INSTITUTIONAL

FINTECH · CONCEPT DESIGN◆

CONCEPT · NOT SHIPPED

TradeX Hedge Fund Portfolio Management Interface

What would a hedge fund terminal look like if you rebuilt it from scratch around the three cognitive modes a PM moves through in a trading day — rapid scan, deep investigation, execution decision — instead of inheriting Bloomberg's data-density premise?

Built from unstructured conversations with L/S equity fund managers (n=3, not a formal study).

Production bridge: ACY

Connect — FIX 4.4 institutional platform, live prime brokerage clients.

See also: TradeX

Institutional Terminal (terminal execution layer).

DESIGN

RESEARCH EXPLORATION◆

CONCEPT · NOT SHIPPEDSpeculative

prototype — no real fund data

This started from real conversations — not desk research. Over lunches with L/S equity fund

managers,

I kept hearing the same friction: terminals surface everything, but a PM's actual morning moves

through three distinct phases — rapid scan, deep investigation, then execution decision. No tool was

designed around that cognitive sequence.

TradeX is my attempt to design for that workflow. I'm not a quant. But I understand the problem from

the people who live it.

Primary Research

3 PM

interviews at L/S equity funds ($200M–$2B AUM). Topics: morning workflow, signal digestion,

position-sizing triggers.

Competitive Analysis

Bloomberg

Terminal, Refinitiv Eikon, FactSet, Palantir Foundry — evaluated for IA, workflow patterns,

and cognitive load before any screens were designed.

Design Hypothesis

A PM's morning

has 3 cognitive modes: scan → investigate → decide. Terminal should adapt to each mode, not

front-load everything simultaneously.

Scope Limits

Not a proof of

regulatory compliance, eng. feasibility, or prod. reliability. Directional artefact — read

alongside shipped ACY Connect work.

The contribution · at a glance

Product designer — TradeX Hedge Fund Manager Platform (PM-cognition concept)

A trading platform designed around the portfolio manager’s cognition — the three mental states a PM moves through, not a wall of widgets.

11

Canonical screens designed

Concept · design scope

3

PM cognitive states modelled

Scan → Investigate → Execute

4

Unmet practitioner demands

Sourced from practitioner research

5

Screen KYC & AML flow

Concept · compliance scope

n=3

Practitioner research

Informal practitioner conversations

4-tier

AI autonomy framework

Agents observe/propose · human decides

Hedge fund PMPortfolio cognitionKYC/AMLAI autonomy tiers

Concept · design study

Concept design study — figures are design scope (screens, modelled cognitive states, the KYC flow). The practitioner research is n=3 informal conversations, not a formal study; no shipped outcomes are claimed.

The full case study

The PM cognition model, the 11 screens, and the AI autonomy tiers — read in full, or stop at the summary above.

The Paradox3 Cognitive States11 Screens — Failure → DecisionKYC & ComplianceThe Hardest AI QuestionVisual LanguageBody of Work

11

Screens Designed

4

Failure Modes Mapped

3

Cognitive States Modelled

$1T+

AUM Segment Addressed

The Paradox of the Modern Institutional Terminal

A hedge fund manager in 2026 has access to Bloomberg,

FactSet, a proprietary quant stack, and six monitors. They have more data than any

trader in history. And yet — when a Taiwanese semiconductor announcement at 2am begins

rippling through their carry trade positions, neither Bloomberg nor FactSet can show

them the causal chain. Only the price move. After the damage is done.

The institutional terminal market has reached a strange

equilibrium: everything is on-screen; nothing tells you what matters right now. Bloomberg gives you the data — the synthesis, the ranking, the "what to ignore during a crisis" is left to the user. TradeX is a concept

exploration of what breaking out of that equilibrium looks like — not through

incremental feature additions, but through a fundamentally different architectural

premise.

3 cognitive states framework — Scan → Investigate → Execute

4 unmet demand categories sourced from ACY's institutional network

5-screen KYC + compliance verification flow

Visual language system — density tiers, semantic colour, keyboard-first interaction

Deliberately Not Built

Live market data — all numbers are simulated

Real FIX execution path — referenced from ACY Connect production, not rebuilt here

Validated quant models — HHI / VaR / regime classification are visualisation primitives, not statistically calibrated

User testing with named PMs — directional informal conversations only (n=3)

Regulatory certification — informed by, not audited against, MiFID II Art. 27 + SEC 17a-4

Status & Honesty

Concept design exploration · Not in production · Speculative prototype. Built from production-grade adjacent work (ACY Connect FIX 4.4, public Bloomberg architecture analysis, 3 informal practitioner conversations) — original IP, no client overlap.

Read as a research artefact, not a shipped product. Every claim is qualified by what was studied vs. what was extrapolated.

Four documented evidence sources — what was studied, not just what was concluded.

ACY Connect Production Work

Direct exposure to FIX 4.4 protocol, institutional order states

(ExecutionReport 35=8, Snapshot 35=W), and prime-broker integration on ACY's

live institutional product. Informed the execution flow design.

Bloomberg Terminal Analysis

Extended analysis of Bloomberg's publicly documented information architecture,

keyboard-command system, and panel layout — via developer docs and trial access.

Informed density and keyboard-first principles.

Informal Practitioner Conversations

Directional conversations (n=3, not structured interviews) with a PM, quant

analyst, and buy-side risk officer in ACY's institutional network, 2024.

Shaped the 3 cognitive states framework + 4 unmet demand categories.

Published Research

CFA Institute on portfolio decision-making under uncertainty · Kahneman (2011)

+ Lo & Repin (2002) on crisis-mode cognition · Visible Alpha + Coalition Greenwich

on Bloomberg/FactSet architectural limits · TauricResearch TradingAgents

(arXiv:2412.20138, 2024) on multi-agent LLM committees · Fincept Terminal v4

(37 AI agents in production) confirming committee architecture is deployable.

Honest caveat: Concept informed by research, not empirically validated.

The "4 failure modes" + "3 structural barriers" are documented patterns from these

sources, not primary-research findings.

Design Thesis

A hedge fund terminal should adapt to the manager's cognitive state — not force the manager to adapt to the terminal's data model.

01 — DECISION

Conclusions before evidence

Surface what the system concluded first. Present the supporting data second. Managers should challenge synthesis — not perform it.

02 — DECISION

Explainability over efficiency

Every AI signal shows its reasoning chain. At no AUM level is "the model said so" an acceptable answer — especially at the execution boundary.

03 — DECISION

Decision and action in one space

Context-switching between analysis and execution is where alpha leaks. Every view connects directly to the execution pathway it naturally leads to.

1. What Hedge Fund Managers Actually Want

Current platforms give managers data. What they want is intelligence that maps

causation, not just correlation. These four gaps came up consistently across

the PM conversations that shaped this project — not from literature reviews:

"Bloomberg tells me what happened. It doesn't tell me what to do about it." — paraphrased

from a fund manager conversation, 2024

⚡

Causal Transmission Maps

When a geopolitical event fires, show

how it propagates through supply chains, FX, and CDS spreads into specific portfolio

positions — in real time, before the price moves. Managers need causation: "Oil

spike → EM currency stress → long carry unwind" on-screen while they can

still act on it.

Liquidity Stress Visualization

"If I unwind 5% of this position right

now, what's the market impact cost?" Modern markets collapse to zero liquidity in

milliseconds during stress events. Historical ADV calculations fail entirely in

crisis conditions. Managers need forward-looking slippage simulation, not

backward-looking averages.

Real-time Alpha Attribution

One button: how much of today's P&L

is market beta, how much is factor exposure (AI thematic, rate sensitivity), and how

much is genuine manager alpha? LP pressure on fees has made attributable skill vs.

luck the central accountability metric — and no current platform surfaces this in

real time.

GenAI Shadow Portfolio Stress Test

Simulate 10,000 extreme but

plausible scenarios — "AI capex collapses 50% by year end," "Taiwan Strait

crisis, 72-hour duration" — and receive position-specific hedge recommendations. The

key word is plausible: not random noise, but scenarios a thoughtful CIO would

actually convene a meeting to discuss.

2. One User, Three Cognitive States

This framework didn't come from a UX textbook — it emerged from a pattern that surfaced

in every PM conversation: managers described not one morning workflow but three distinct

mental modes in a single trading day, each requiring completely different information and

interaction primitives. The terminal was ignoring that entirely.

State 01 · Pre-Market

Strategic Mode

6:30 – 9:30am

Calm,

deliberate. The manager reviews overnight developments, reads research briefs,

calibrates the day's positioning. Attention is broad and exploratory — they want

to understand the portfolio's shape before engaging any individual position.

UX implication: Portfolio overview

first. Macro signals relevant to the day's thesis. No individual position noise

until the manager chooses to drill down.

State 02 · Live Event

Crisis Mode

Event-triggered,

seconds matter

An announcement

breaks. A position moves 4% in 90 seconds. Cognitive tunnel vision narrows to a

single question: what is my exposure and how do I act? The manager

cannot process narrative or discovery — they need impact visibility and an

execution pathway with zero context-switching.

UX implication: One prioritized signal,

maximum visibility. Risk exposure for affected positions. Direct path from

analysis to execution — no navigation required.

State 03 · LP Reporting

Narrative Mode

Monthly / quarterly

cycle

The manager

must reconstruct the period's story — not just P&L, but why. How

much return was genuine alpha vs. beta vs. factor exposure? LPs under fee

pressure demand this answered clearly. The same interface that worked for crisis

must now support retrospective narrative construction.

UX implication: Attribution clarity.

Period performance decomposed into alpha / beta / factor split. Exportable

narrative framing, not raw data tables.

Most institutional

terminals are designed for State 01 — calm,

expert browsing. They fail in State 02 because

they were never designed around crisis-response psychology. They provide almost no

support for State 03 because attribution data

lives in a separate system. TradeX's five views are each anchored to one of these

cognitive states.

3. Why Nobody Has Built This Yet

The gap isn't imagination or ambition. It's three structural barriers that have resisted the

entire industry's attempts — and each one has a design implication that cannot be ignored:

A. The Data Silo Problem

Macro data lives in one system.

Alternative data — satellite imagery, credit card flows, shipping manifests — lives

in another. Internal research notes are in PDFs. Building real-time causal

relationships across these requires enormous compute and data-cleaning

infrastructure. Incumbent platforms were architected before cloud-native pipelines

existed; rebuilding them is harder than starting over.

Design implication: the interface must

surface data source confidence alongside every insight. A signal derived from three

independent data streams is not equivalent to one derived from a single API. The UI

must show where the signal came from. A signal derived from three independent data streams carries a different weight than one from a single API. Each signal in TradeX surfaces its source (proprietary edge, market data, third-party), its refresh latency, and model agreement — the user sees the reasoning, not just the conclusion.

B. The Black Box Paradox

Quant models are by definition

opaque. But when a fund is down 8% and a manager needs to explain it to LPs by end

of day, "the model said so" is not an answer. Finance has zero tolerance for AI

hallucination — which means every AI-powered recommendation must carry an

explainability layer before any institutional player will trust it with live

capital.

Design implication: this is the same

problem addressed in Nova, at institutional scale. The explainability UI pattern —

showing reasoning chains, not just conclusions — is non-negotiable regardless of the

sophistication of the underlying model.

C. The Proprietary Data Wall

A fund's edge lives in its

proprietary signals — internal alpha research, exclusive data partnerships, bespoke

factor models. No fund will integrate these into a third-party SaaS platform where

the data could leak, be used to train competitor models, or expose methodology. This

means any platform that aggregates the full intelligence stack must offer on-premise

deployment with air-gapped data architecture — which eliminates most modern SaaS

economics.

Design implication: the UI must make data

provenance visible at every level — what is proprietary, what is market data, what

is third-party alternative data. The manager needs to know which parts of the system

see their edge and which parts don't.

