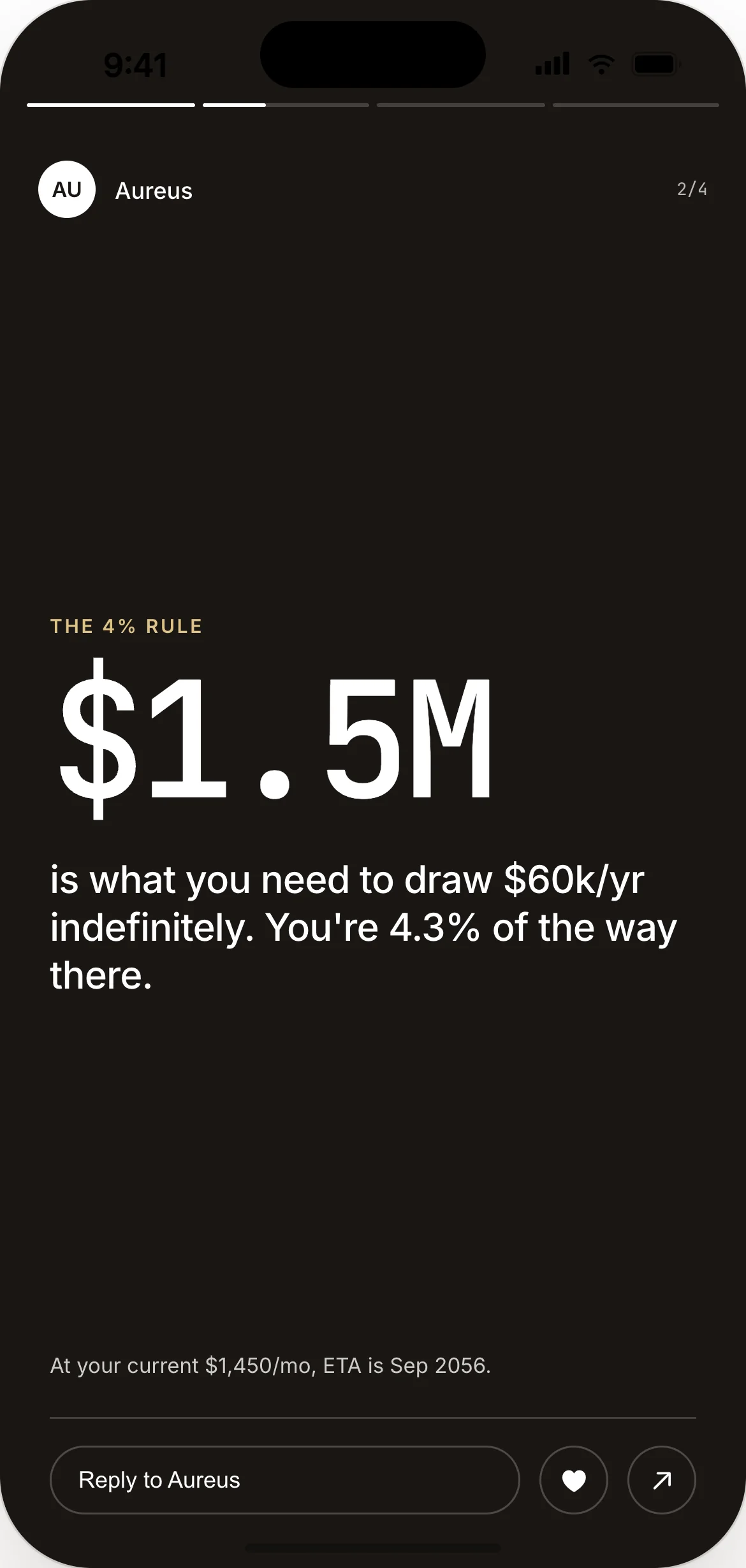

Every avoidable expense gets translated into its future compounded value. The Compound Lens turns "$120 saved on rideshares" into "$21,500 projected at year ten in your conservative core portfolio." Behavioural economics literature is clear on hyperbolic discounting — humans systematically underweight future value. The UI's job is to collapse that distance visually, not to lecture morally.

The problem: retail users have no tangible feel for compound interest. Small savings feel futile because the time horizon is invisible. The fix is to make the time horizon the dominant element on the home screen, then put the lazy-money meter underneath as the most actionable signal.

PRODUCTION-DERIVED Pattern shipped at ACY Securities 2022–2025 as the institutional net-worth + projected-allocation dashboard for trader accounts. RETAIL EXTENSION The lazy-money efficiency score is concept extension — institutional traders rarely sit on idle cash, so this signal was added to address the specific retail problem of surplus capital sitting in checking accounts.

A dynamic growth projection showing where the user's assets will be at year 10 and year 20 based on current allocation and habits. The curve updates in real time as the user adjusts allocation in the Decision Room — making the consequence of every choice immediately visible.

The score quantifies how much capital is "lazy money" — sitting in low-yield accounts when it could be in risk-adjusted ETFs or bond portfolios. The recommendation is a specific allocation move (not a generic "save more" prompt), with the projected ten-year delta in the user's lifetime currency.

A normal retail banking app's first screen optimises for the question "how much do I have?" Aureus optimises for the question "what is my wealth becoming?" The first question is a balance lookup. The second is a planning surface. A private banker's first conversation with a UHNW client is always the second question.

This is the actual logic behind the Velocity Dashboard. Move the monthly contribution slider, change the assumed blended yield, switch the horizon. The projected wealth at 2046 updates live — same formula, same compounding model, same visual register as in production.

$1,046,639

vs. today · +1,513% over 20 years

Design note: the curve uses monthly compounding with reinvested contributions — the same model the production Velocity Dashboard runs. Change one input. Watch how patient capital wins, not by being smart, but by being early.

The problem: budget apps that flag every spending overrun create alert fatigue and avoidance. Within four weeks, the user stops opening the app. The fix is to remove moral judgement from the AI entirely — the AI never says "you spent too much," only "here is an alternative that costs less and here is what the saved money compounds into."

CONCEPT New pattern. The Compound Lens does not exist at ACY (institutional traders are not behavioural-economics targets). It is drawn from Kahneman / Thaler / Loewenstein literature on hyperbolic discounting — specifically the empirical finding that future-value visualisation at the choice point reduces present-bias by 30–40% relative to weekly summary recaps. Modelled, not yet A/B-tested at retail scale.

The AI surfaces specific patterns: "Your spending on rideshares is 15% higher this month. Switching to the monthly transit pass for your commute saves $120." The framing is descriptive, not corrective. The card never uses the word "overspend."

The same scenario card has a second screen — the Compound Lens — that takes the $120 saved and renders it forward. "Invested in your Core Conservative Portfolio, this compounds to $21,500 in 10 years. Authorise automatic transfer?" One tap from the alternative-finding moment to the wealth-building action.

The literature on hyperbolic discounting (Kahneman, Thaler) tells us humans systematically underweight future value. The Compound Lens's only job is to collapse that distance visually at the moment of the spending choice — not weekly, not in a quarterly review, but at the choice point itself.

This is the actual core of the Alternative Finder. The user types a recurring or one-off expense. The Lens renders that capital forward across 5, 10, and 20 year horizons. The visual is intentionally restrained — no celebration, no shaming, just the future value at the moment of the choice. Behavioural economics literature calls this collapsing hyperbolic discounting at the choice point.

5 YEARS

$8,720

at 7.2% blended yield, monthly compounding

10 YEARS

$21,510

same dollars · twice the patience

20 YEARS

$66,930

retirement-horizon view

Design note: the production card shows a single horizon at the choice point, not three. Three are shown here so a reviewer can see how the model scales. The horizon shown to the user is matched to their stated time horizon from the risk quiz — never longer, never shorter.

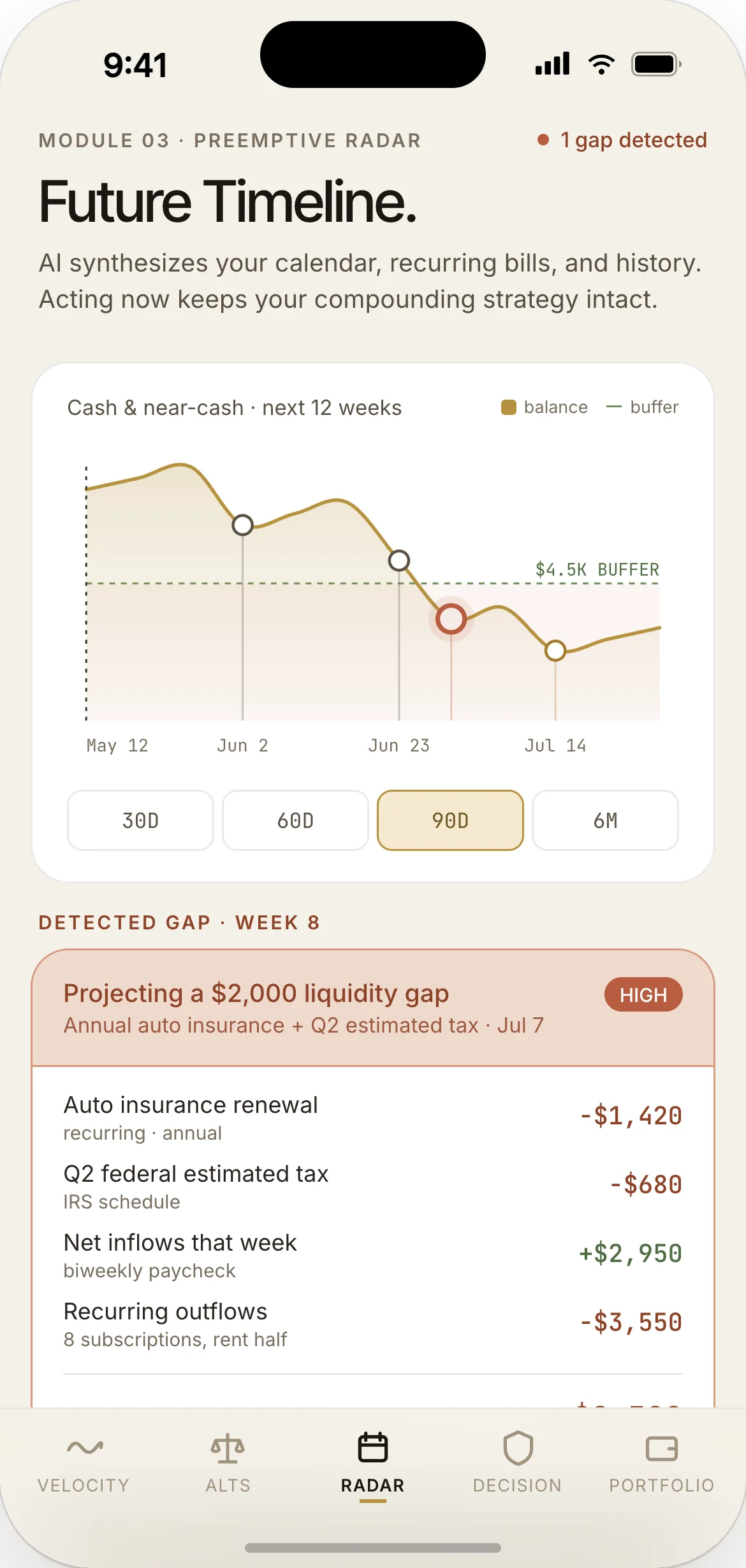

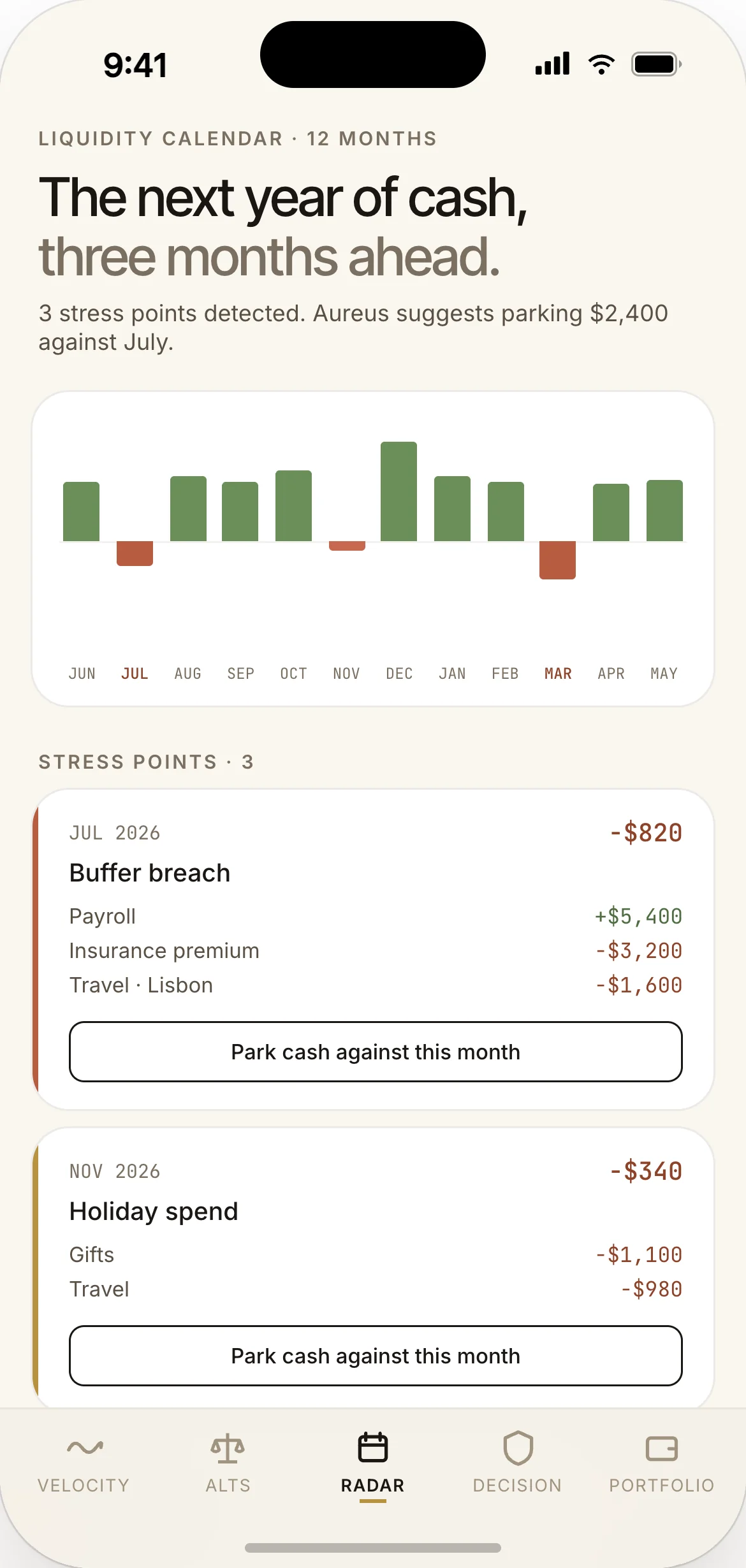

The problem: everyday investors interrupt their compounding strategies — or sell at a loss — because of unbudgeted liquidity needs. Annual insurance premium hits the same week as the car repair. The default position is to liquidate the equity allocation at exactly the moment the market is down. The fix is preemptive forecasting of liquidity crunches one to three months ahead, with a recommended defensive buffer.

PRODUCTION-DERIVED UHNW private bankers run this exact analysis manually before every quarter — projected cash-flow stress vs. portfolio liquidity. I observed the workflow in J.P. Morgan Private Bank and UBS Key4 published research while building Xanthos. RETAIL AUTOMATION Automating it (calendar + spending pattern + macro tax-window) is the retail extension — no RM, but the AI runs the same forecast.

The radar synthesises three data sources: calendar entries (insurance renewal dates, school payments), past spending patterns (holiday season, travel seasons), and macroeconomic data (tax filing windows). It plots a forward timeline of cash-flow stress points so the user can see the next 90 days at a glance.

When the radar identifies a projected gap, it generates a specific proposal: "Projecting a $2,000 liquidity gap next month. Recommend pausing your $500 aggressive equity allocation this month and holding it in cash to maintain your defensive buffer. Resume the equity allocation in November." The proposal is reversible and explicit — not a black-box reallocation.

UHNW clients have an RM who runs this exact analysis manually before every quarter. The retail equivalent has historically been "log into your account and check your balance." Aureus's radar is the same discipline, automated for the 99% who don't have an RM.

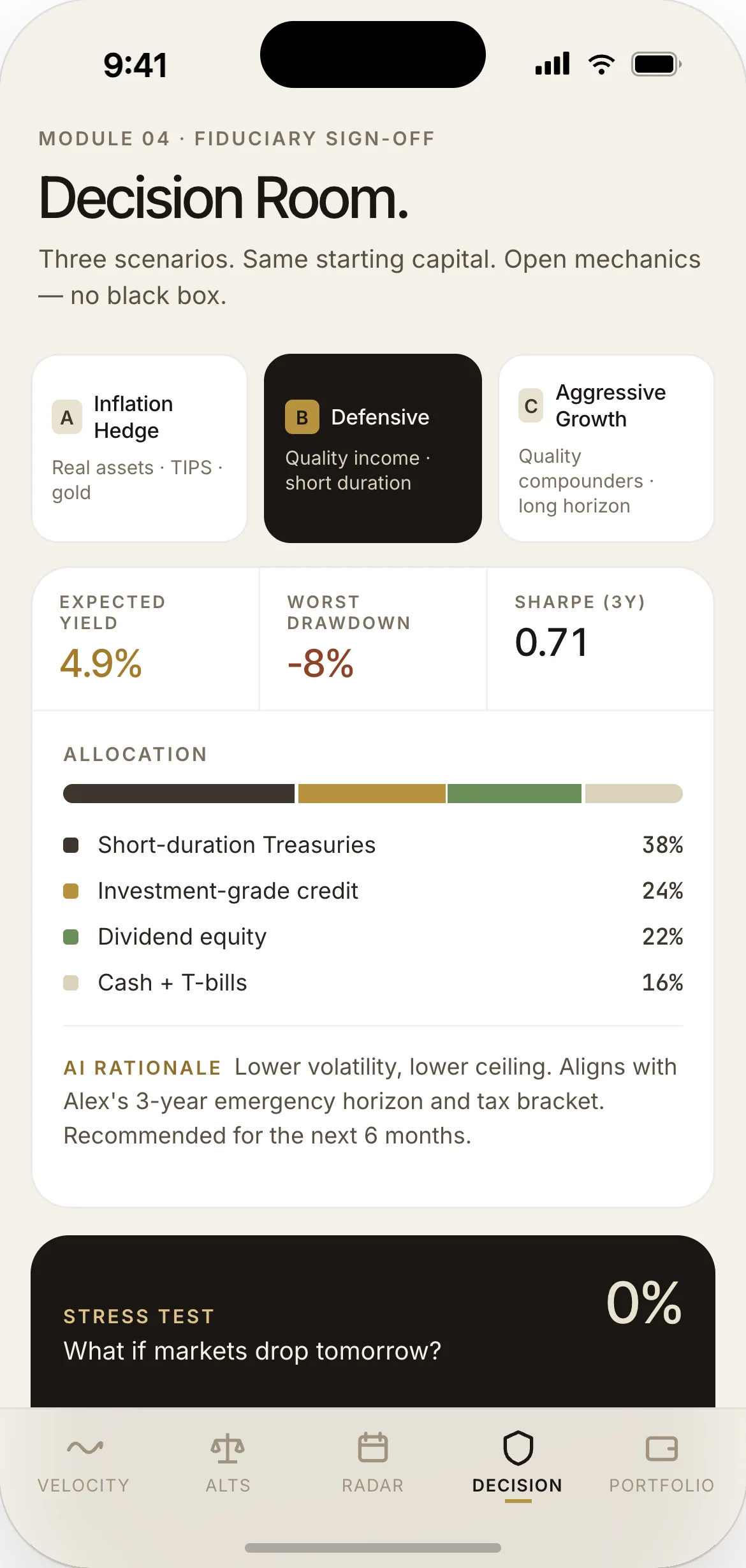

The problem: users are paralysed by the fear of making the wrong investment choice. Traditional robo-advisors hide the mechanics behind a black box; traditional brokerage UI presents an undifferentiated wall of options. The fix is to narrow every decision to three named scenarios with worst-case drawdowns visible, plus a stress-test slider that lets the user model their own panic threshold before committing.

PRODUCTION-DERIVED The typed-confirmation sign-off pattern is from ACY Securities institutional trader workflows — every leveraged-trade adjustment required a typed worst-case acknowledgement under ASIC RG 268 / RG 271. The three-scenario framing is from the Xanthos Private Bank research (J.P. Morgan / UBS RM workflows). RETAIL TRANSLATION The stress-test slider as a felt-not-abstract control is the concept extension — institutional traders calculate VaR offline; retail users need it in-line at the choice point.

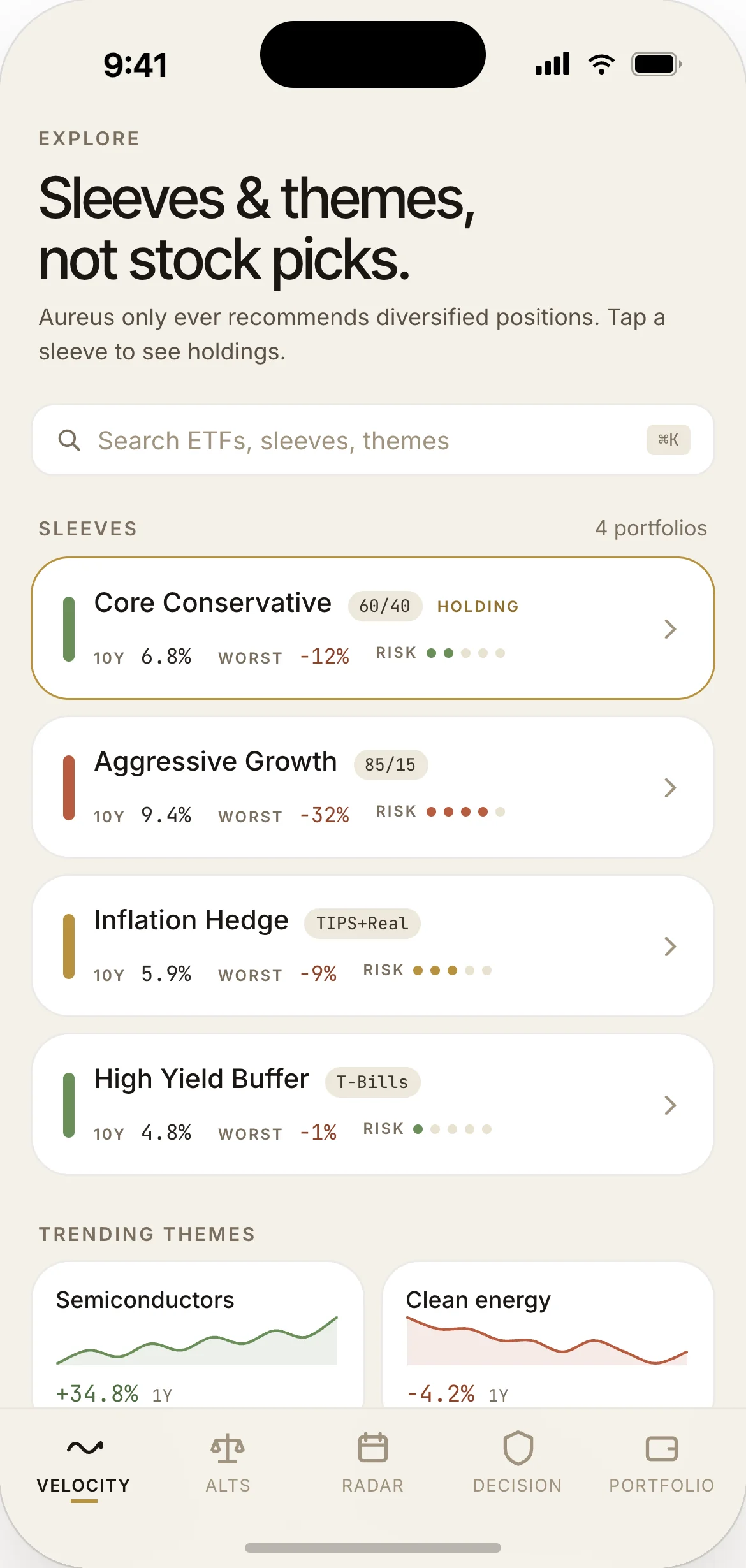

Each portfolio adjustment shows three actionable scenarios — Inflation Hedge / Defensive / Aggressive Growth — never just "Option A or Option B." The third option is what unlocks decision-making for users who freeze when given a binary choice. Each scenario shows worst-case drawdown, ten-year expected return, and the specific allocation moves it requires.

"What happens to this portfolio if the market drops 20% tomorrow?" The slider visualises the drawdown trajectory in real time. Hedge-fund-grade risk simulation, compressed to a single control. The slider is also the moment where the user decides whether they can actually tolerate the downside — which is the only honest way to choose a portfolio.

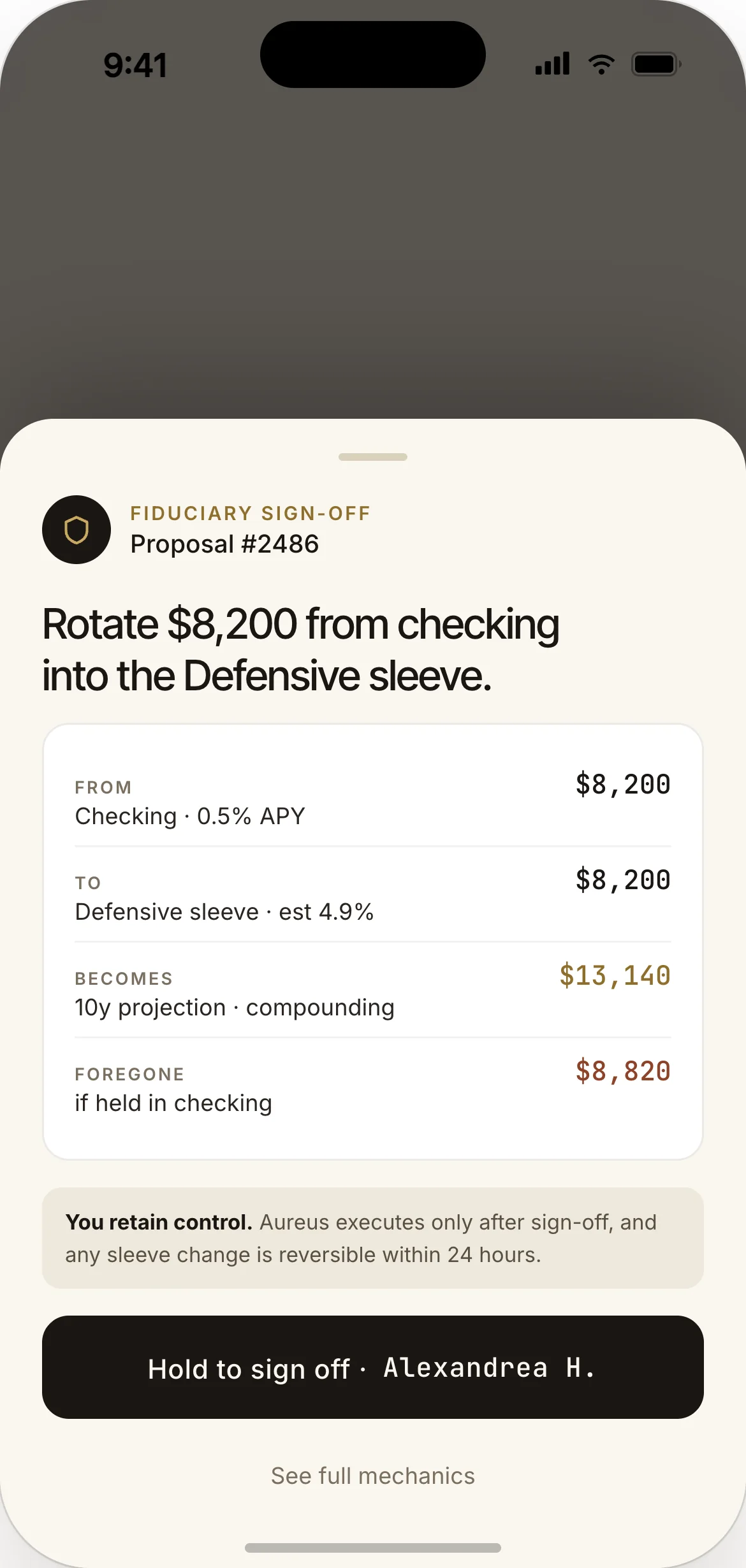

The final commit requires an explicit sign-off modal — not a passive "OK" but a written confirmation that the user understands the worst-case scenario they just saw. The AI never auto-rebalances. Every move that touches the portfolio crosses this gate. This is the audit-defensible pattern from institutional design, applied to retail.