4. Where Current Tools Fall Short

Understanding the landscape reveals why the gap persists — and which parts of the problem

TradeX's design specifically addresses:

Platform Type

Examples

Core UX Limitation

Legacy

Terminal

Bloomberg,

FactSet

Data-complete

but intelligence-absent. Architecture predates cloud-native AI pipelines by

two decades. Steep learning curve designed for specialists. Modern UX is

bolted on, not native.

Modern

Web Platform

Koyfin,

TradingView

Strong equity

UI, insufficient depth for derivatives, fixed income, and structured

products. Not built for the multi-strategy complexity of hedge fund

operations. Strong for retail, insufficient for institutional.

AI-Driven Search

AlphaSense,

Finchat

Excellent at

text-based research synthesis and document analysis. Not designed for

real-time portfolio monitoring, position management, or execution workflow

integration. Answers questions; doesn't support live decisions.

"Managers don't need more data. They need a system that connects their internal research

notes, external market data, and live risk models into a single reasoning layer — an

agentic workflow that thinks alongside them, not one they have to query."

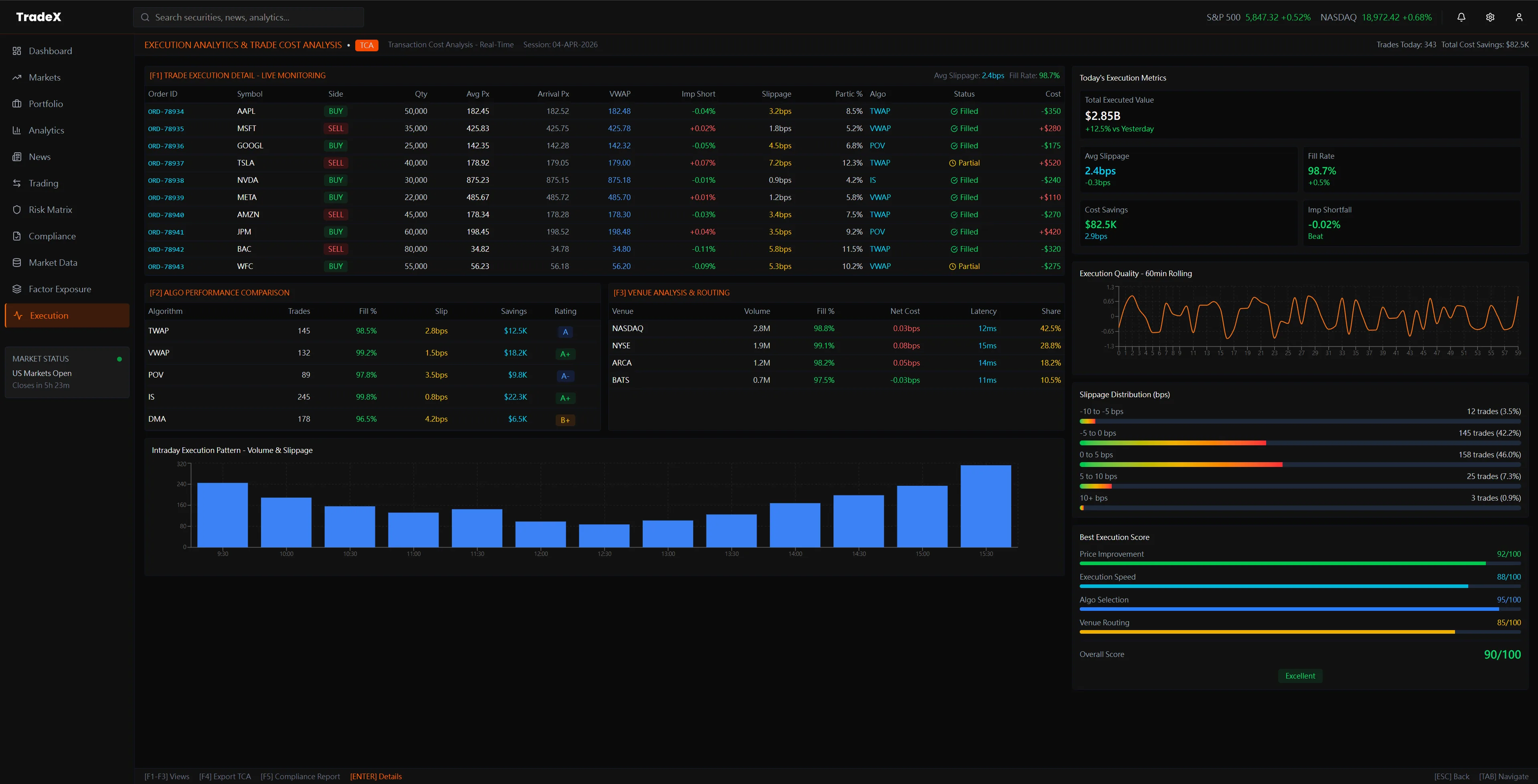

5. The Screen System — Design Decisions Behind Each View

Each view in TradeX is built around a specific failure mode in current institutional

interfaces. The design decisions aren't aesthetic — they are structural responses to

documented workflow breakdowns under real market conditions.

11 Screens · Failure → Decision at a glanceScan first, deep-read selectively below

#

Screen

Failure mode it solves

Core design move

01

Live Markets

Equal visual weight collapses signal-to-noise during volatility

AI-selected single focus chart + portfolio-relevant watchlist

02

Portfolio Management

Position table forces mental reconstruction of structural exposure

Vertical allocation lead, position table as supporting evidence

03

Portfolio Analytics

Risk + exposure + compliance live in three separate tools

Single view with synchronised risk · exposure · compliance lenses

04

Market News & Insights

News flood with no relevance filter to current book

Position-aware filtering, surface impact-on-book first

05

Trading Desk

Execution UX taxes cognition right when stakes are highest

Compliance checks are out-of-band, after-the-fact, blame-assigning

Pre-trade compliance overlay rendered inline with the trade ticket

07

Fund Performance & Risk

Period-over-period diffs scattered across exports + slide decks

Comparative intelligence in one view — book-level + strategy-level rolled up

08

Institutional Dashboard

Alpha attribution lives in quarterly reports, not in the trading day

AI-driven attribution + hedge fund signal flow surfaced at session open

09

Institutional Screener

Single-panel screening forces tab-switching for cross-asset views

Multi-panel screener with synchronised cross-asset filters

10

Factor Analysis

Factor decomposition is post-hoc, recomputed in spreadsheets

Live factor decomposition across asset classes, recalculated on filter change

11

Factor Exposure & Concentration

Concentration breaches surface only after the audit, not in the moment

Real-time HHI & factor exposure with pre-breach amber alerts

Each row below expands the row above with the failure mode, the design decision, the outcome it produces, and the tradeoff accepted. Click any anchor to jump.