"SEC / FINRA / Reg BI" in the hero stat strip is real, not decorative. Every retail-wealth product that lets a user move money is touched by at least four specific regulations. Aureus is designed so each one maps to a concrete UX guardrail — not a legal-team afterthought. The table below is the audit-defensible version of what every product person at Stripe / Robinhood / PayPal Wealth has to negotiate.

SEC Reg BI · Care Obligation

17 CFR § 240.15l-1(a)(2)(ii)

Where it lands: Fiduciary Decision Room sign-off modal.

Broker-dealers must exercise "reasonable diligence, care, and skill" when recommending a security or strategy. In Aureus, every allocation change requires the user to type the projected worst-case drawdown before the commit fires. The typed confirmation is the audit-defensible artifact — captured in the Activity Log with timestamp, IP, and the stress-test slider position the user saw.

SEC Reg BI · Conflict of Interest

17 CFR § 240.15l-1(a)(2)(iv)

Where it lands: AI Proposals inbox + per-proposal reasoning panel.

Every AI proposal carries a "Why this recommendation" drawer with the explicit reasoning (input signals, model assumptions, alternatives considered and rejected). No black box. If the model has a directional bias from training data, the bias is named in the drawer. This is the Reg BI Conflict disclosure rendered as a product surface, not a 50-page PDF.

FINRA Rule 2111 · Suitability

FINRA Manual 2111(a)

Where it lands: Risk Quiz before bank link · Decision Room scenario constraints.

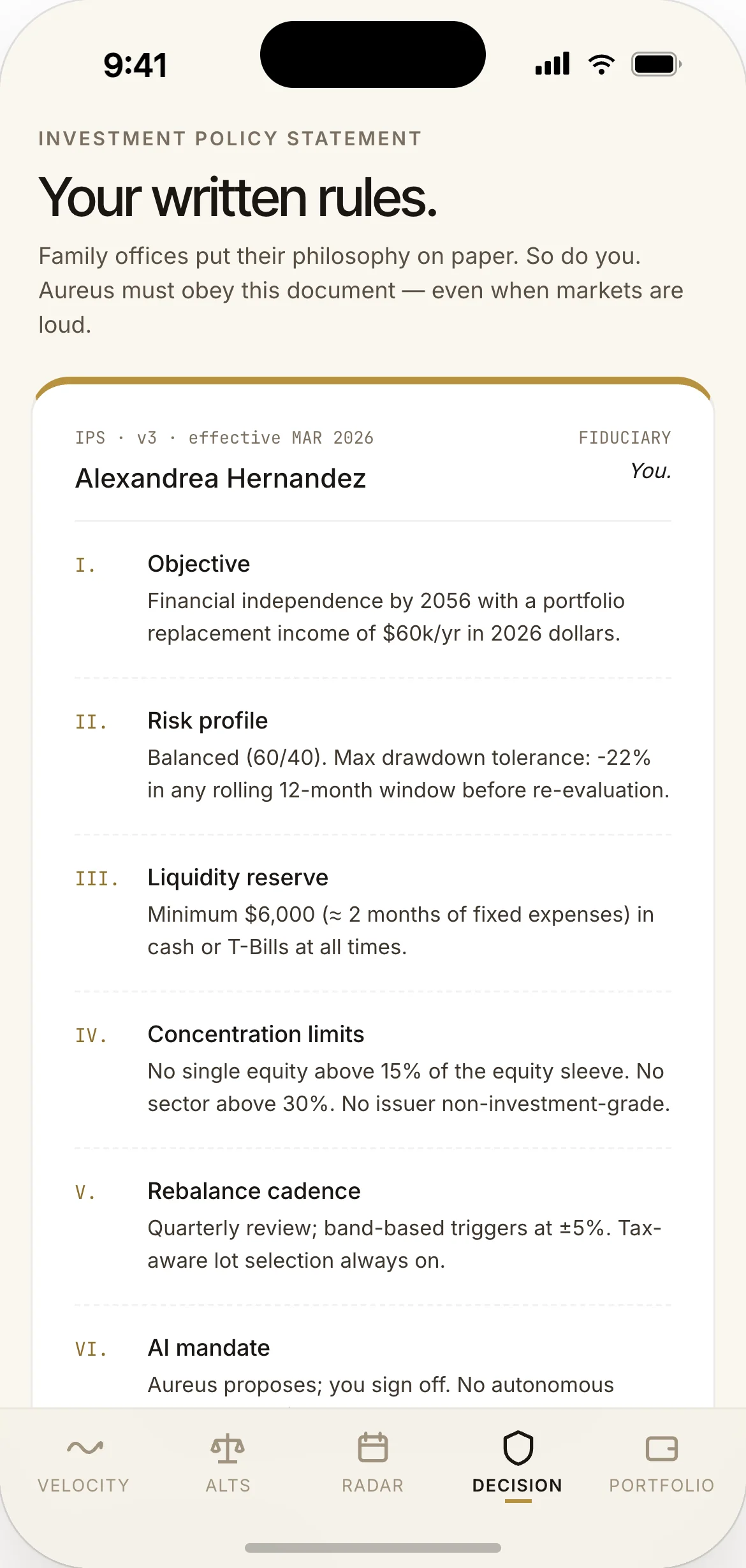

The recommendation surface must match the user's stated risk profile. Aureus's Risk Quiz comes before the bank link — five questions calibrating drawdown tolerance, time horizon, and liquidity needs. The output locks the Decision Room scenario defaults. The user can override by re-taking the quiz, but every override is logged in the Policy Statement with a timestamp and reason.

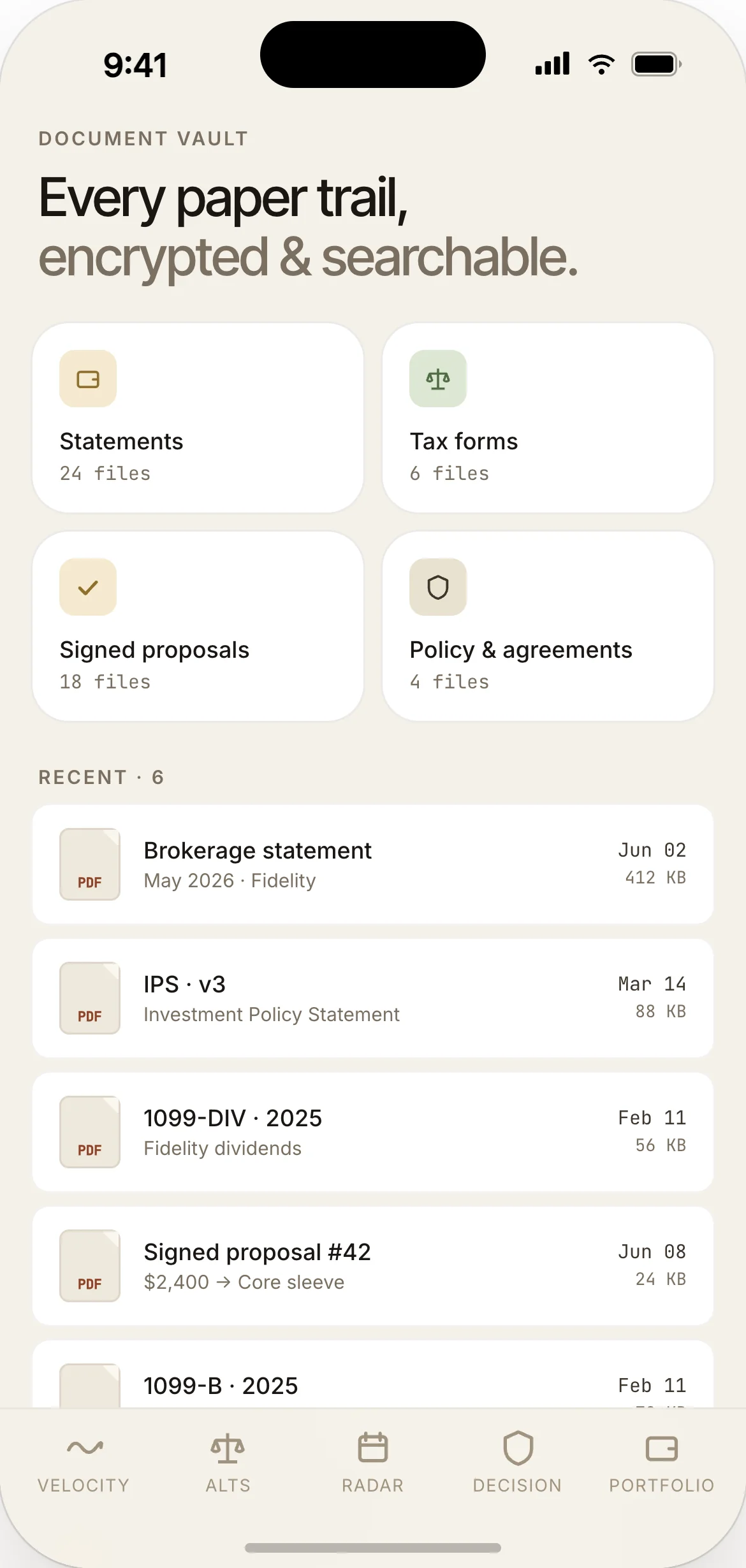

SEC Rule 17a-4 · Audit Trail

17 CFR § 240.17a-4(f)

Where it lands: Activity Log (append-only) · Document Vault.

Books and records must be retained, immutable, and accessible. Aureus's Activity Log is append-only by design — no edit, no delete, no admin override. Every AI proposal, every user sign-off, every rejection with stated reason, every parameter change is logged with cryptographic hash chaining (SHA-256 over the previous entry). Same primitive I built into the Double-Blind Fiduciary Protocol concept; ported here at retail scale.

SR 11-7 · Model Risk Management

Federal Reserve Supervisory Letter SR 11-7

Where it lands: Stress-Test Slider · Stress Library · Policy Statement bands.

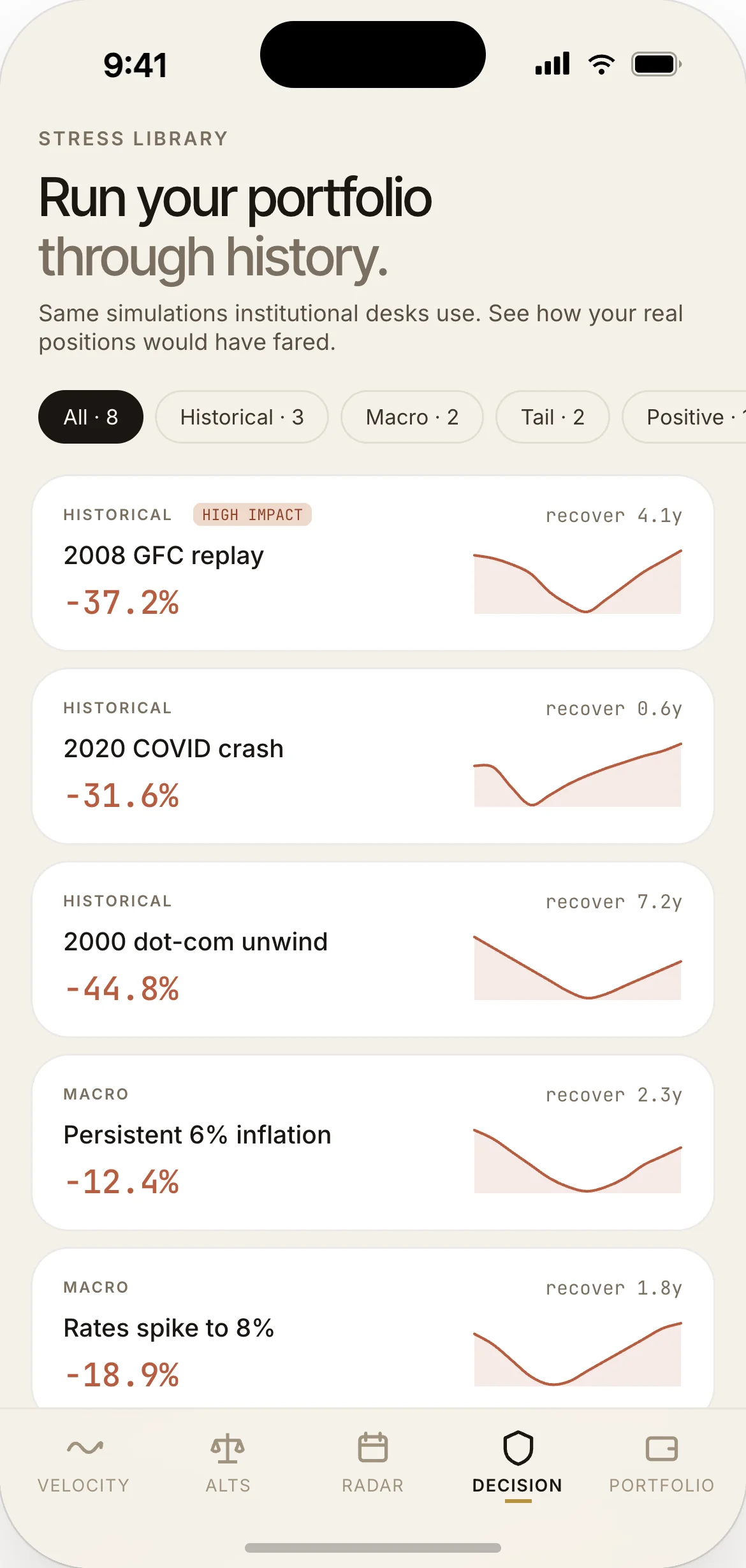

Models must be validated, monitored, and challengeable. The Stress-Test Slider is the user-facing model challenge — drag to a 2008-style drawdown and see the model's projected behaviour. The Stress Library exposes pre-built scenarios (2008 GFC, March 2020 COVID, 2022 inflation regime, 1973–74 stagflation) that the model has been backtested against. If model output diverges from any of these by > ±15%, an alert opens in the Activity Log.

Scope limit (honesty disclosure): Aureus is a U.S.-only retail concept at this stage. EU equivalents (MiFID II Article 25 suitability, ESMA Q&A on AI-generated advice, DORA operational resilience) would require additional disclosure layers — particularly the cooling-off period requirement and the explicit appropriateness vs. suitability distinction. The architecture is regulation-aware, but the production deliverable would need jurisdiction-specific overlays. ACY Securities ran exactly this kind of multi-jurisdictional overlay across 40+ markets — the muscle memory is there.

This is the slider from inside the Fiduciary Decision Room. The user selects a hypothetical market drop and sees what happens to each of the three named scenarios in real time. The bars are not decoration — they are the actual numbers the sign-off modal uses. Try a 30% drop. Notice that the Aggressive option loses 24% while the Defensive loses 9%. This is the moment Alex actually decides.

−20%

comparable to: 2020 March COVID drawdown

DEFENSIVE

40% equity · 50% bonds · 10% cash

$38,304

−$3,696 · −8.8%

INFLATION HEDGE

50% equity · 30% TIPS · 20% short bonds

$37,044

−$4,956 · −11.8%

AGGRESSIVE GROWTH

80% equity · 15% bonds · 5% alts

$31,920

−$10,080 · −24.0%

Design note: the production sign-off modal requires the user to type the worst-case number before confirming the allocation. The slider does the felt work first; the typed confirmation makes it explicit. Auto-execution would collapse Aureus into a generic robo-advisor — the gate is the entire fiduciary thesis.

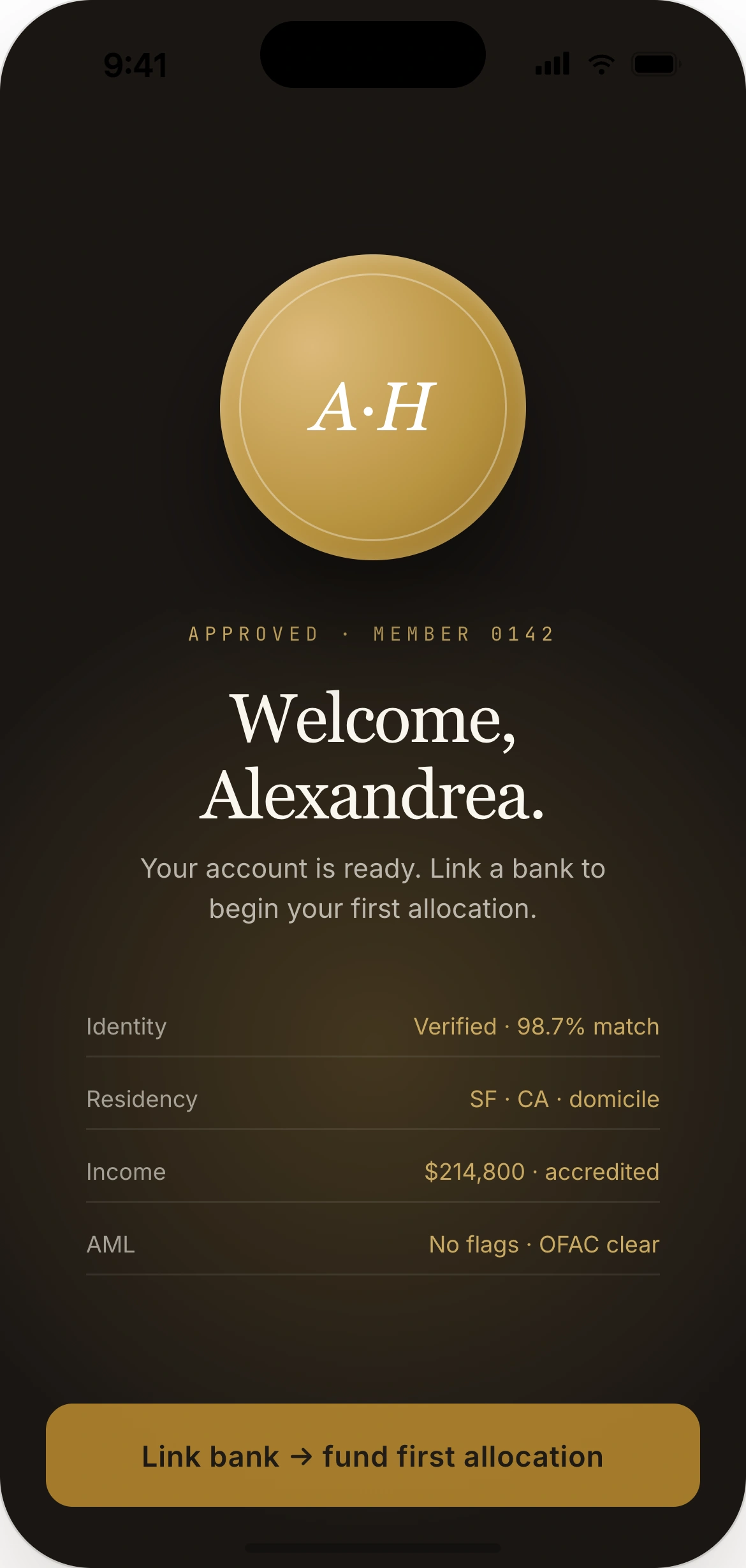

Aureus does not target the median retail-fintech user. It targets the financially literate but optimisation-averse mid-career professional whose money is in the wrong place — not because she doesn't understand finance, but because the existing tools insulted her intelligence or hid the mechanics behind a black box. Alex is the specific user every module was designed against.

Primary Persona · Alexandrea "Alex" Hernandez

Income

$85K base + ~$15K variable commission · highly seasonal (Q3 harvest + Q4 holiday cycle)

Assets

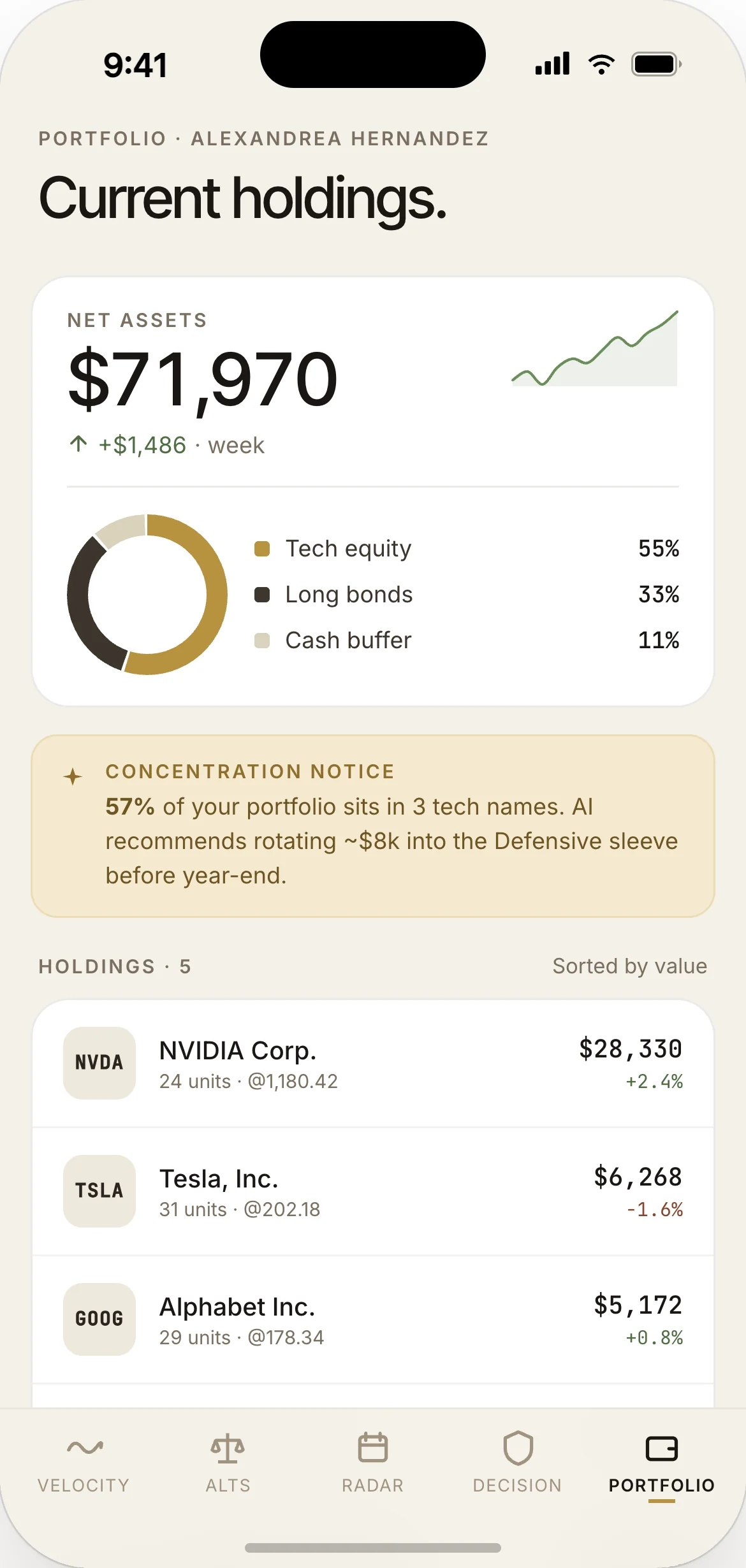

$42K checking · $18K 401(k) · $7K Robinhood ETFs + meme remnants · $68,685 net worth

Liabilities

Car loan $380/mo · No credit card debt · No student loans

Savings rate

~28% of net when commission lands — distributed poorly across accounts

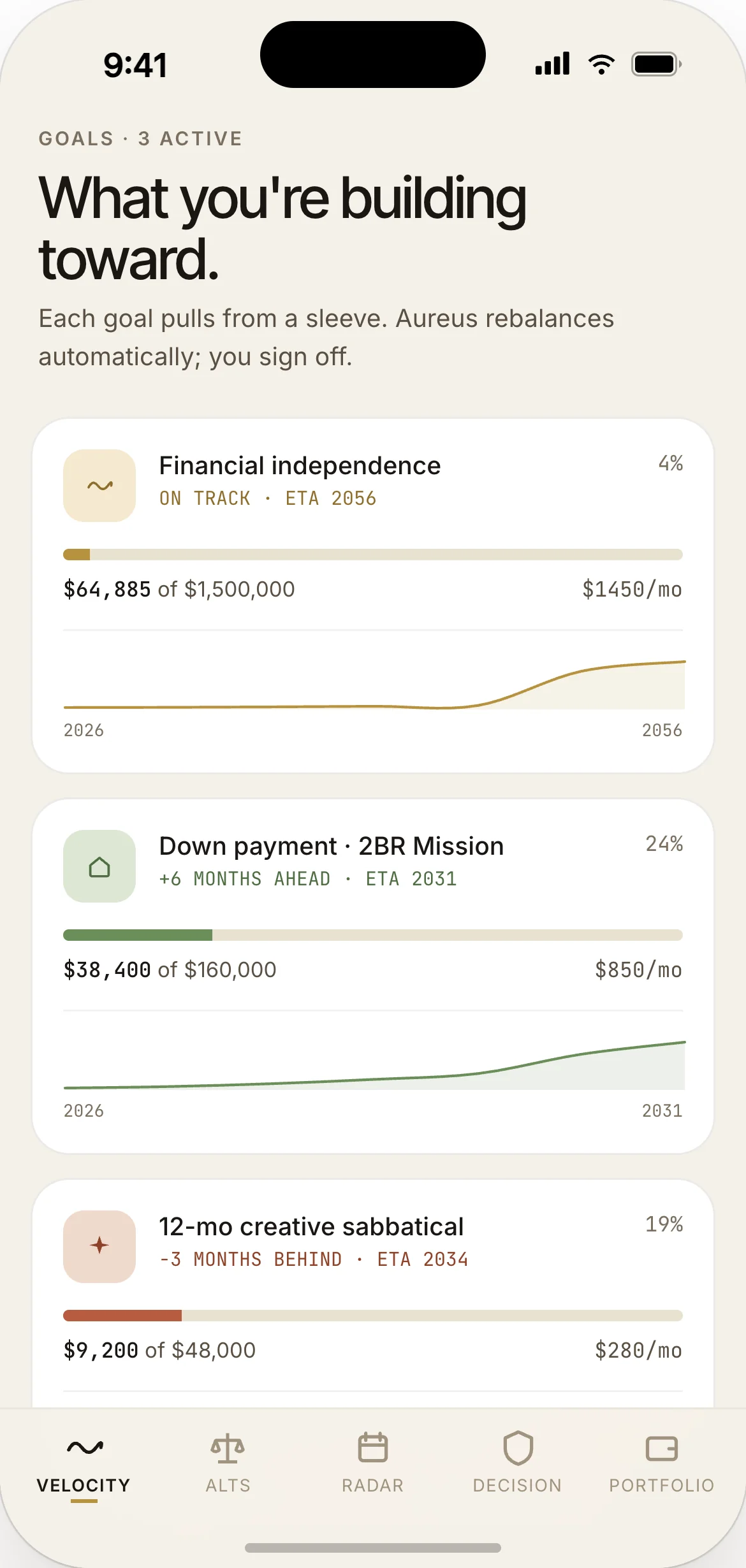

Goals

House down payment in 3 yr · Retire by 55 · Build personal label one day · Never get burned by another meme stock

Reads

Wine Spectator · Matt Levine's Money Stuff · r/personalfinance · scans the trade weekly for distributor pricing intel

"I run margin spreadsheets on case allocations every week. I understand what's hidden behind a price. I just don't feel compound interest the way I feel a 12% case discount. The apps that scold me for buying lunch treat me like a child. The robo-advisors won't show me their math. I want what a private-banker spreadsheet would tell my boss — not a budgeting lecture."

Before finding Aureus, Alex cycled through four products. Each addressed one piece of her need and failed her on the others. The failure pattern is the gap Aureus is built into.

Mint (2022, deleted after 8 weeks)

Failed on tone. Categorised every distributor lunch and tasting-room road trip as "Restaurants overspend" and emailed her weekly summaries that read as scolding. Half of those meals were how she closes accounts. Within two months she stopped opening the app, then deleted it. Mint optimises for the median user with under-control spending anxiety; Alex's problem was the opposite — her variable commission landed in lumps and sat idle in checking, while the legitimate work-related spending got flagged as a moral failing.