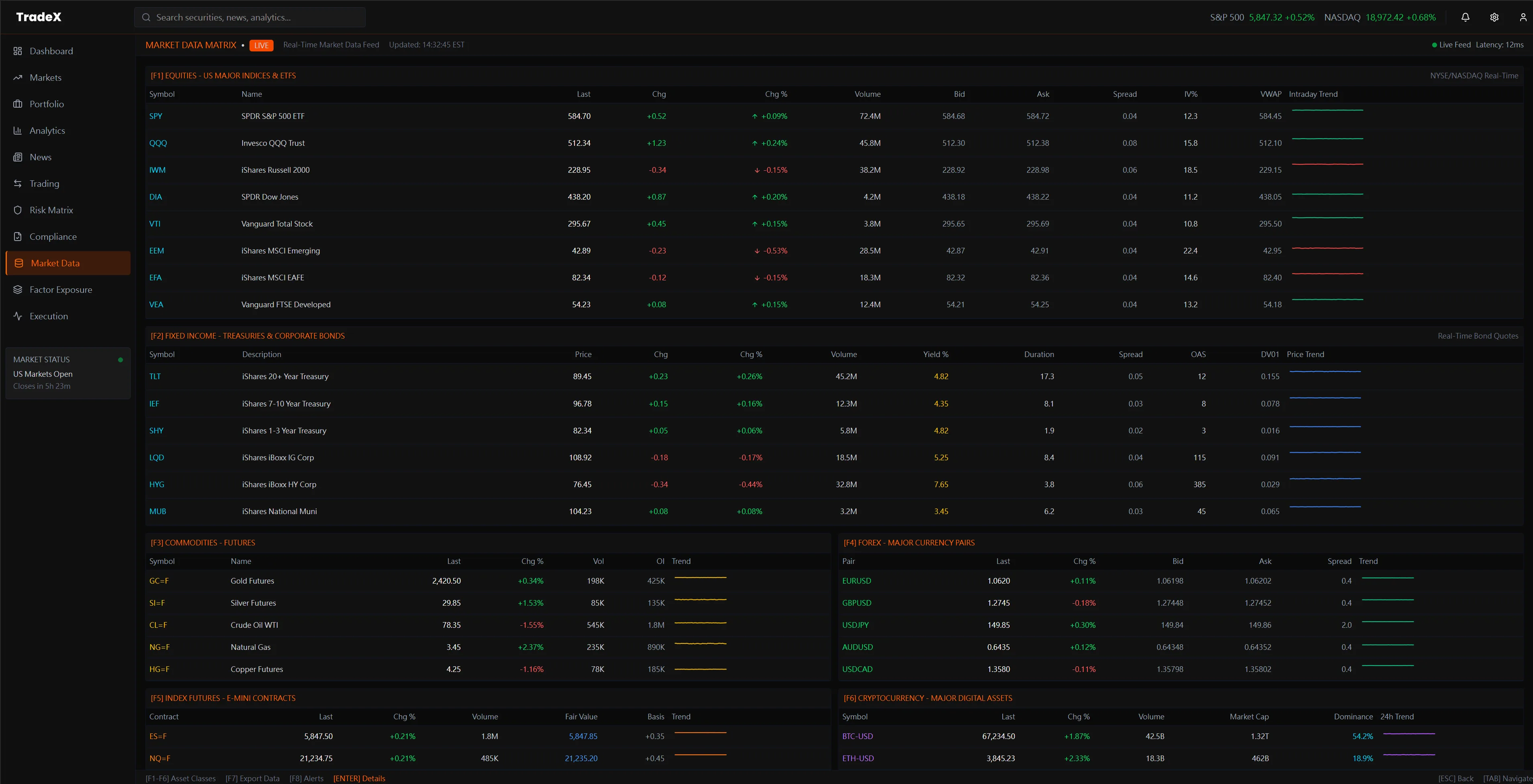

SCREEN

01

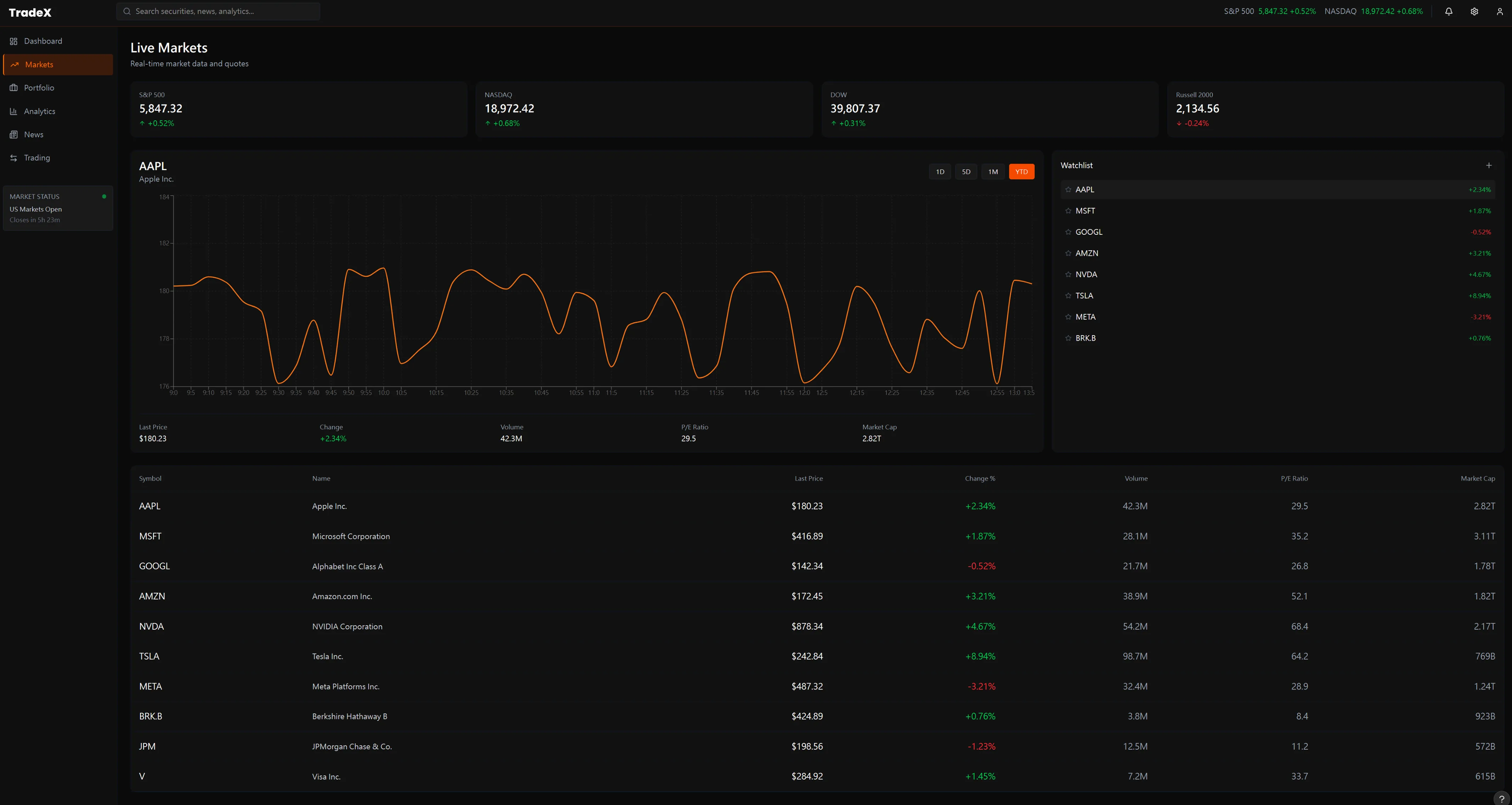

Live Markets — Information at

Institutional Speed

The Failure Mode

Legacy terminals present every

asset simultaneously at equal visual weight. During volatility, signal-to-noise

collapses — everything is urgent, so nothing is urgent. The manager's attention

is not directed; it is simply overwhelmed.

The Design Decision

TradeX anchors on a single

AI-selected focus chart with a portfolio-relevant watchlist. This provides

Cognitively Ergonomic Expert Density — surfacing the highest

monitoring priority at that moment rather than overwhelming with raw breadth.

Context-first, market-second.

Outcome → Cognitive triage shifts from the manager to the system. During volatility the PM arrives at the single highest-priority signal — not a full board requiring manual prioritisation under time pressure.

Tradeoff accepted: Sacrifices breadth for depth of attention on entry. Assumes the AI's priority model is trustworthy enough to delegate the first-pass triage — a hypothesis that needs live validation with real fund data.

SCREEN

02

Portfolio Management — From AUM

to Position Clarity

The Failure Mode

Most portfolio views lead with a

position table — a flat list of tickers and numbers that requires the manager to

mentally reconstruct concentration, correlation, and structural exposure. This

is cognitive assembly work the interface should do.

The Design Decision

TradeX leads with vertical

allocation

analysis and monthly performance — structural signals before positional

detail. The design applies Cognitively Ergonomic Expert Density

by making the position table the evidence that supports the visual

conclusion, not the starting point. At $10M+ AUM, the fund's shape matters more

than any single ticker.

Outcome → The manager understands portfolio shape before engaging any individual position — compressing the time from "terminal opens" to "I know what I need to act on today."

Tradeoff accepted: Visual hierarchy imposes an opinionated reading order. A PM who wants to start from an individual ticker must navigate one level down — a deliberate friction that protects against confirmation-bias-driven position sizing.

SCREEN

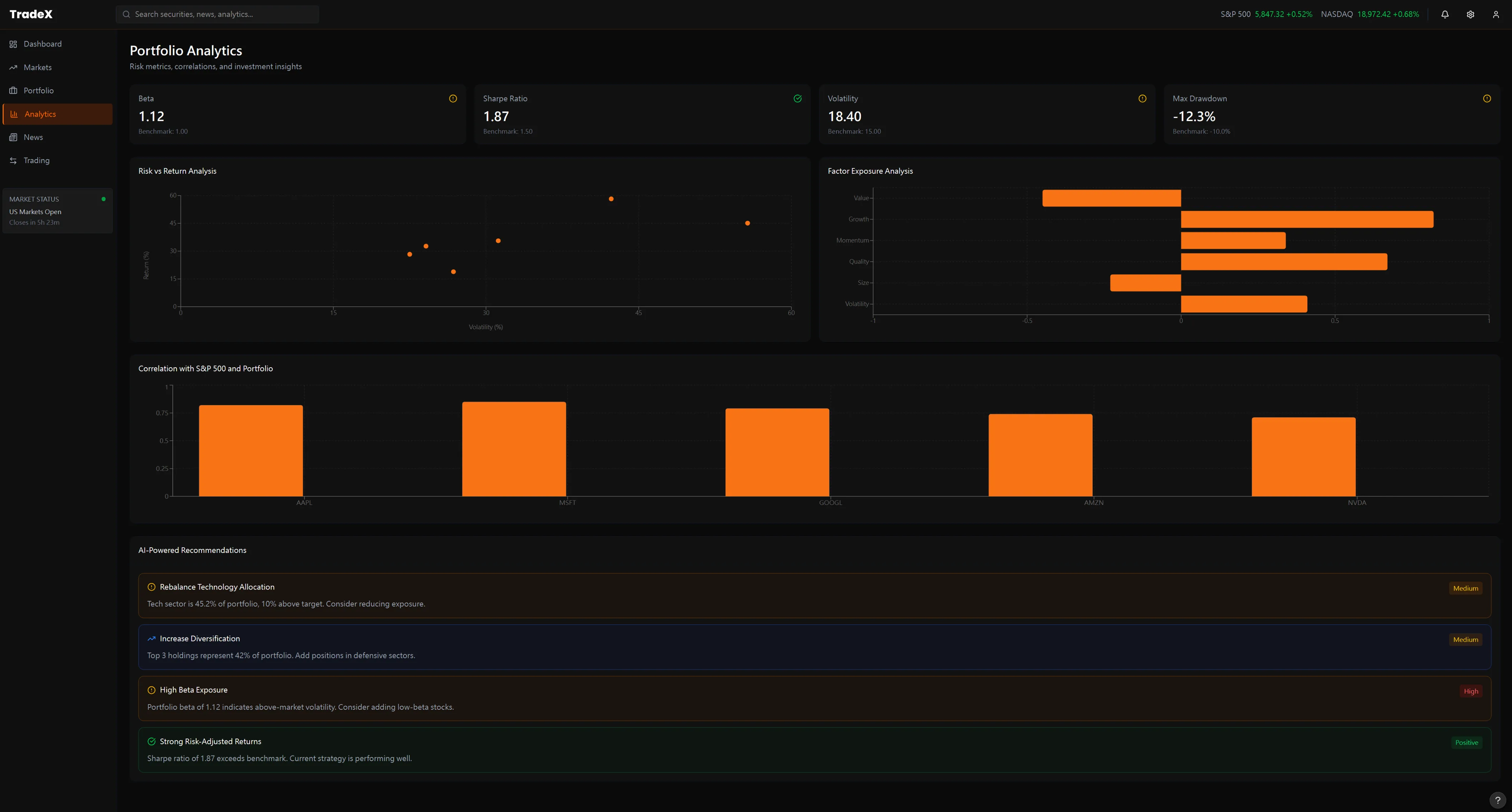

03

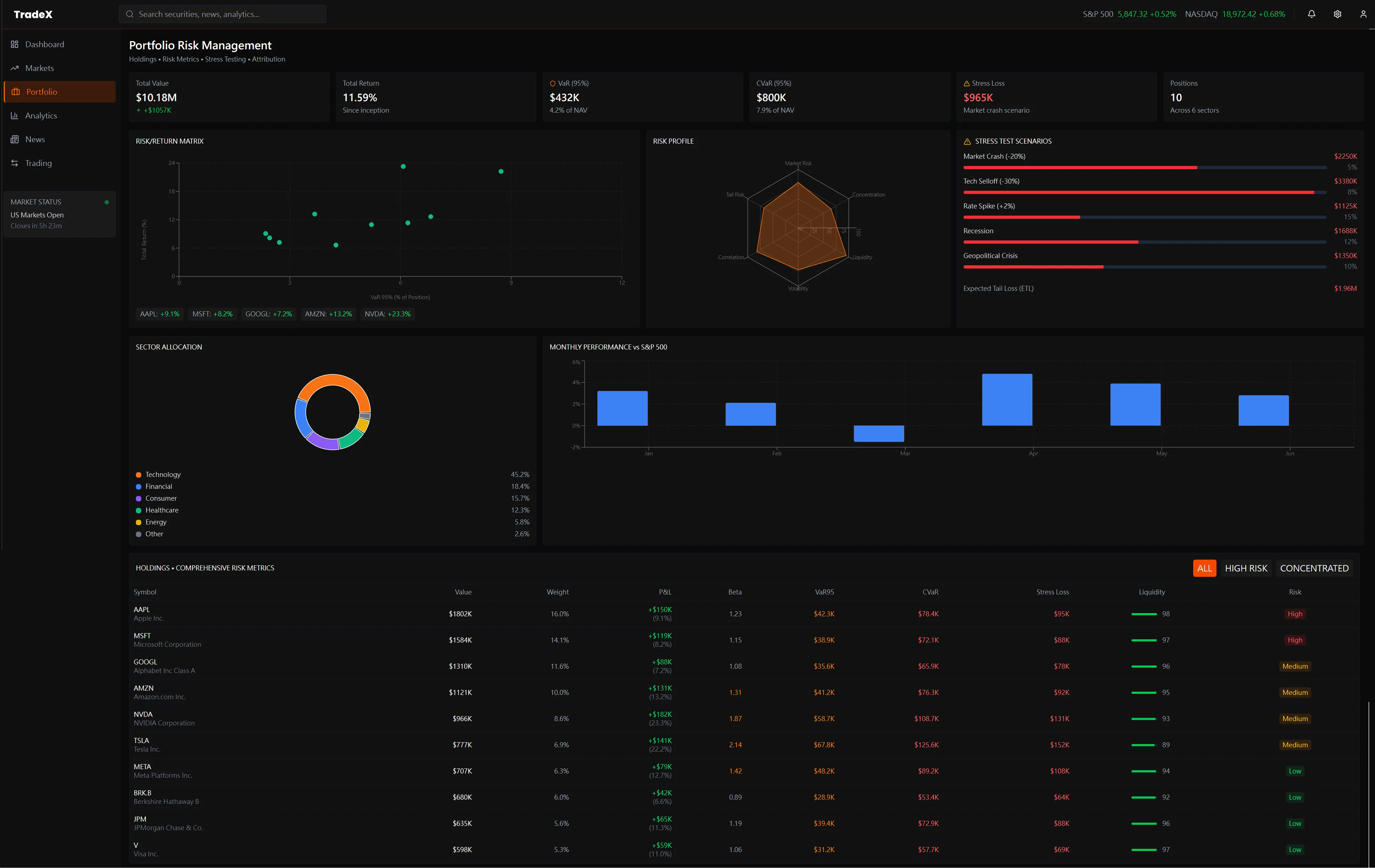

Portfolio Analytics — Risk,

Exposure, and Compliance in One View

The Failure Mode

Risk metrics (beta, Sharpe,

drawdown), options Greeks exposure, and compliance tracking live in completely

separate modules — often separate tabs or windows. Monitoring all three

simultaneously requires constant context-switching that destroys the manager's

ability to see the relationship between them.