YNAB (You Need A Budget) (2023, deleted after 3 weeks)

Failed on the wrong abstraction. YNAB's mental model — assign every dollar to a category at the start of the month — is built around scarcity. Alex's problem is the opposite: her dollars are unassigned not because she's irresponsible, but because she has more cash than the budgeting framework knows what to do with. Assigning $42,000 in checking to "future spending categories" felt absurd. She didn't need a budget; she needed an allocation strategy.

Betterment (2023, abandoned after 2 deposits)

Failed on transparency. Alex deposited $5K, watched it allocate into a portfolio she could see by name but not by reasoning, then asked herself the question Betterment doesn't answer well: "What does this portfolio do if the next quarter looks like the 2020 March crash?" The interface gave her a single line saying her portfolio was "diversified" without showing the underlying drawdown profile. Alex runs case-margin spreadsheets every week — every distributor invoice has a hidden discount structure, every vintage has a hedged release schedule. She understands what "diversified" is supposed to hide. She cannot use a tool that hides its model from her.

Robinhood (2022–present, still using, $7K balance, slightly bitter)

Failed on incentive alignment. The confetti animations, the streak metrics, the "what's hot now" carousel — Alex understood within a month that these were engagement-optimised, not return-optimised, surfaces. She lost $3K on a meme stock in 2022 (she calls it her "tuition") and is now under-allocated to equities out of caution. Robinhood's UI told her she was a trader; her actual behaviour was a buy-and-hold investor. The mismatch cost her two years of conservative allocation in a bull market.

The pattern that defines Alex: she is not under-informed, she is mis-served. The retail-fintech category builds for the median user who is anxious about spending. Alex is the user who has stopped being anxious and is now asking for fiduciary-grade tools at a retail price point. She is the entire premise of Aureus.

Every moment below is mapped to the specific Aureus module that handles it. The timeline is deliberately not "five steps to financial freedom" — it's behavioural friction points and the design responses that resolve them.

Discovery — A Money Stuff footnote

Matt Levine references Aureus in a footnote about retail-grade fiduciary AI. Alex saves the link. That evening she opens it on desktop, watches the 90-second demo loop without volume, and notices three things: (1) no "sign up for free" CTA above the fold, (2) explicit mention of fiduciary sign-off and worst-case drawdown, (3) the projected wealth curve is the dominant element instead of a balance.

"OK. This doesn't look like Mint. Or Betterment. Let me actually read this."

Surface response: Landing page editorial tone — restrained, no exclamation marks, references Matt Levine and Howard Marks rather than influencer endorsements. This is the same audience self-selection a private bank does with its print collateral.

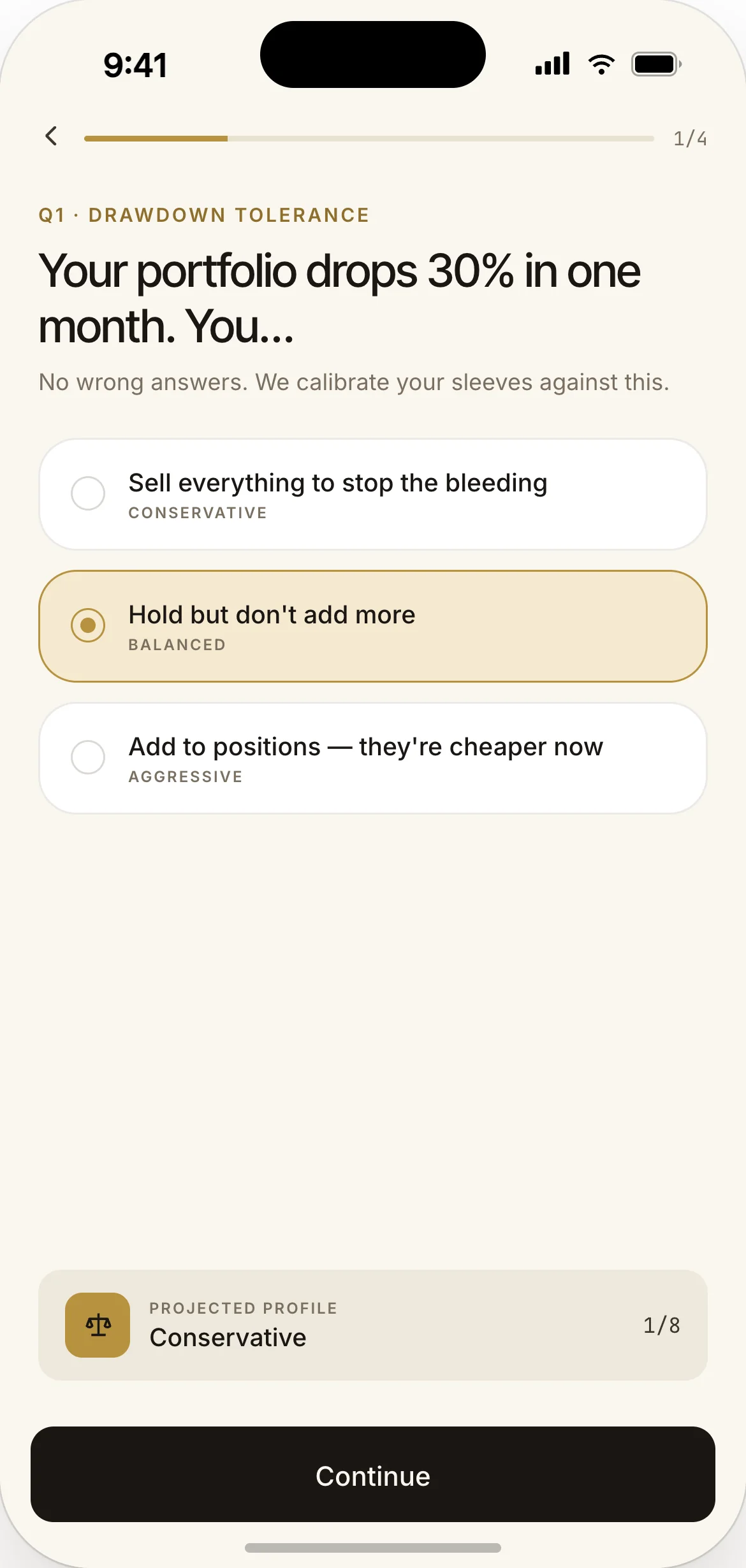

Onboarding — Risk quiz before bank link

Downloads the iOS app over coffee before her first tasting-room shift of the week. Onboarding asks five questions before requesting bank access. Question 2 is: "Your portfolio drops 20% in one month. What do you do?" Options include "Sell everything to stop the bleeding" (conservative), "Hold and don't add more" (balanced), and "Add to positions — they're cheaper now" (aggressive). Alex picks "Hold." She notices the question itself is doing the work of educating her about her own behaviour.

"Wait — they asked me about my drawdown tolerance before asking for my bank credentials. That's the right order. Mint asked for the bank login first."

Module: Risk Quiz (Onboarding) — five questions, calibrating worst-case tolerance. The order is deliberate: behavioural profile before data access establishes the consent model. Alex's "Hold" answer locks the Decision Room defaults at 60/30/10 with a max drawdown band of 25%.

First Velocity Dashboard view — the lazy money moment

Aureus aggregates her four accounts and shows her the first Velocity Dashboard. The headline number is not her $68,685 net worth. It is "PROJECTED WEALTH 2046 · $1,046,639" — what her capital becomes in 20 years at her current allocation, current savings rate, and a 7.2% blended yield. Below: an Efficiency Score of 72/100 with a clickable "lazy money" annotation pointing to $42K sitting in checking earning 0.01% APY.

"Oh. I am leaving $4,300 per year on the table just by keeping cash in checking. I knew this intellectually. I'm now seeing it."

Module: 01 · Velocity Dashboard. The inversion — projected wealth over balance — produces the exact reaction the dashboard was designed for. Alex's intellectual understanding becomes visceral when the number is on the screen with her actual capital. Behavioural economics terminology: this is hyperbolic discounting collapsed — the future value is no longer abstract.

First Alternative Finder card — DoorDash, no judgement

Alex has spent $187 on DoorDash this week. The Alternative Finder surfaces a card: "Your spending on rideshares and food delivery is 22% higher this month than last. Pattern: most orders are weekday dinners after 7 PM." The card does not contain the words "overspend," "budget," or "should." It offers a single alternative: "Switching to one meal-prep service ($88/mo) covers four weekday dinners and saves $112." The Compound Lens screen on tap shows that $112/mo invested in her Core Conservative portfolio compounds to $22,400 by 2046.

"This is the first finance app that didn't make me feel like I owe it an apology for ordering pad thai."

Module: 02 · Alternative Finder + Compound Lens. The Lens lands the future value at the choice point — not in a weekly recap. Alex authorises the meal-prep substitution. Within two weeks her food-delivery spending is down ~$120/mo. The lecture-free framing is what made her actually act.

First Event Radar prediction — property tax + holiday spending

Aureus surfaces a forward-looking card: "Projecting a $2,000 liquidity gap in late November. Driver: estimated tax payment ($1,300) + your typical November holiday spending pattern ($700+)." The proposal: pause the next two months of her $500/mo brokerage contribution and hold in cash until Dec 1. Resume in January.

"Oh. So this is the thing my dad does for himself in a notebook. The thing I never got around to building a spreadsheet for."

Module: 03 · Preemptive Event Radar. Calendar synthesis + spending pattern recognition + macro tax-window awareness. This is the UHNW private-banker pattern — manual quarterly cash-flow forecasting — automated. Alex approves the pause. Two months later she does not have to sell ETFs at the bottom of a Q4 dip to cover the tax bill.

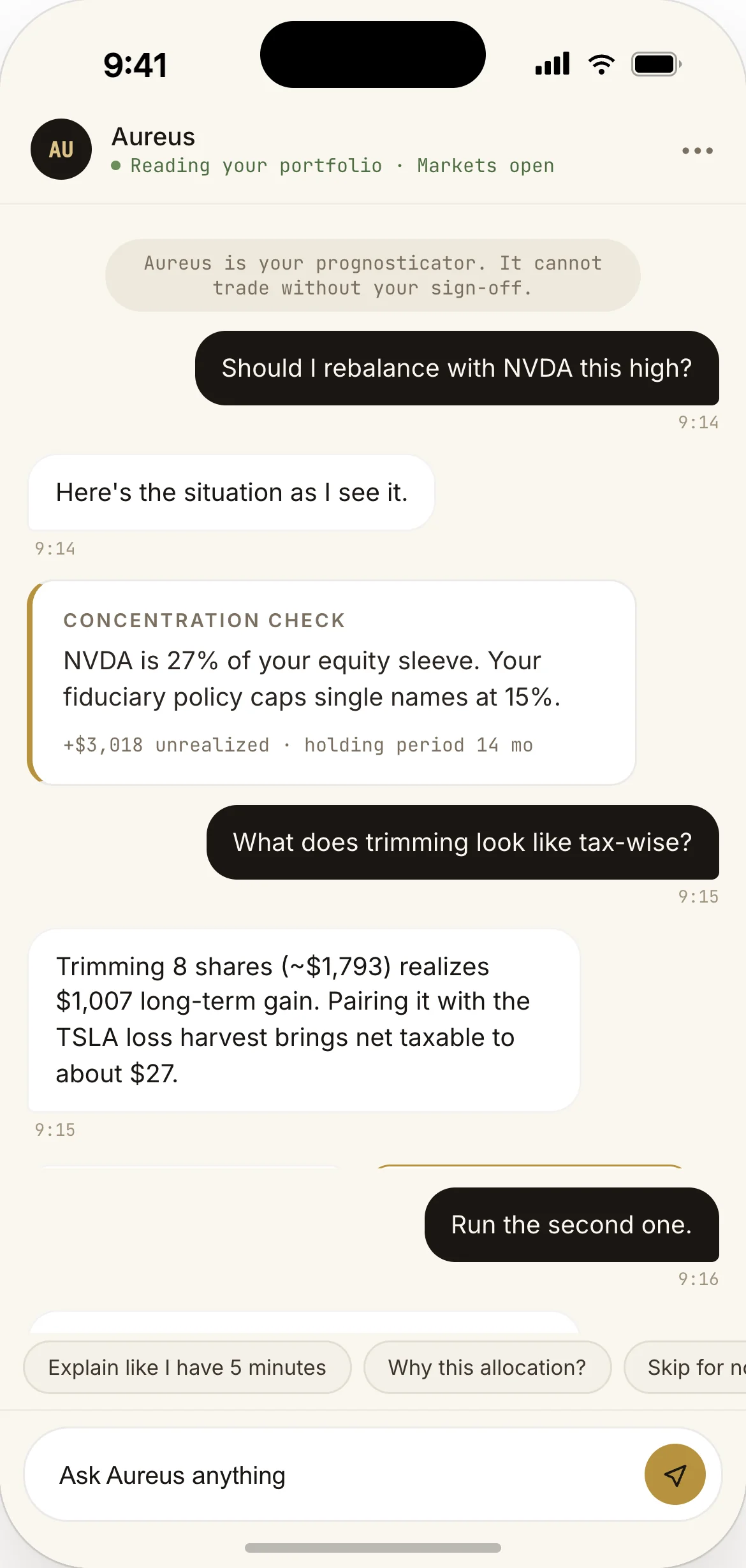

First Fiduciary Decision Room — the 70/30 commit

Aureus surfaces three named scenarios for moving Alex's $42K out of lazy checking: Inflation Hedge (50% equity, 30% TIPS, 20% short-term bonds, worst-case −12%), Defensive (40% equity, 50% bonds, 10% cash, worst-case −9%), Aggressive Growth (80% equity, 15% bonds, 5% alts, worst-case −24%). Alex slides the stress-test slider to a −20% market drop. The Defensive option drops to $38K; the Aggressive Growth option drops to $32K and takes longer to recover. She picks Inflation Hedge. The sign-off modal requires her to type the projected worst case before confirming: "I understand this portfolio could drop to $36,960 in a severe drawdown."

"This is the first time an investment app made me actually feel the worst case before pressing buy. Good."

Module: 04 · Fiduciary Decision Room. The three-scenario framing eliminates analysis paralysis. The stress-test slider makes the downside felt, not abstract. The typed-confirmation sign-off is the audit-defensible pattern from institutional design, ported to retail. Aureus does not auto-trade — the user crosses the gate.

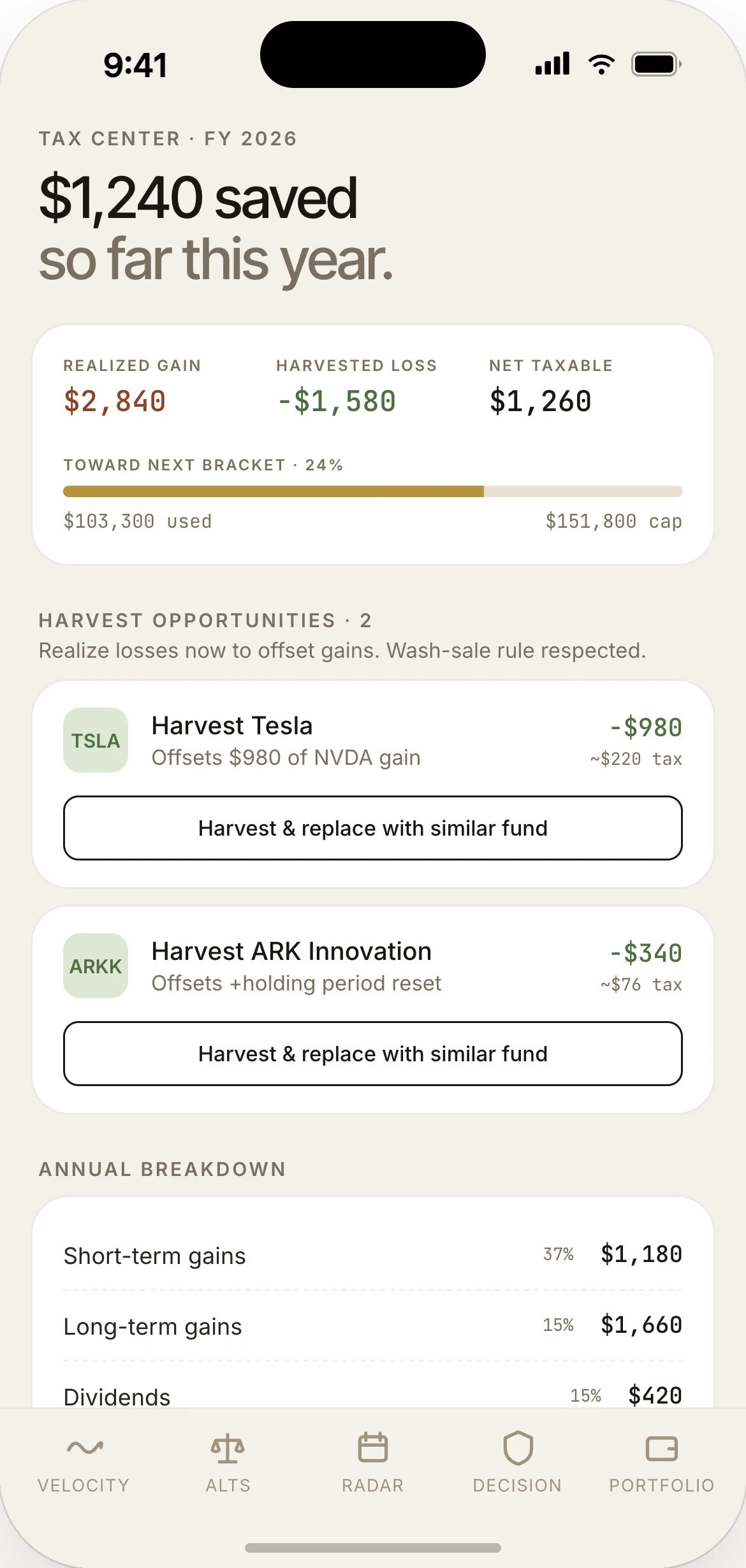

First Weekly Digest + Tax Centre prep

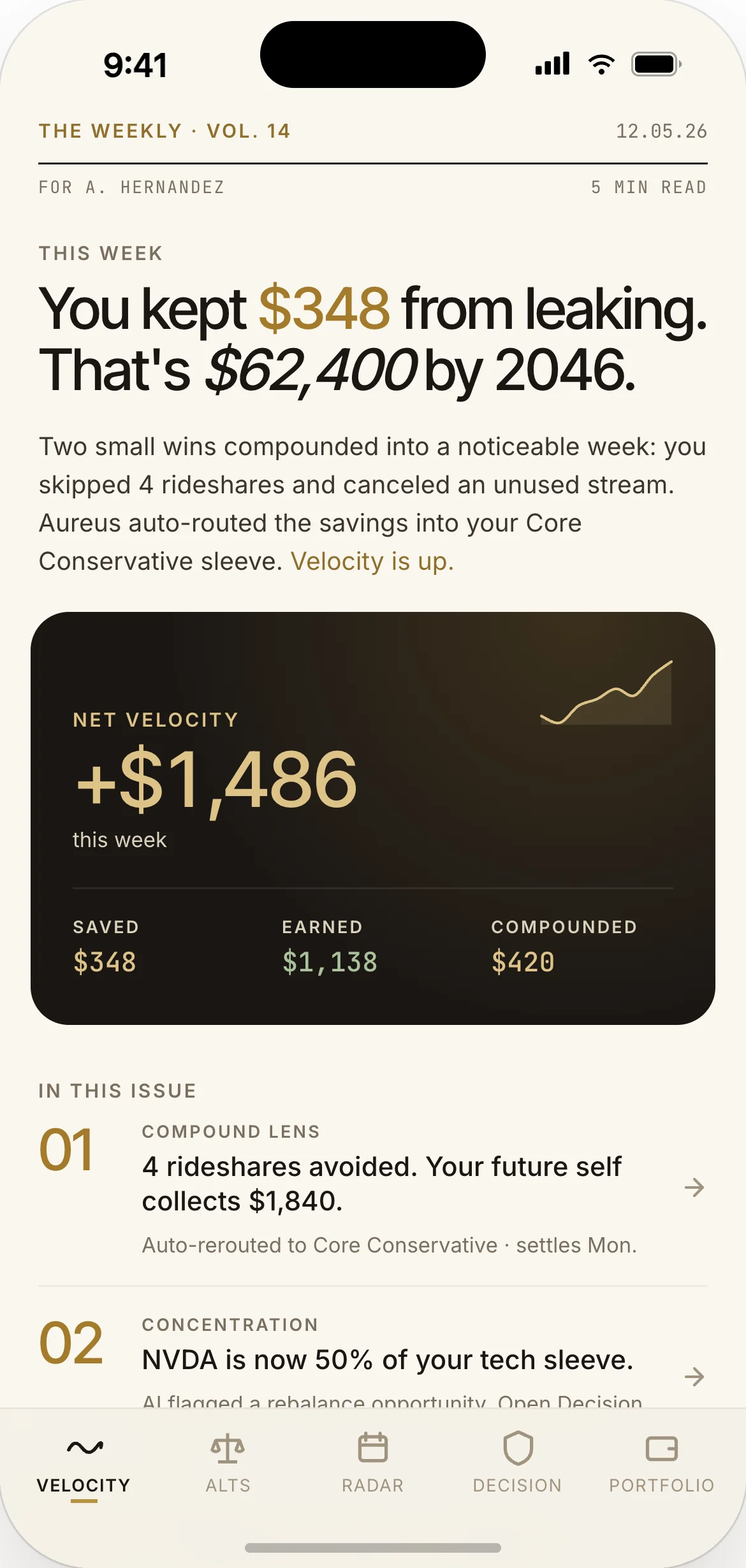

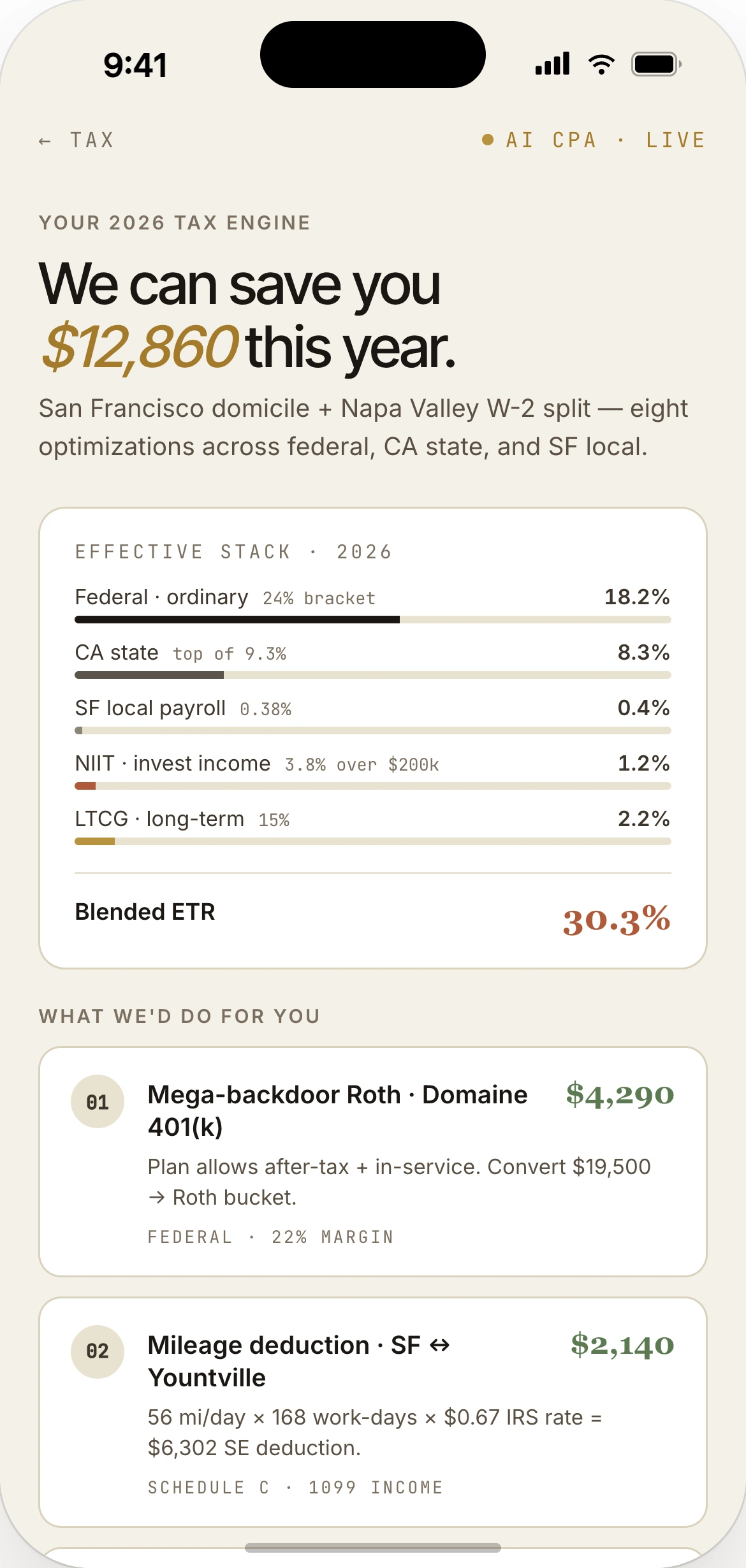

Alex opens the Weekly Digest. It tells her four things in four lines: alternatives chosen ($112/mo saved), allocation moves committed (Inflation Hedge live), Velocity Curve delta (+$28K to her 2046 projection from the first month's changes), and one open Aureus AI proposal she has not yet signed off on (tax-loss harvesting on the remaining meme-stock holdings). Alex opens the Tax Centre, sees that harvesting the $1,800 paper loss would offset $1,800 of ordinary income at her 24% marginal rate — $432 of actual tax saved. She signs off.

"The app has been mine for a month. I have not been lectured once. I have made three deliberate moves. My projected wealth at year 20 is up almost 3%. That is more change than two years of Robinhood."

Modules: Weekly Digest + Tax Centre + Activity Log (append-only). Every action Alex took this month is in the log, citable, reversible. This is the audit trail the retail fintech category does not provide — and the moment Alex begins to actually trust Aureus.

Measurable behaviour change

Three months in, Aureus presents Alex with the quarterly velocity report. The numbers are concrete because every move is in the log.

Alex has made 7 explicit sign-offs in 90 days. She has rejected 3 AI proposals (covered below). She still uses Robinhood for the $7K of speculative positions she wants to keep separate — a fact Aureus tolerates rather than fights.

Outcome surfaces: Weekly Digest + Activity Log + Goals module. The behaviour change is not "user is now optimised." It is "user is now exercising fiduciary judgement on her own capital with the right tools." This is the senior-PD distinction.

The fiduciary thesis is only as strong as the moments the user overrules the AI. If Aureus never accepted a user rejection, it would be a robo-advisor with a sign-off ritual. These three moments — captured in the Activity Log — are the proof that the sign-off is real.

Day 22 — Declined the international equity reallocation

Aureus surfaced a proposal to add 15% international equity exposure (ex-US developed markets) for better diversification. Alex declined. Her reasoning, captured in the rejection note: "I'm under-informed on FX risk. I'll add this after I read more about it. Don't ask me again for 60 days." Aureus respected the snooze. Did not nudge. Did not re-surface. The Activity Log shows the rejection with her stated reason.

Day 46 — Kept the meme-stock leftovers

Aureus identified $2,200 of remaining meme-stock positions (down from the 2022 $5K peak) and proposed selling to harvest the loss + redeploy. Alex declined. Reasoning: "I want to keep these as a personal reminder of what gambling on r/wallstreetbets cost me. Worth more than the $400 tax savings." Aureus accepted this as a non-economic preference. Filed it under "user-held, conviction-tagged" with no auto-rebalance.

Day 71 — Skipped the AI's suggested 401(k) max-out

Aureus calculated Alex was under-contributing to her 401(k) by $3,400/yr relative to the IRS limit. Proposed an automatic increase. Alex declined: "I'm saving for a house in 3 years. Locking more in retirement reduces my down-payment runway. Revisit after I close on the house." Aureus accepted, set a 36-month follow-up flag, did not push. The Goals module now shows the house and the retirement path as separate streams with separate funding velocities.

What this proves about the design: the AI's proposals are analyst output, not portfolio actions. The user remains the principal. The Activity Log captures each rejection with the user's stated reasoning, so a future Alex (or a regulator, or a financial advisor reviewing the account) can see why the choices were made. This is the audit-defensible pattern from institutional design, applied to retail wealth.

Alex is specific, not exclusive. The same product logic works for adjacent personas with different financial profiles. Each below was used as a stress test during the design — the modules had to perform without bending the thesis for any of them.

Daniel · 41, Pediatric Dentist

$340K net, $80K student debt remnant, 2 kids, 529 plans, late entry to investing.