The Design Decision

The analytics view treats

risk/return, options exposure, and compliance as a unified panel — each is a

lens on the same portfolio state. AI recommendations at the bottom surface

anomalies the system has already identified across all three dimensions, so the

manager reviews conclusions rather than assembling them from fragments.

Outcome → A VaR breach is immediately contextualised against options exposure and compliance status in the same glance — eliminating three separate system lookups and the manual reconciliation between them.

Tradeoff accepted: Unified density requires a larger display and higher cognitive investment to read the full panel. Appropriate for the institutional context; would be hostile UX on a retail or mobile surface.

SCREEN

04

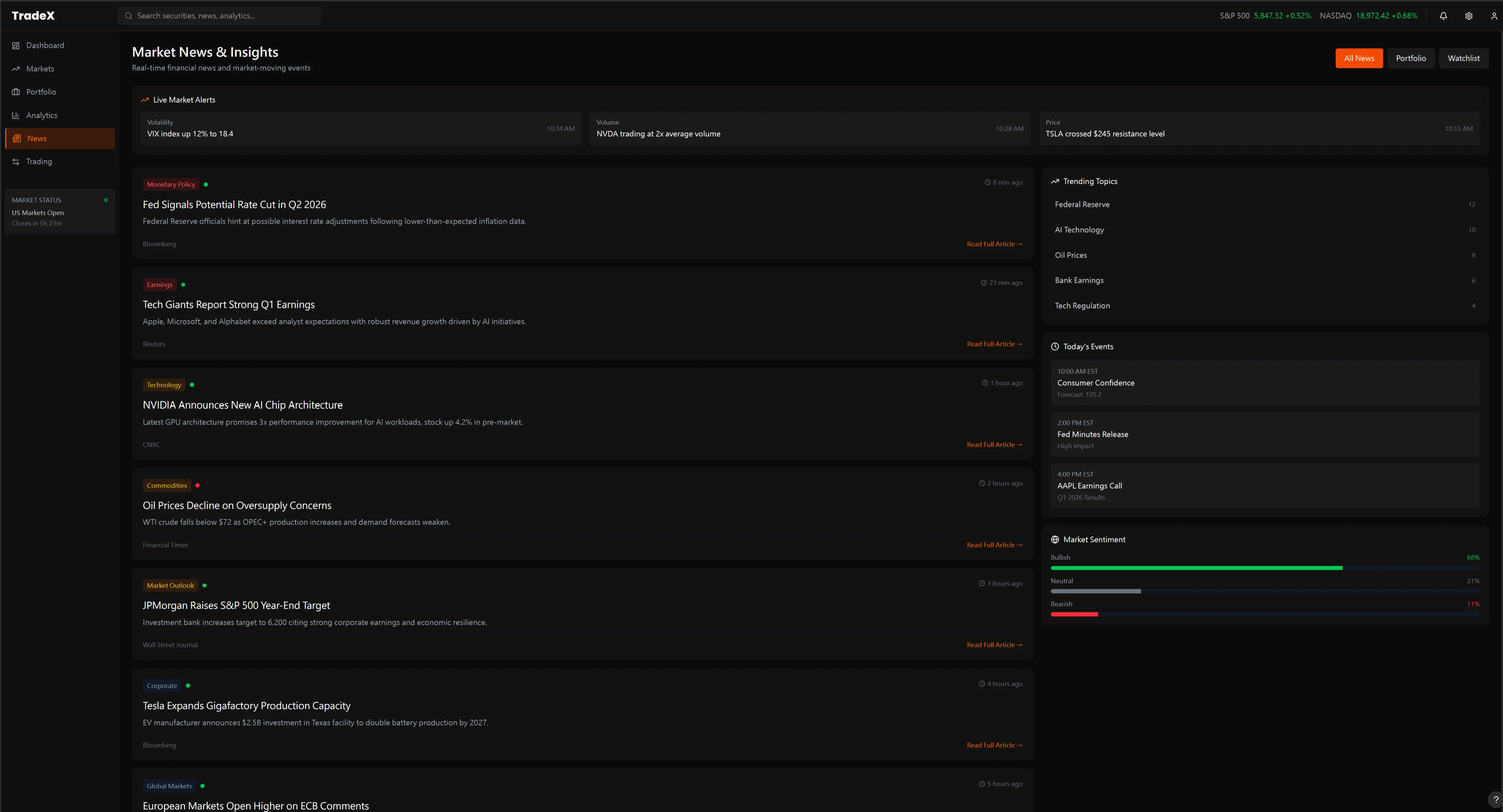

Market News & Insights —

Signal vs. Noise at Scale

The Failure Mode

A hedge fund manager receives

hundreds of news items per hour. Chronological feeds with categorical tags

require the manager to personally assess relevance to their specific book — a

task that consumes hours of attention and produces both false positives (noise

treated as signal) and false negatives (real signals buried in the feed).

The Design Decision

TradeX's news view features

real-time thematic sentiment analysis on the right panel — market mood by theme,

not just by asset class. News items are pre-filtered for portfolio relevance.

The manager's attention is directed toward articles the system has already

mapped to open positions, not the full firehose.

Outcome → News consumption shifts from scanning a full feed for personal relevance to reviewing a curated shortlist already mapped to open positions. The manager reads 20 articles with 90% relevance instead of 200 with 9%.

Tradeoff accepted: Portfolio-mapped filtering creates confirmation bias risk — the system may amplify information that reinforces current positions over information that challenges them. A contrarian override mode would be needed in a production build.

SCREEN

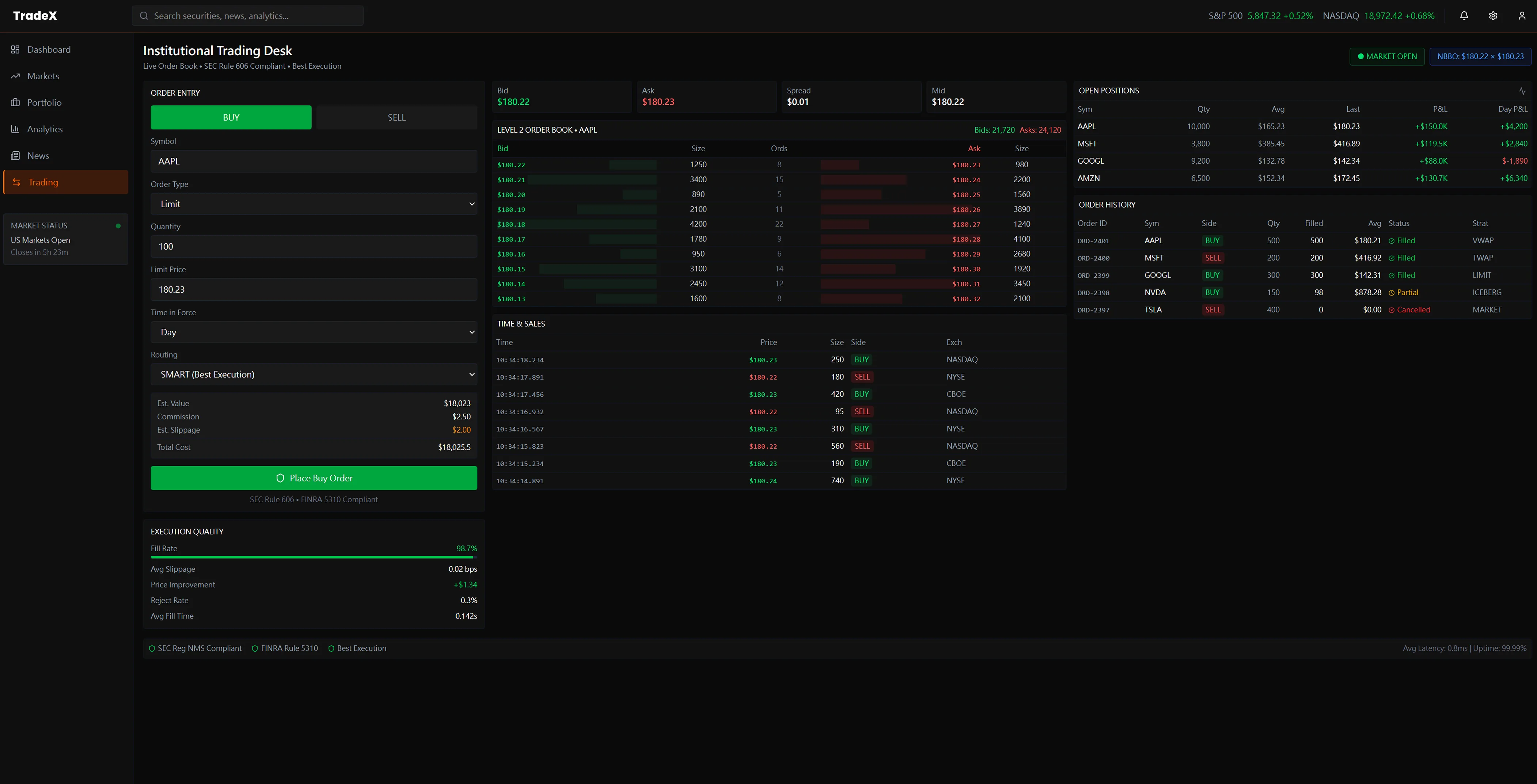

05

Trading Desk — Execution Without

Cognitive Cost

The Failure Mode

Execution interfaces are typically

separate from analytics. A manager who decides to adjust a position must leave

the analytics view, open the execution module, re-enter the position context,

confirm ticker and sizing — while the market continues to move. Friction at the

decision-to-action boundary is where alpha leaks invisibly.

The Design Decision

The trading desk is directly

connected to open positions — clicking any portfolio position pre-populates the

order panel. A portfolio impact preview shows estimated post-trade allocation

before execution confirms. Decision and action occupy the same cognitive space,

minimizing the latency between conviction and execution.

Outcome → Decision-to-execution latency drops because the order panel is pre-populated from the position the PM was already analyzing — no context re-entry, no ticker lookup, no cognitive reset mid-trade.

Tradeoff accepted: Tight analytics-execution coupling means any error in position state propagates directly into the order panel. The design trusts the portfolio data layer — which requires a real-time, authoritative position feed to be reliable.