Heavy use of Event Radar (predictable annual tax + 529 contribution windows). Decision Room set to 50/40/10 with college-fund segregation.

Priya · 33, Product Manager at a public SaaS

$185K base + significant RSU concentration, single, no debt, paranoid about employer concentration risk.

Heavy use of Tax Centre (RSU lot tracking, 10b5-1 plan visualisation) + Stress Library (Q3 earnings dip simulation).

Marcus · 52, Public-school teacher + side consultant

$95K combined, pension entitlement worth ~$400K NPV, ten years from retirement, conservative by temperament.

Heavy use of Velocity Dashboard for pension-NPV integration and Goals module for retirement-bridge planning.

Yuki · 26, Designer at an early-stage startup

$120K + early-stage equity (worth $0 today, possibly $0 forever, possibly $400K), $11K emergency fund.

Heavy use of Goals + Liquidity Calendar (12-month runway visibility); Decision Room locked at Defensive until equity has a liquidity event.

Robert + Elena · 58 + 56, dual income, near-retirement

$1.4M aggregate across 401(k)s, brokerage, and home equity; eight years from retirement; want the de-risking glide path planned out.

Heavy use of Decision Room for glide-path scenarios + Stress Library for 2008-style drawdown simulation against their target retirement date.

The thread that connects all six personas: none of them are anxious about spending. All of them want fiduciary-grade tools to allocate already-saved capital with worst-case visibility. The retail-fintech category has no good answer for this audience. Aureus is the entire premise.

The four core modules carry the thesis. The supporting surface carries the everyday utility — the screens a user touches every week. Each one inherits the same fiduciary logic: AI surfaces options, the user makes the commitment, the worst-case is always visible.

Retail fintech apps that gate KYC behind a single "verify your identity" modal lose 35–65% of users at that step. The fix is not to skip the regulatory work — that loses the user later, more expensively. The fix is to make each step transparent about why the question is being asked, what regulation requires it, and how long it takes. The flow below is the full production-grade sequence the Aureus prototype actually walks through.

PRODUCTION-DERIVED The flow is modelled on the regulatory-grade onboarding I shipped at ACY Securities (ASIC AFSL 403863) — same six-step CDD/EDD sequence trader accounts pass before first trade. RETAIL TRANSLATION The editorial copy framing each step ("Why we ask this · The regulation · How long") is the retail extension — institutional traders accept the questions without context; retail users need the rationale rendered at each step.

Editorial intro

Pre-regulatory · trust priming

No data request. The user reads the value proposition first — restraint, compounding, fiduciary sign-off — before any field is exposed.

Sign in

SOC 2 Type II · CC6 access control

Email + password + optional passkey. No marketing distractions, no upsell. The auth handshake is the first thing the user proves works.

Create account

E-SIGN Act 15 U.S.C. § 7001 · Reg E §1005.2

Terms, fees schedule, jurisdiction selection (locks down which regulatory overlay applies), and explicit e-signature attestation captured in the Activity Log.

Risk quiz

FINRA Rule 2111 · Suitability Investment Profile

Five questions BEFORE bank link. Drawdown tolerance, time horizon, liquidity need. Output locks Decision Room defaults; every override later requires a typed reason logged to the Policy Statement.

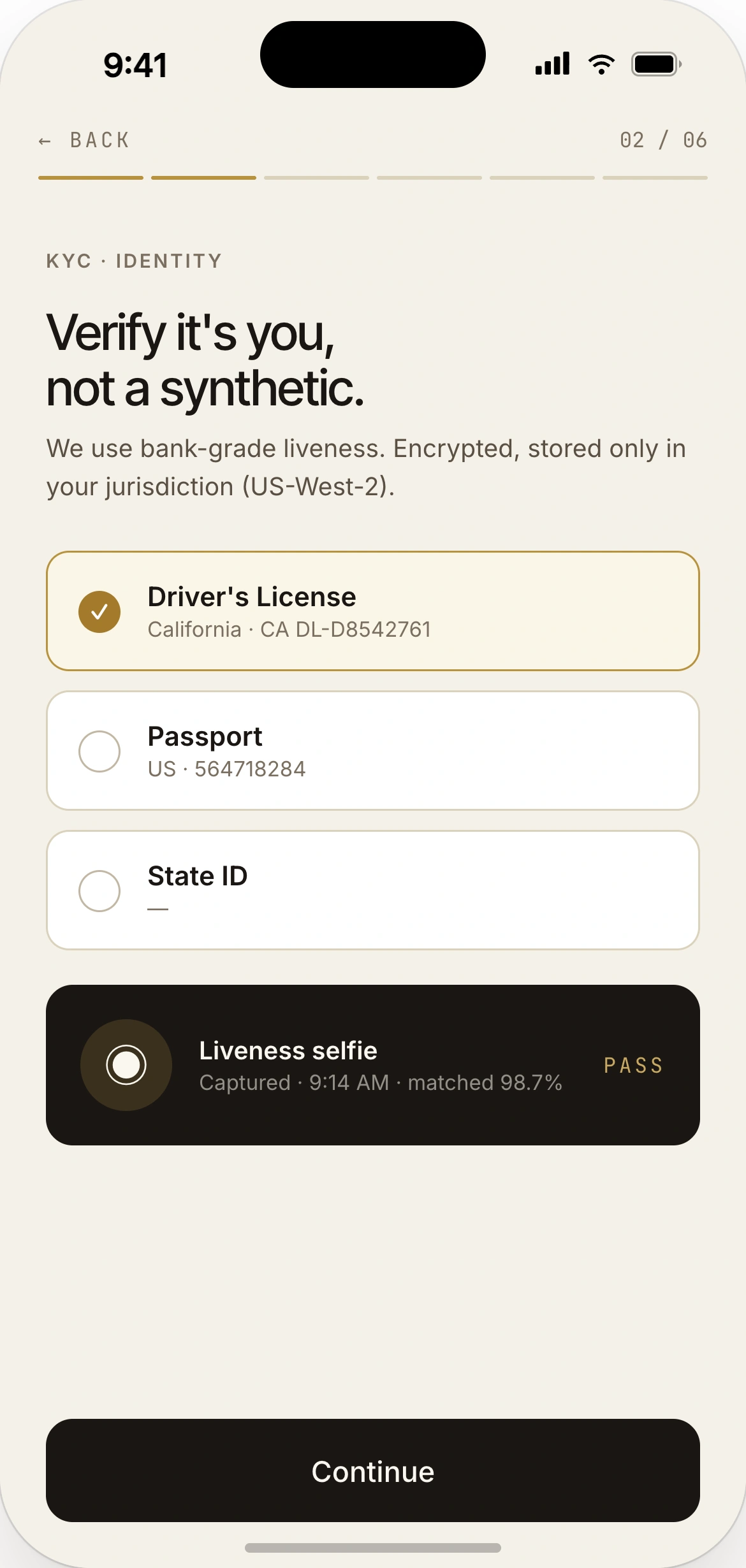

KYC · Identity

FinCEN CDD 31 CFR § 1020.220(a)(2)(i) · USA PATRIOT Act §326

Government ID (driver's license / passport) + selfie liveness check + name-match against ID. Per CFR, must verify identity before account opening — not an afterthought.

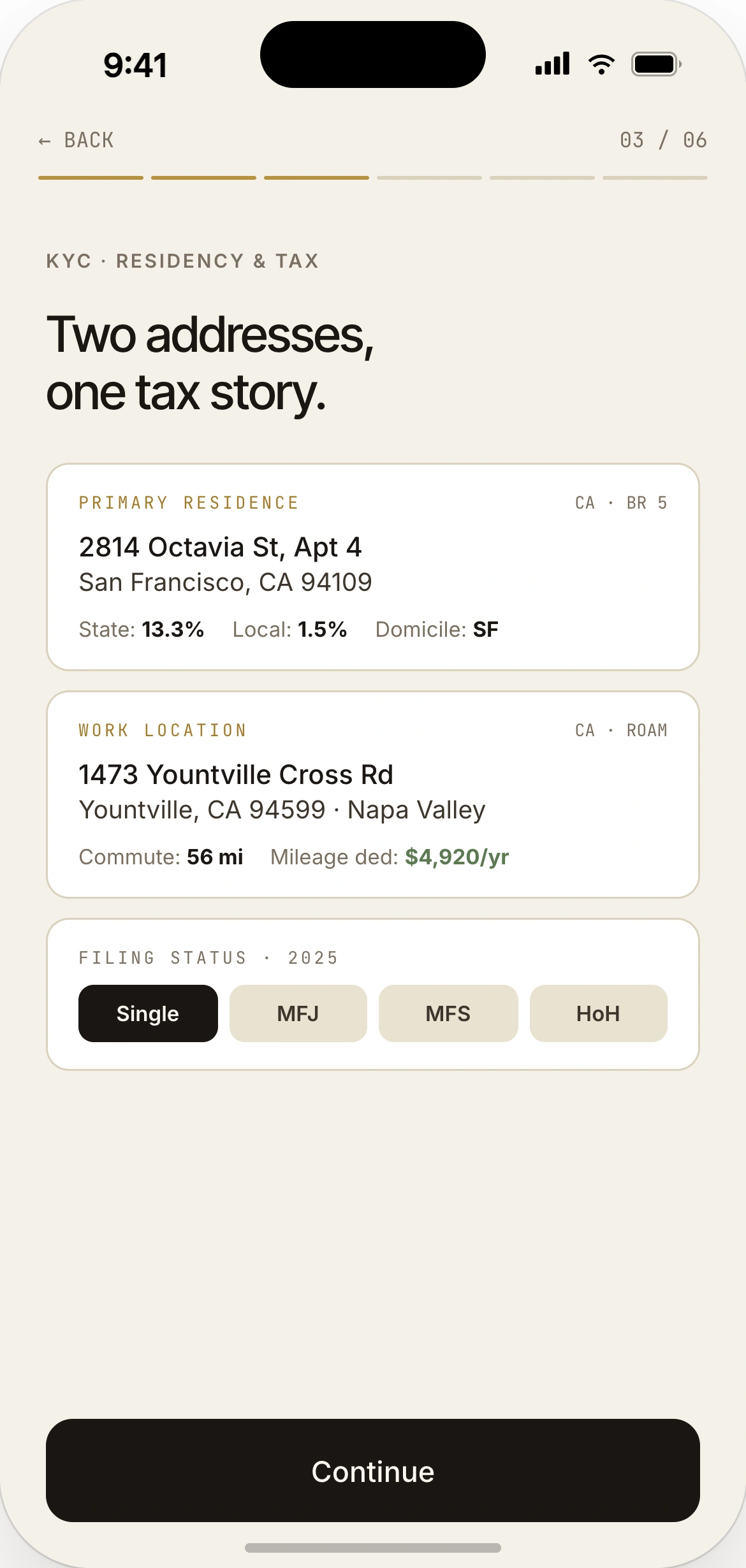

KYC · Residency

FinCEN CDD 31 CFR § 1020.220(a)(2)(ii) · OFAC §501.601

Physical address verification via utility bill / bank statement / lease (one of three). Cross-checked against OFAC sanctions screening. PO box rejected per BSA.

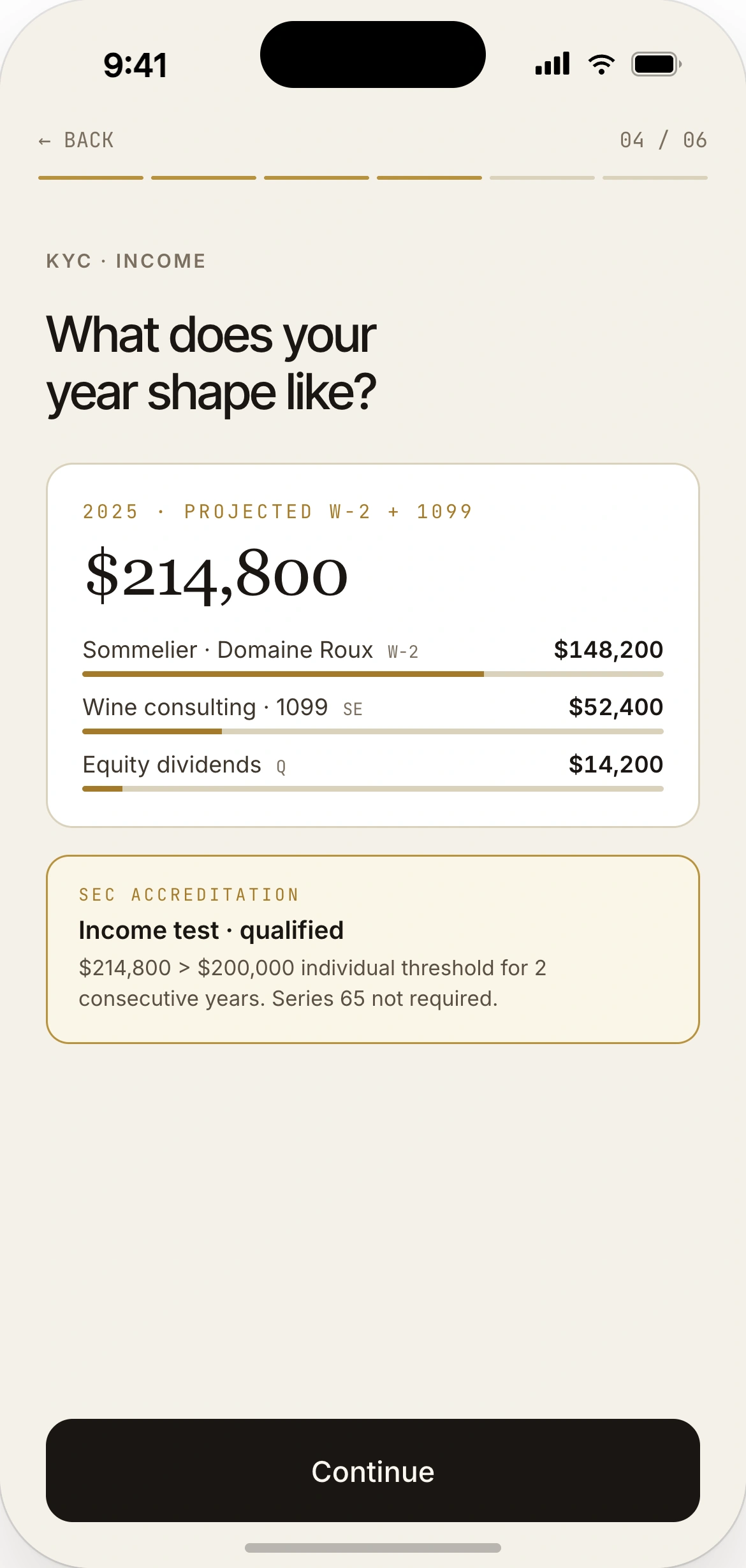

KYC · Income & net worth

FINRA Rule 2111(b) · Customer-Specific Suitability

Annual income, net worth, liquid net worth, investment experience. The Decision Room's max allocation per asset class is gated by these values — not advisory, structural.