SCREEN

06

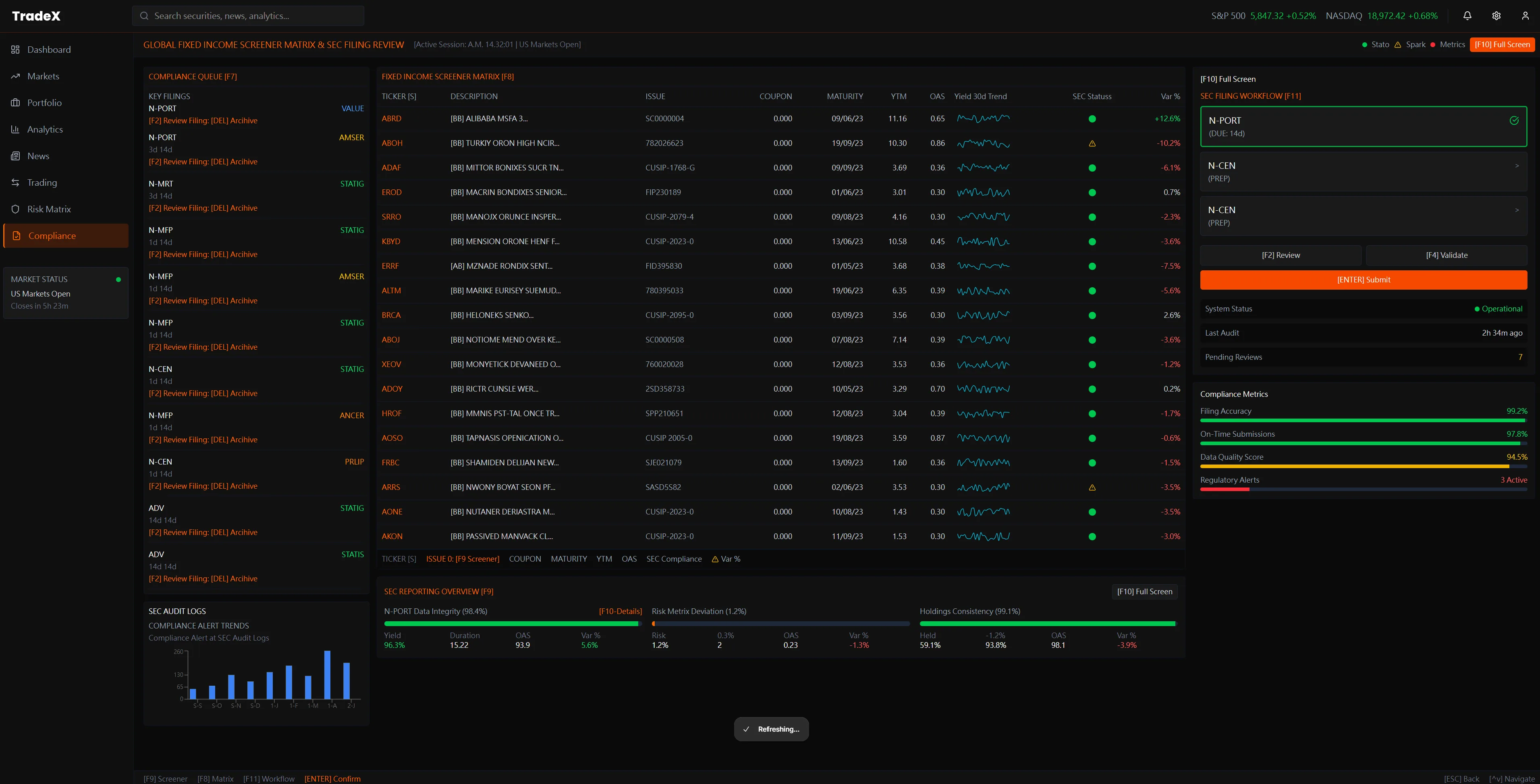

Compliance Screener — Regulatory

Intelligence in the Trading Layer

The Failure Mode

Compliance screening lives in a

separate back-office system. Fund managers and compliance officers must

context-switch between trading terminal and regulatory tools — often with a

24-hour data lag. Violations surface after the position is taken, not before. At

LP reporting time, reconstructing the compliance audit trail requires hours of

manual assembly from siloed systems.

The Design Decision

TradeX embeds a live compliance

screener directly in the terminal: a filterable matrix covering 60+ screening

criteria, position-level regulatory status, and SEC filing health — all updated

in real time alongside live price data. The right-panel filter system lets

compliance officers apply multi-criteria screens without leaving trading

context. Data provenance (which feeds are proprietary vs. market data) is

visible at every row.

Outcome → Compliance runs pre-trade, not post-settlement. Orders that breach concentration limits or disclosure windows don't execute — the violation blocks the order in milliseconds. No discovering breaches three weeks later in the audit.

Tradeoff accepted: Real-time compliance requires the data feed to be both accurate and low-latency. Stale compliance data is worse than none — it creates false confidence. This design only works if the underlying feed is production-grade.

SCREEN

07

Fund Performance & Risk Analytics

— Comparative Intelligence Across the Book

The Failure Mode

Comparative analytics across a

multi-strategy book require custom Excel models or back-office reporting cycles.

By the time a fund manager sees the cross-fund Sharpe comparison or the

stress-scenario performance matrix, the market conditions that generated those

numbers have already changed. There is no live view of how all funds in the book

relate to each other simultaneously.

The Design Decision

This view surfaces 30+ funds

side-by-side with live performance metrics (Return, Alpha, Beta, Sharpe) in a

scannable density matrix — the left panel. The right panel runs in parallel:

Sector Allocation bar chart, Stress Test scenarios (Stress / Crisis / Montreal),

Regional Exposure concentration, S&P 500 correlation, and EUR/USD sensitivity.

Each panel updates live. The manager sees the book's shape and its macro

exposures at the same glance.

Cross-Project Connection: This view is the

intelligence-first evolution of the Portfolio Risk Matrix in

TradeX

Institutional Terminal

— where 960 data points (80 funds × 12 metrics) are organized for sub-second

scanning. The institutional terminal establishes the density architecture; the hedge

fund screen adds live macro correlation panels that update as conditions shift.

Outcome → Cross-fund comparative intelligence — Sharpe, Alpha, Beta, stress scenarios, regional exposure — becomes a live view rather than a monthly Excel exercise. The PM sees the book's shape and its macro exposures simultaneously.

Tradeoff accepted: Displaying 30+ funds in a density matrix requires strict visual discipline — any additional data column degrades scanability. The design deliberately excludes several metrics available in back-office systems to protect the scan speed.

SCREEN

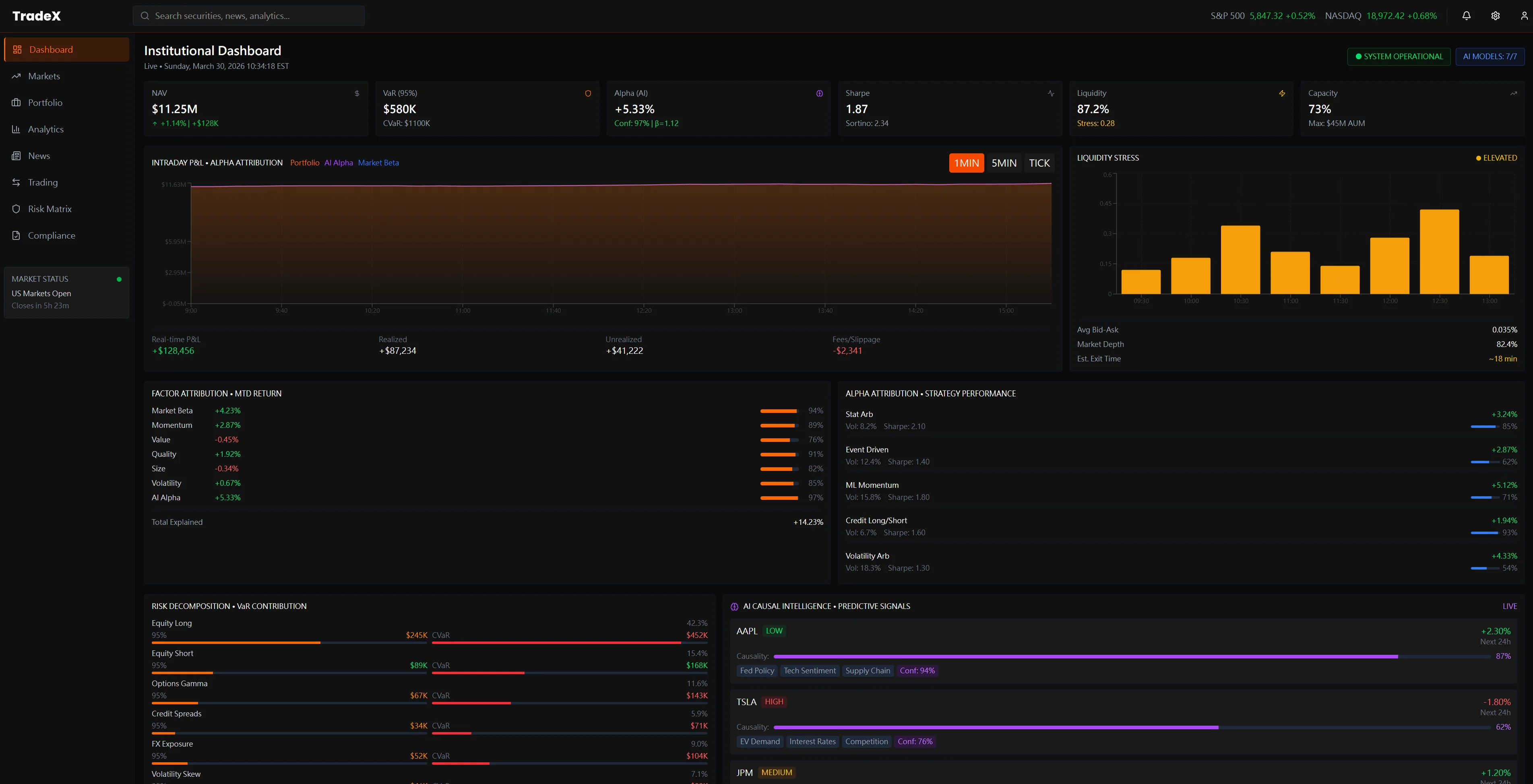

08

Institutional Dashboard — Alpha

Attribution & AI-Driven Hedge Fund Signals

The Failure Mode

Alpha attribution — the LP's core

question of "how much of this return is genuine manager skill vs. beta vs.

factor exposure?" — currently requires a multi-step monthly process. No current

terminal shows intraday attribution live. Managers face LP pressure on fees with

no real-time tool to demonstrate skill, only backward-looking monthly

decompositions assembled from multiple systems after market close.

The Design Decision

The Institutional Dashboard is the

State 03 (LP Reporting) view built for State 02 (live market) refresh rates.

Intraday P&L ($11.2M) is decomposed live into its attribution curve. The Alpha

Attribution panel shows constrained dynamic analysis in real time. At the

bottom, the AI-Driven Intelligence module surfaces hedge fund signals — AMS and

TPOE streams — giving the manager both the performance number and the

intelligence layer that explains it, simultaneously.

$11.2M

Total PnL Live

87.2%

Attribution Clarity

AI

Signal Intelligence

Outcome → Alpha attribution — the LP's core accountability question — becomes a live intraday view rather than a backward-looking monthly decomposition. Managers can demonstrate skill in real time, not just retrospectively.

Tradeoff accepted: Live attribution requires a real-time factor model with sub-minute refresh. The complexity of implementing this correctly is significant — the design sets the UX target, but the data engineering required to deliver it is non-trivial.

SCREEN

09

Institutional Screener —

Multi-Panel Market Intelligence in One View

The Failure Mode

Institutional managers currently

switch between 3–4 separate terminal windows to cross-reference equity

positions, factor exposure, trading performance, and sector allocation. No

unified screener exists that surfaces all four simultaneously —

cross-referencing requires manual cognitive assembly across disconnected panels,

introducing both latency and error.

The Design Decision

TradeX's Screener consolidates

Equity Type Media (full long/short position analytics), Factor Type Media

(factor exposure by position), Trading Performance (concentration metrics:

$2,858 total, 66.7% attribution), and Sector Allocation into one coherent

multi-panel layout. Cross-referencing equity vs. factor vs. sector becomes a

single-screen read — a 4-window task collapsed to zero switching cost.

SCREEN

10

Factor Analysis — Live

Decomposition Across Asset Classes

The Failure Mode

Factor attribution in current

terminals is a post-trade construct — PMs see factor exposure in morning reports

generated after market close, not during live market hours when it could

influence execution decisions. By the time a factor tilt is visible, the

position is already built and partially or fully filled.

The Design Decision

Live factor decomposition across

Prime Type Media equity positions, Factor Type Media (long/short split), and

Transaction Type cross-referenced simultaneously. The PM sees factor tilts as

positions are being built — not as a retrospective audit. Rebalancing becomes a

real-time decision, not a corrective morning action.

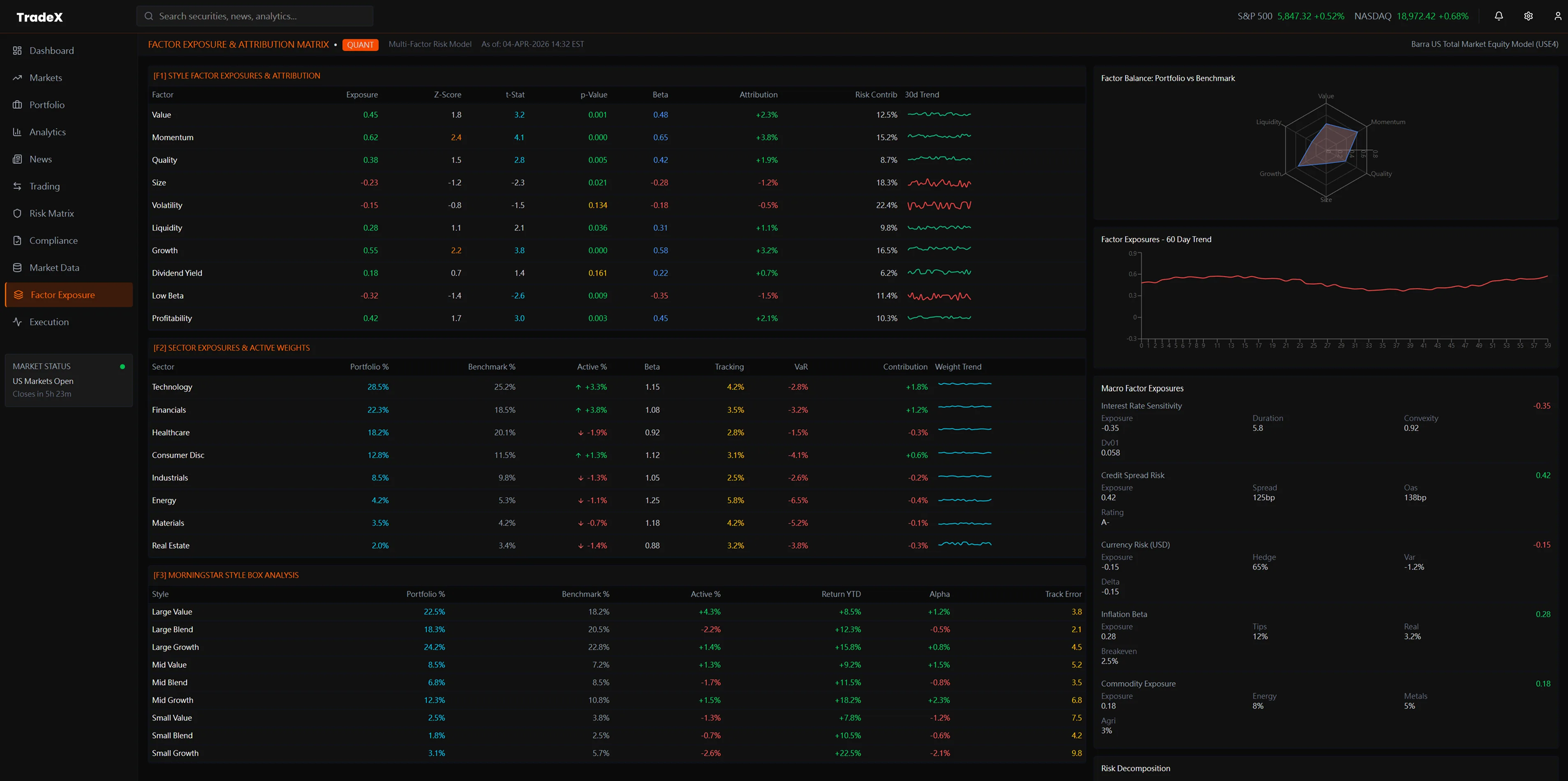

SCREEN

11

Factor Exposure & Concentration

Risk — Before the Breach, Not After

The Failure Mode

Concentration risk alerts in

current systems are threshold-triggered — the flag fires after the position has

been built and the exposure already exists. Risk managers receive alerts when

the problem has materialized, not while there's still room to adjust

construction. The 90-day trend that would have predicted the breach is never

surfaced proactively.

The Design Decision

Three visualisations working

together: the Factor Balance radar chart (portfolio shape vs. benchmark), a

90-day Factor Exposure trend line (directional drift, not snapshot), and the

Macro-factor Exposure grid. Sector-level beta exposures (Technology, Financials,

Healthcare, Consumer Discretionary) are visible as concentration accumulates —

making the breach preventable, not just auditable.

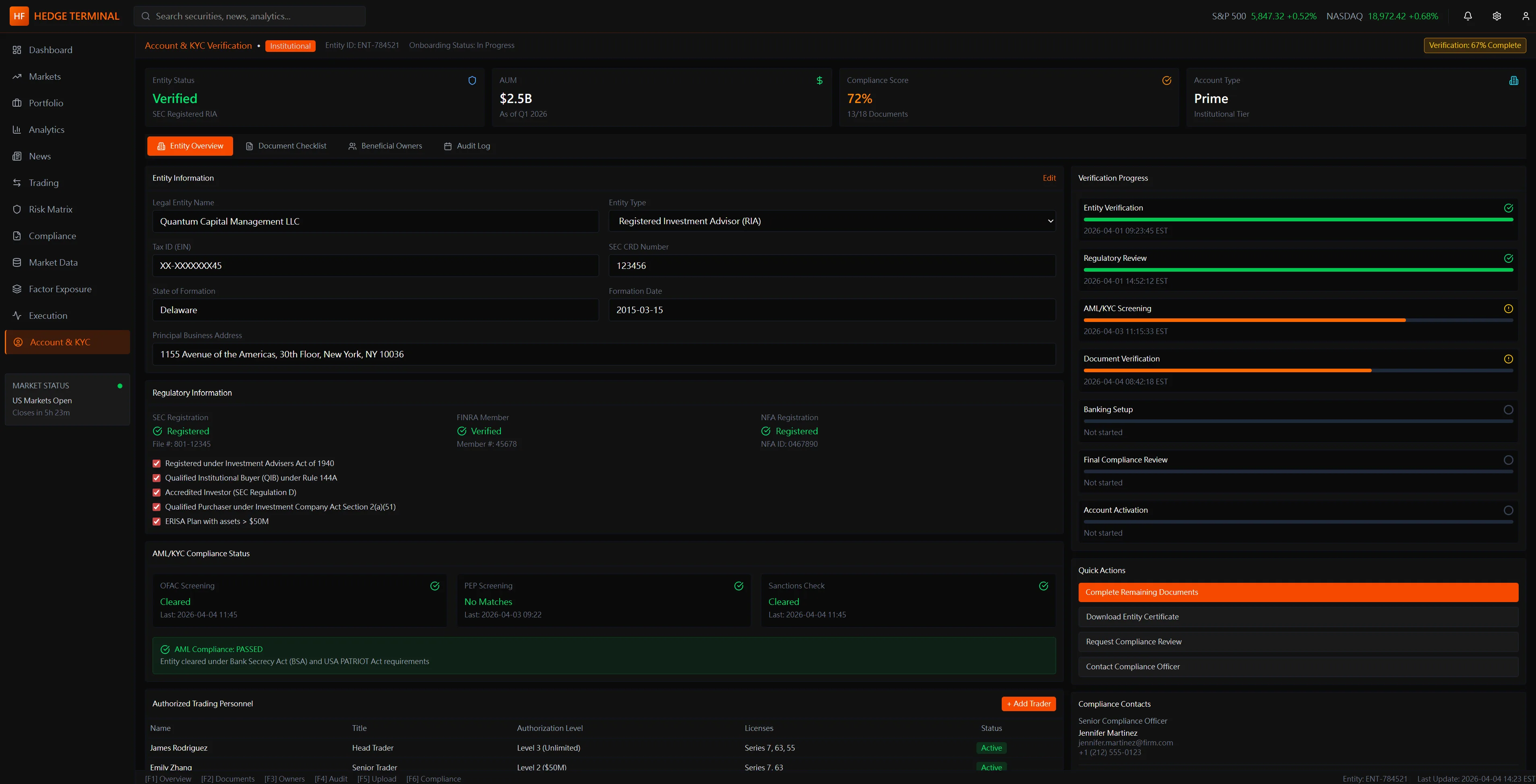

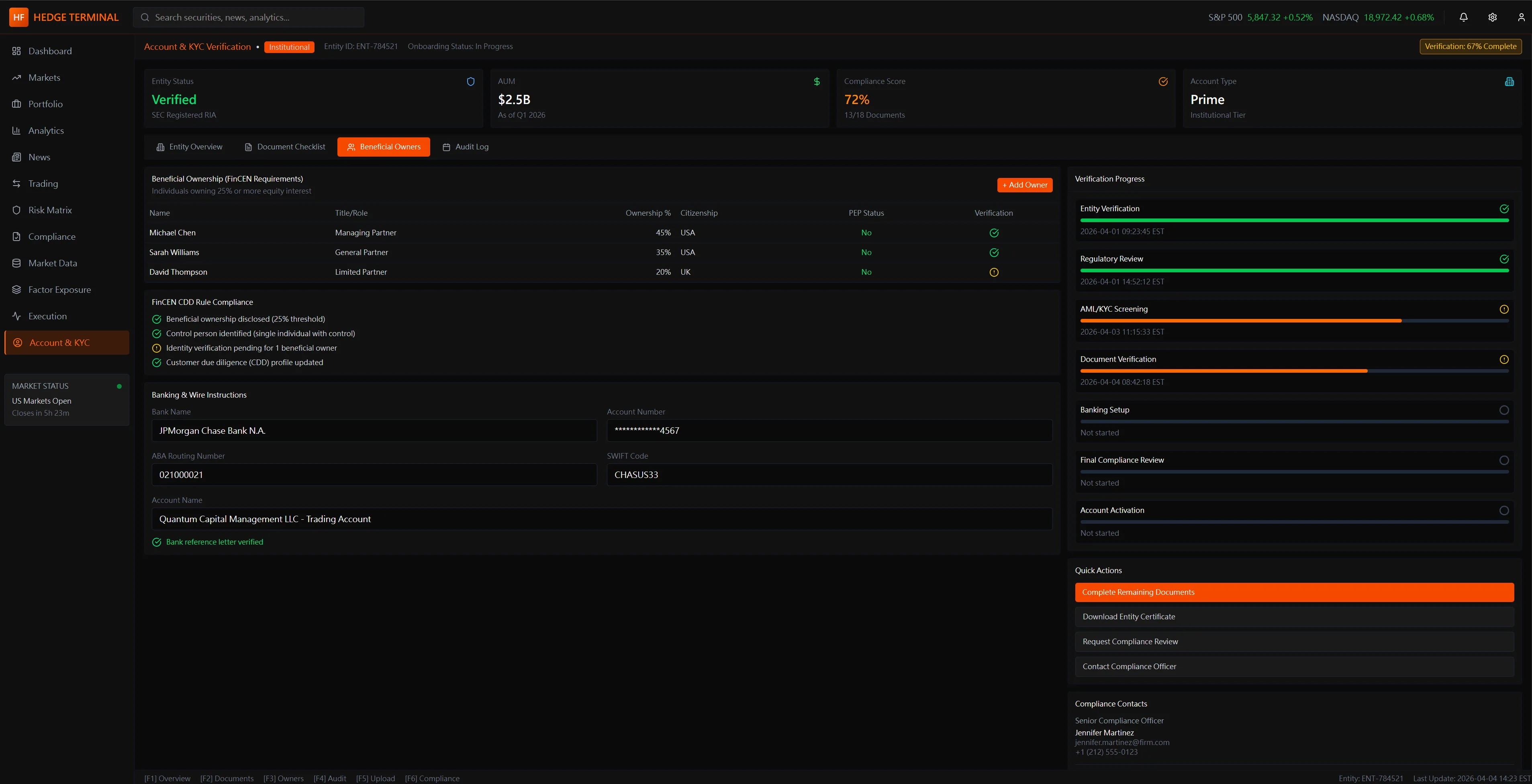

Institutional onboarding at a hedge fund level involves regulatory verification that no

consumer-grade KYC flow handles — RIA registration, FINRA compliance, AML/CDD

requirements, and multi-party document attribution across auditors, legal counsel, and

prime brokers. TradeX's KYC system is designed as a four-tab compliance

workspace, not a simple form: every verification step has live progress

tracking, document status, and a direct audit trail for regulatory review.