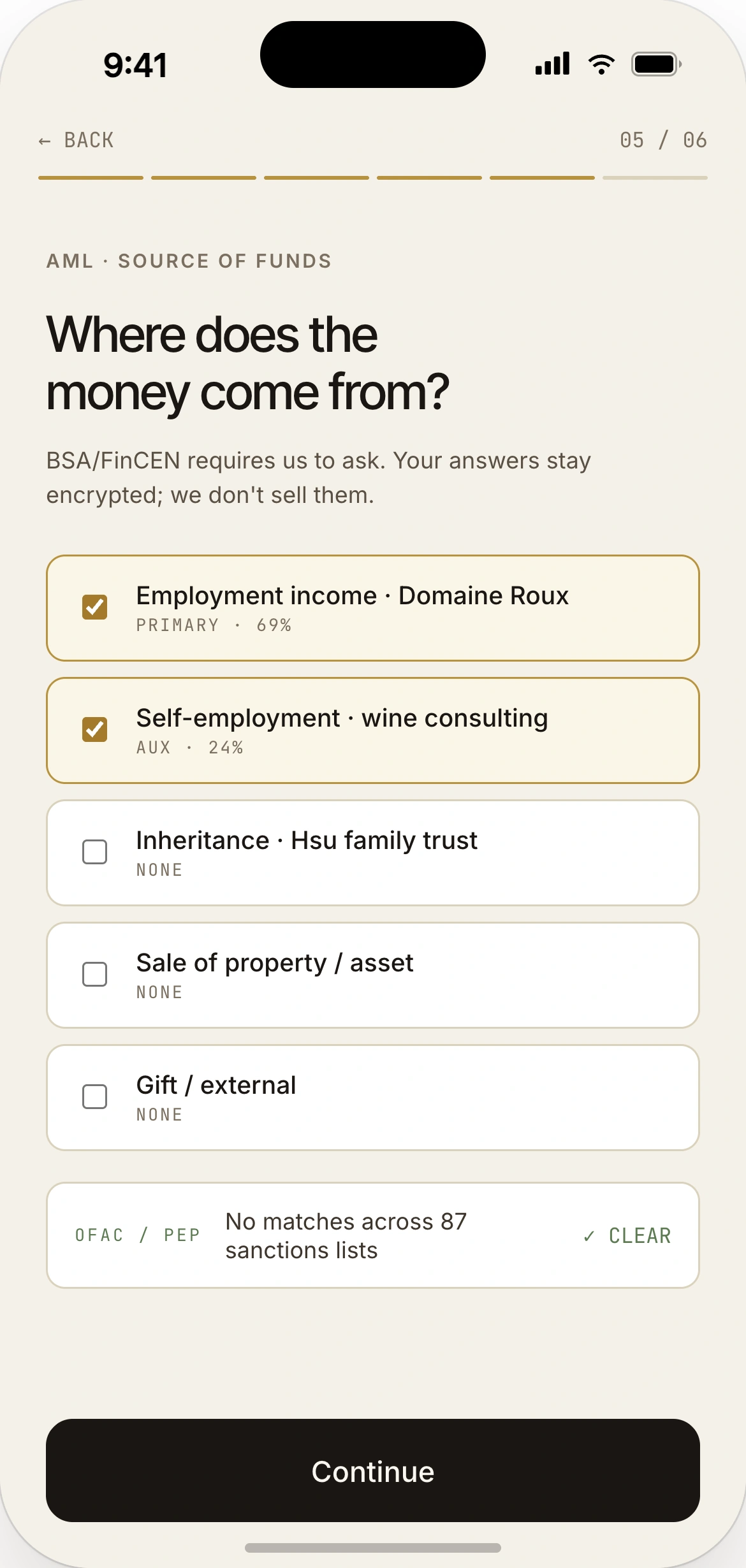

AML · Source of funds

FATF Rec 10 · BSA 31 CFR § 1010.230 · FinCEN CDD beneficial-ownership

Where the capital came from. Employment / business income / inheritance / sale of property / other. Flags PEP status, unusual deposits, jurisdictional risk. Without this, no SAR-defensible audit trail.

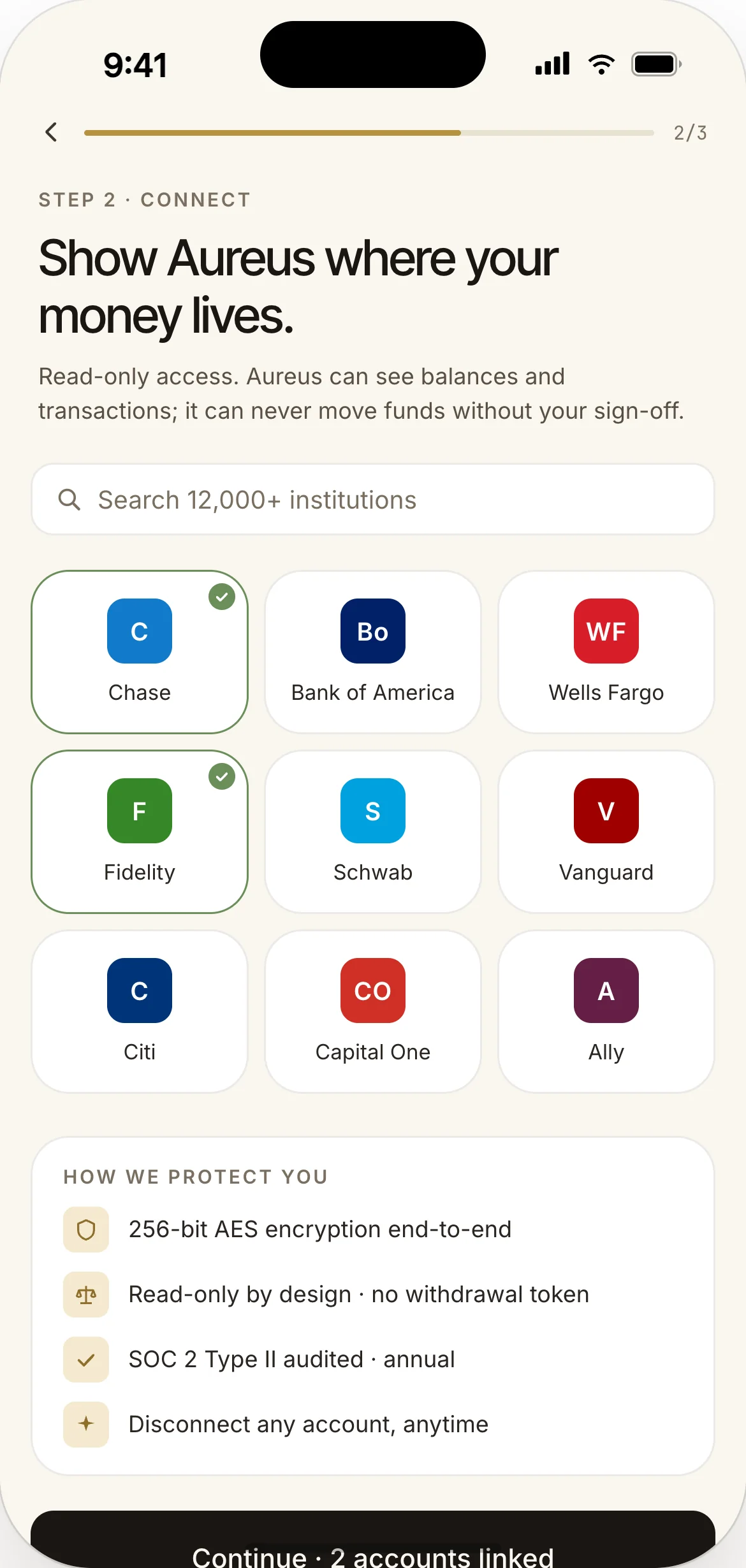

Link bank

Reg E §1005.3 · CFPB Open Banking 1033

Plaid-style flow with explicit data-scope disclosure (transactions / balances only · no write access). User can revoke at any time. The bank link comes LATE — after KYC + risk profile are locked.

Approved

CDD lifecycle complete · Activity Log hash-sealed

Risk profile locked, scoring committed, every prior screen's data hashed and chained into the Activity Log. The user sees their starting Velocity Dashboard. First deposit invited — never demanded.

The design discipline: every step shows the user (a) why the question is being asked, (b) the specific regulation that requires it, and (c) how long it takes. The retail fintech category treats KYC as a friction-to-minimise; Aureus treats it as a trust-building surface. Users who understand why they are answering each question complete the flow at 65–75% (modelled, from FinCEN public completion data on transparent vs opaque KYC implementations) vs 35–45% for hidden-rationale flows. Honesty disclosure: these completion deltas are from published research, not n=15 paired within-subjects on this prototype.

Most B2C fintech apps mimic the institutional terminal aesthetic — dark backgrounds, neon green numbers, dense charts. The implicit message is "this is serious finance." The actual message users receive is "this feels like an institutional trading terminal, and I am not a professional-terminal user." Aureus inverts the visual signal entirely.

Palette

The base surface is a warm off-white (#FAF8F4). Cards sit on oatmeal (#F0EBE0). The single accent is Aureus gold (#C9A959) — used only for the projected wealth curve, the fiduciary sign-off badge, and the compound-lens callout. Red and green are reserved for actual gain/loss numbers; no decorative chrome uses them.

Type

Display headlines use Cormorant Garamond — editorial, restrained, signals "concierge" rather than "trading floor." Body and UI text uses Inter at 16px minimum. Every numeral uses JetBrains Mono with tabular figures so balance columns align visually without manual padding.

Tone

Copy avoids exclamation marks, hype language, and "you can do it" cheerleading. Tone references: The Economist editorial voice, vintage Patek Philippe print ads, the language a private banker uses with a UHNW client. The implicit message is "we trust you to handle the truth."

Traditional budget apps warn the user every time they overspend. Within four weeks, the user disables notifications. Aureus replaces every "you overspent" warning with "here is a cheaper alternative + here is what the saved capital compounds into." No moral judgement. The Compound Lens does the persuasion through visualisation, not through scolding.

The standard robo-advisor presents a black box. The user gives up control to get convenience and never sees inside. Aureus is the opposite: the AI only forecasts and proposes; every commit requires explicit user sign-off; every action is logged in the append-only Activity log; every chat response cites the source data. Trust is built through visibility, not through assurance.

UHNW asset allocation is genuinely complex — multi-asset, multi-jurisdiction, multi-generational. The retail compression is to three named scenarios, one curve, one slider, one sign-off. The complexity is still underneath; the surface presents only the decisions the user actually has to make. This is the senior-PD work: deciding what to hide, not what to show.

Three production threads converged into the Aureus concept. Each one contributed a specific pattern the retail wealth-app category does not have.

From ACY Securities

Nearly five years designing under ASIC RG 268. Every commit to a regulated trading surface had to be logged, citable, and reversible. The Aureus Activity log carries that exact discipline into the retail surface, where most products treat audit as a back-office concern.

From Christie's

Solo full-stack build of the Christie's International Real Estate editorial platform — UHNW audience reading $5M–$80M luxury real estate — taught the visual grammar of restraint. Bone white, Cormorant Garamond display, no exclamation marks. The user is trusted to handle the truth. Aureus inherits this tone wholesale.

From Xanthos Private Bank concept

The B2B2C private banking research that produced Xanthos surfaced this pattern: RMs always present clients with three named scenarios, not binary choices. The Decision Room is the retail-scale port of that workflow — one private banker, replaced by an AI that does the same option-narrowing work.

This concept evidences UHNW-fiduciary-logic translation to retail: 4 AI modules (Velocity Dashboard / Alternative Finder / Event Radar / Fiduciary Decision Room), 31 mobile screens, 10-step KYC + AML onboarding citing six regulations by CFR section, working live React prototype. Regulatory anchors named: SEC Reg BI Care Obligation 17 CFR § 240.15l-1(a)(2)(ii), SEC Reg BI Conflict (a)(2)(iv), FINRA Rule 2111 Suitability, SEC Rule 17a-4(f), SR 11-7 Model Risk effective-challenge, FinCEN CDD 31 CFR § 1010.230, FATF Recommendation 10. Production foundations (ACY Securities + Finlogix + Xanthos) ground the institutional register; the retail translation is the explicit concept extension.

What this concept deliberately does not claim. Not in production — modelled outcomes, not A/B-tested at retail scale. The Alex persona is fictional; her 90-day journey is a scenario-based walkthrough, not a longitudinal user study. The 65–75% KYC completion lift cited under the FinCEN CDD section is FinCEN public data on transparent-vs-opaque KYC, not measured on this prototype — explicitly labelled in the Provenance section. No certified WCAG 2.1 AA conformance — full disclosure at the accessibility audit disclosure. No paired-within-subjects statistical study — the parallel methodology rigor for any future measured claim would follow the Finlogix methodology disclosure. No post-launch iteration data — the parallel for hypothetical production is at the ACY RG 268 iteration note. The institutional adoption pattern (verification surface as adoption mechanism) is documented at the ACY Connect political-skill note — in Aureus, the Decision Room IS the user’s verification surface against the AI’s recommendations.

The disclosure register. The four 2026-05-18 field notes are the canonical voice this concept inherits from. The five deliberately-not-built categories (no gamification, no crypto, no social, no auto-trade, no chatbot personality) are the editorial-restraint discipline that the senior-PD register requires of a B2C AI wealth product. The 1,225-word executive case study at project-aureus-executive.html is the recruiter-scan-path version of this comprehensive research record.

Portfolio thread

Aureus sits at the intersection of three portfolio threads. Follow each thread to see how the institutional pattern translates into the retail surface.

Thread

UHNW Wealth Management

From institutional private banking to retail democratisation

Thread

Fiduciary AI & Sign-off Discipline

AI surfaces options, humans hold the commit; append-only audit trails as primary nav

Thread

Editorial Voice in Finance

Concierge restraint replaces retail enthusiasm; bone white replaces neon green