SCREEN

12 · TAB 1

KYC Core Overview — Firm Profile,

Status & Verification Progress

The Failure Mode

Institutional KYC at the RIA/prime

broker level is managed across disconnected email chains, PDF submissions, and

manual compliance officer checklists. The firm has no single view of where their

account stands across the 7 verification stages — status is opaque until a human

responds, creating onboarding timelines measured in weeks, not days.

The Design Decision

A persistent right-panel

Verification Progress tracker surfaces real-time status across all 7 stages

simultaneously — Entity Verification through Account Activation. The firm

identity (RIA registration, ADA, CRD, jurisdiction) anchors the left panel. The

compliance officer and the fund manager share the same source of truth,

eliminating the "what's the status?" email loop entirely.

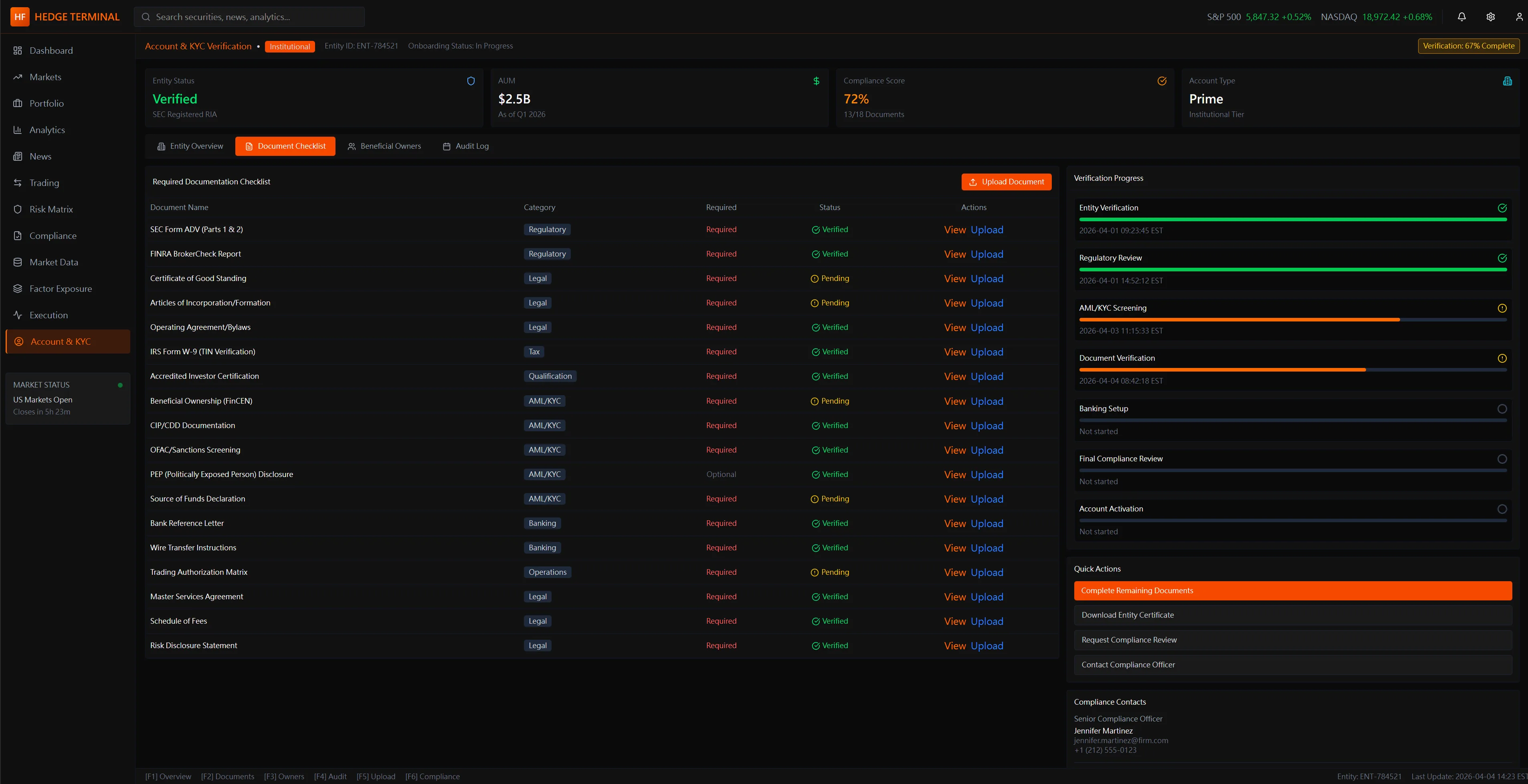

TAB

2Document

Checklist

Live status per document (Approved / Review / Pending / Completed) — ADV Parts 1&2,

FINRA registration, Certificate of Good Standing, Articles of Incorporation, and 20+

regulatory documents tracked in one view. Quick Actions panel enables direct

escalation to compliance officer without leaving the interface.

TAB

3Business

Details & AML Compliance

FinCEN CDD AML compliance status per entity relationship type (Managed / Licensed /

Limited Partners). Banking & wire institution linkage (JPMorgan Chase, ABA routing)

with legal entity chain. The tab ensures AML compliance is entity-level, not

account-level — a structural requirement at the prime broker tier.

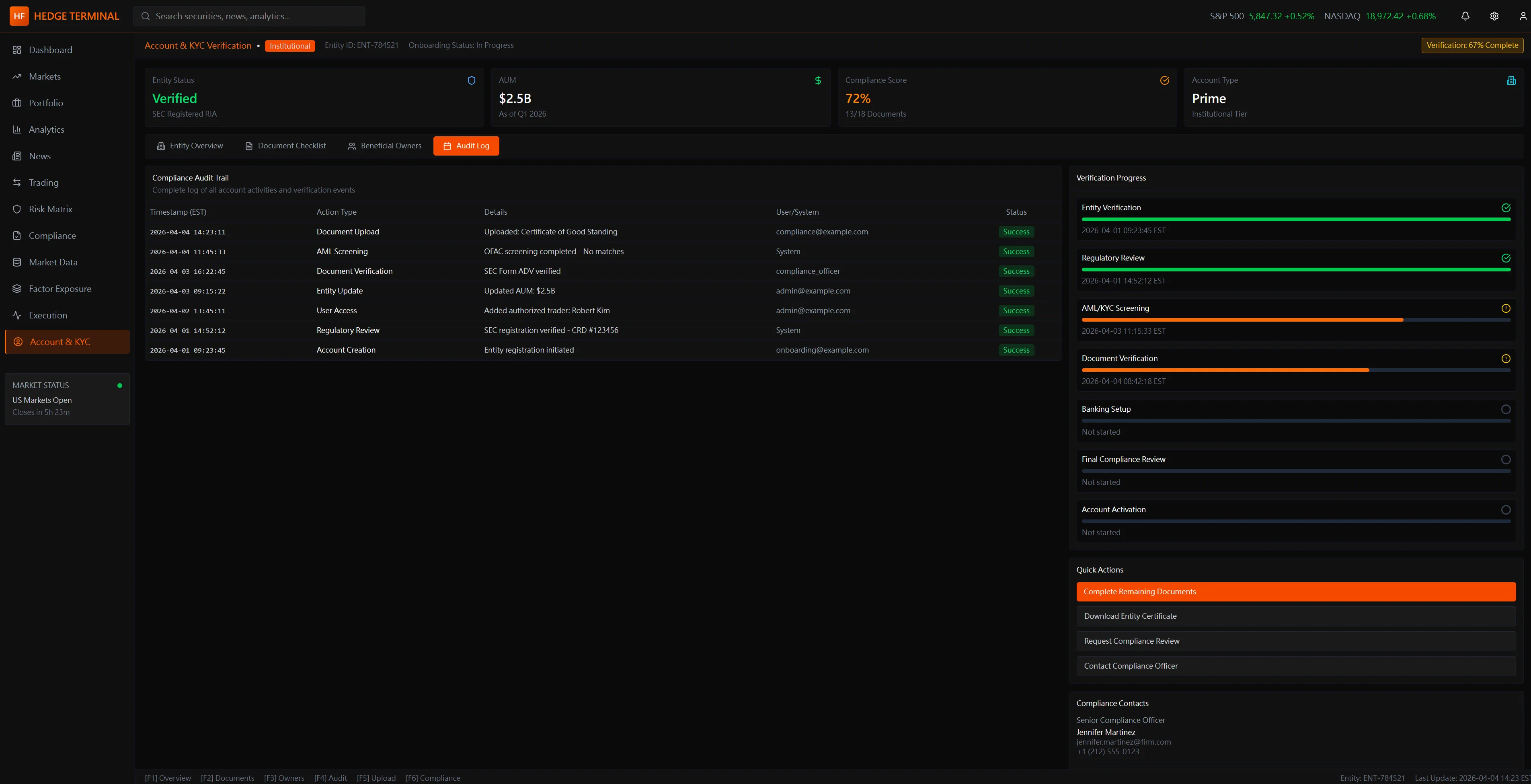

The audit trail is not a log — it's

the evidence chain. Every compliance event (account opening

authorization via LYNX, CPA accounting certification, entity system verification via

Quantum Grid S75) is timestamped with actor, document type, and status. The Document

Editor panel enables in-platform certificate scanning and update without email

attachment workflows. Designed to be forensically defensible: if a regulator pulls

the AML file, every step has a traceable record with no gaps.

6. Three Principles That Unify the System

Across all five views, three design commitments repeat consistently — each a direct inversion

of how current institutional tools are built:

Conclusions Before Evidence

Every view surfaces what the system has

concluded before presenting the data that supports it. The manager's job is to

challenge the system's synthesis — not to perform the synthesis themselves. This

inverts the default model of institutional tools, which present raw data and leave

the assembly entirely to the user.

Explainability Over Efficiency

Every AI recommendation includes a

reasoning path the manager can interrogate. When the system flags concentration risk

in AI infrastructure, it shows which positions, which exposure metrics, and which

market conditions are driving the flag. At no AUM level is "the model said so" a

complete or sufficient answer.

Decision and Action in One Space

The cost of context-switching between

analysis and execution is invisible in normal conditions and catastrophic under

stress. TradeX minimizes the number of cognitive transitions between forming a view

and acting on it — each screen connects directly to the execution pathway it

naturally leads to.

7. The Hardest Design Decision: How Much Should the AI Proactively Surface?

Every feature in Section 1 — causal maps, liquidity stress, alpha attribution, stress tests —

presupposes that the AI will surface these things automatically. But that creates

the single most difficult design tension in the entire system:

The problem:

If the AI surfaces everything it detects → alert fatigue. A

manager who receives 40 flags before 9am will stop reading them. The very system

designed to direct attention starts creating noise. Worse: when a real crisis flag

appears alongside 39 routine ones, it carries the same visual weight as the noise. The

design has failed at its core job.

Option: Full Proactive Surfacing

REJECTED

Surface

every AI-detected anomaly across all positions in real time. Maximally thorough — and

exactly why it fails. Alert fatigue sets in within days. Managers learn to ignore the

system. Trust degrades, and the AI's real signal capability is squandered.

Option: Pure Query Mode

REJECTED

AI answers

when asked, never initiates. Eliminates alert fatigue — but defeats the core

premise. A manager who must query for causal chains, liquidity stress, and

attribution provides no cognitive advantage over existing tools.

TradeX Answer: One Prioritized Signal Per View

Context

CHOSEN

Each

view surfaces exactly one AI-prioritized conclusion — the single highest-significance

signal for that view's context. A "See all detected signals" expand is available but

collapsed by default. This imposes curation on the AI: it must rank before it can

surface, which means the interface's usability depends on the quality of the ranking

model.

The trade-off accepted: A high-significance

event ranked below another signal in the same view could be missed during the first

glance. This is the cost of preventing alert fatigue. The design assumes ranking

quality; if ranking fails, curation fails. This is the open hypothesis that real-world

testing would need to validate.

8. Visual Language as Functional Communication

The TradeX visual system makes three decisions that are often dismissed as aesthetic but are

structurally load-bearing:

Deep Dark

Backgrounds (#0a0a0a range)

Not a

style trend. A fund manager may spend 12+ continuous hours in front of this

interface across multiple monitors. High-contrast bright UIs cause progressive

eye strain and increase cortisol during already-stressful sessions. Dark reduces

photonic load to the content itself — the data becomes the only light source the

eye needs to attend to. This is why professional trading terminals have been

dark since before dark mode was fashionable.

●

Orange Accent, Not

Red

Red

is reserved for loss, error, and danger in every financial interface a manager

uses. If TradeX used red as its primary accent, the color's semantic meaning

would collide with its branding function — every time the manager saw

orange-that-should-be-red, they'd experience a half-second of mis-read alarm.

Orange carries urgency and priority without the adrenaline trigger that red

produces. Under cognitive stress, the half-second saved matters.

⊞

Organized Density,

Not Reduced Density

Consumer UX often treats density as the problem — the solution is to simplify.

For expert users, density is not the problem. Control is. A fund manager wants

all the data — they simply want it organized so they can extract meaning without

assembly. TradeX doesn't reduce what's on screen; it organizes it into a

hierarchy that routes the eye from conclusion to evidence rather than from raw

number to interpretation. Density organized is not the same problem as density

reduced.

Expert Density:

The "Bloomberg Bar" Principle

For Principal roles at firms like BlackRock or Goldman, "clean design" is a

secondary requirement to Information Throughput. I architected the TradeX

grid to support 500+ data points per viewport through:

Micro-Visuals: Using cell-level sparklines and heatmaps

instead of raw text, allowing for instant pattern recognition across 80+

tickers.

Adaptive Padding: A "Power User" mode that reduces UI

chrome to <5% of screen real estate, maximizing the data-to-pixel ratio.

Information Tiering: Critical execution data (Bid/Ask/Size)

uses high-contrast typography, while historical context (1D Change/Avg Vol)

uses lower-luminance tones.

⚠️

Stateful Data

Health: The UX of "Stale Data"

In high-frequency environments, "No Data" is safer than "Old Data." I designed a

specialized state machine for data trust visualization:

Luminance Decay: Price labels automatically dim if the

heartbeat from the Liquidity Provider exceeds 250ms, signaling "stale"

status before the connection is officially lost.

Trust Indicators: A millisecond-precision "Heartbeat

Monitor" next to high-stakes execution buttons, preventing traders from

hitting "Confirm" on ghost liquidity.

Fail-Safe UI: If latency exceeds 500ms, "Market Order"

buttons transition to a warning state, requiring a manual override to

acknowledge the execution risk.

9. What I Would Test with Real Fund Managers

Intellectual honesty in concept design means knowing what you've assumed and what you've

validated. These are the three open hypotheses that real research sessions would need to

address before any of TradeX's design decisions should be treated as confirmed:

Hypothesis 1: Alert

Fatigue Threshold

TradeX surfaces one prioritized signal per view. The assumption is that one is the

right number — not zero (useless) and not many (fatigue). But what is an experienced

fund manager's actual saturation point? Does it vary by cognitive state (pre-market

vs. live event)? Does it vary by strategy type (quant vs. discretionary)?

Research method: Session

observation across three different managers, three days each. Count unprompted

signal interactions vs. ignored signals. Map ignoring patterns to time of day and

market conditions.

Hypothesis 2: Mode

Switching vs. Unified Layout

TradeX uses one visual layout across all cognitive states. The assumption is that a

well-organized interface works for both morning strategic review and live crisis

response. But State 01 and State 02 may require fundamentally different information

hierarchies — perhaps an explicit "Crisis Mode" that reconfigures the layout

entirely is worth the cognitive cost of mode-switching.

Research method: Simulated market

event during a session. Observe whether managers navigate to different views or

attempt to get everything from their current screen. Map eye-tracking (if available)

against the layout hierarchy.

Hypothesis 3: Minimum

Explainability for Execution Trust

TradeX assumes that showing a reasoning chain (not just a conclusion) is sufficient

for a manager to act on an AI recommendation without independent verification. But

the threshold may be higher than designed. At what depth of explanation does a

manager feel confident enough to execute without checking the AI's work manually?

Research method: Present identical

AI recommendations with varying levels of explainability (conclusion only / one-step

reasoning / full chain). Measure time to execution decision and rate of independent

verification behavior.

10. How This Connects to the Wider Body of Work

TradeX doesn't exist in isolation. It's the institutional-scale expression of design problems

I've been working through across multiple projects — each developing a component of the same

underlying challenge:

Competitive Analysis:Legacy

terminals, modern web platforms, AI-driven research tools — failure mode mapping

across all three categories

Cognitive Modeling:Three-state user

model (Strategic / Crisis / Narrative) derived from professional trading session

patterns

Cross-Project Research:Nova AI trust

patterns · Finlogix density architecture · TrueWorth visualization hierarchy ·

TradingAgents arXiv:2412.20138 (multi-agent trading firm architecture) ·

Fincept Terminal (37-agent investor committee in production)

Key Outcomes

Failure Mode Library:4

persistent unmet needs documented across institutional terminal category — each

mapped to a specific cognitive cost in the manager's workflow

Three-State User Model:Defined

Strategic / Crisis / Narrative cognitive states as the architectural basis for view

hierarchy — a framework applicable beyond this project

Design Tension Resolved:Alert

fatigue vs. exhaustive surfacing — one prioritized signal per view context, with

documented trade-off and open hypothesis for validation

Cross-Portfolio

Synthesis:Identified three transferable design principles

(explainability architecture, organized density, conclusions-first hierarchy)

consistent across Nova, Finlogix, TrueWorth, and TradeX

This is a research-driven design exploration, not a production product. Every decision

documents a real failure mode in existing tools and a defensible design response.

Section 9 explicitly lists what remains unvalidated — because intellectual honesty is

part of the design work.

Live Demo · Intraday Factor Attribution

Where did today's P&L actually come from?

LPs under fee pressure need real answers — not end-of-month reports. This panel decomposes intraday P&L in real time: how much is genuine alpha, how much is market beta, and which factor exposures (momentum, value, quality, low-vol, size) account for the rest. The information hierarchy puts the LP's primary question — are we generating alpha? — at the top.

Data simulated · Updates every 3 seconds · Same decomposition structure used in institutional attribution systems (Axioma, Barra)

P&L Attribution EngineBarra-style decomposition

LIVE

Total P&L

+$0.0M

+0.00%

Alpha

+$0.0M

Skill-based return

Beta

+$0.0M

Market exposure

Factor

+$0.0M

Style tilts

Contribution Waterfall

Factor Decomposition

Intraday Attribution Curve — Alpha vs Total

Total P&L

Alpha only

Gap = beta + factor exposure

Design principle: alpha is surfaced first because that is the LP's primary question. Beta and factor decomposition follow — they provide context, not the headline. When alpha is negative, the colour encoding changes immediately so the PM sees the situation before reading any number.

Live Demo · Multi-Agent Signal Consensus

When models disagree, that's the signal

Six independent agents — trend, mean-reversion, momentum, volatility regime, sentiment, macro — vote on direction. The weighted ensemble consensus is what a PM trades on. Disagreement between models flags regime uncertainty before price confirms it.

Inspired by MiroFish (multi-agent swarm prediction) · AI-Trader (agent reputation scoring) · All data simulated.

Signal Aggregation EngineSPX · S&P 500

LIVE SIM

Weighted Ensembleconfidence-weighted · 6 agents

Bullish

—

Bearish

—

Agreement

—

Regime

—

Design note: this panel surfaces agreement and disagreement equally. High model disagreement signals regime uncertainty — often more actionable than consensus. The tug-of-war bar makes conviction balance immediately readable without requiring the PM to count votes.

Portfolio Construction · Quantitative Analysis

The Efficient Frontier — where risk earns return

Markowitz mean-variance optimization underlies every serious institutional allocation decision. Each point is a portfolio of the six fund strategies. The frontier is the set of portfolios delivering maximum return for each unit of risk. The Capital Market Line (gold) stretches from the risk-free rate through the max-Sharpe portfolio — every portfolio above the line is unachievable; everything below leaves return on the table.

500 randomly sampled portfolio weights · Hover any point for details · Frontier recalculates on Resimulate

Efficient FrontierAnnualised Risk vs Return · 6-Strategy Universe

Feasible portfolios

Efficient frontier

Capital Market Line

Max Sharpe portfolio

Max Sharpe Portfolio

Risk MetricsLIVE

Strategy Allocation

What this case study evidences · and what it doesn’t

For a Senior PD or Design Lead interview panel.

This concept evidences PM-cognition design at the institutional hedge-fund tier: 11 screens

across 3 cognitive states (rapid scan / deep investigation / execution decision), 4 unmet demands

from research, 5-screen KYC flow, AI autonomy tiers framing (humans hold the commit, AI surfaces

options). Built from 4 research sources including 3 informal practitioner conversations + public

architecture analysis. Production foundations (ACY Connect FIX 4.4 institutional API)

ground the protocol literacy; the buy-side PM cognition layer is the explicit concept

extension.

What this concept deliberately does not claim. Not in production — concept

artifact, no live data feed, no real FIX execution path, no validated quant models. Not n-participant

user research — n = 3 informal practitioner conversations, supplemented by public-source

architecture analysis. No certified WCAG 2.1 AA conformance — full disclosure at the

accessibility audit

disclosure. No paired-within-subjects statistical claim — the parallel methodology

rigor for any future measured claim would follow the

Finlogix methodology

disclosure. No post-launch iteration data because there is no launch — the parallel

pattern is documented at the

ACY RG 268

iteration arc. The institutional adoption pattern (verification surface as adoption

mechanism) is documented at the

ACY Connect

political-skill note.

The disclosure register. The four 2026-05-18 field notes are the canonical voice

this concept inherits from. The TradeX Hedge Fund concept maps the PM-cognition layer; alongside

Praxis Prime (operational lifecycle) and TradeX Institutional Terminal (execution microstructure)

it completes the institutional workflow triple under one disclosure discipline.

Every problem we solve for clients has multiple valid approaches — different costs, different ROI, different risk profiles. These threads show how the approach on this page compares to others in the portfolio.

Thread

Concentration, Risk & Agents

Portfolio-level math primitives — HHI, beta, VaR, regime — rendered into UI defaults and AI-assisted decision surfaces.

Index Weights · SPX + NDXConcentration math exposedLow eng cost · 503+101 slices · HHI 230.6 / 638.2

Macro Signal NetworkRegime classifier feeding routingLow eng cost · 4 prints → 14 surfaces