Aureus

UHNW Private-Banking Fiduciary Logic, Translated for Retail

Aureus is a self-initiated B2C concept that brings institutional-grade fiduciary discipline to retail wealth-accumulation. Four AI modules, 31 mobile screens, five named regulatory anchors, a working live React prototype. Modelled outcomes, not A/B-tested at retail scale. This page is the five-minute senior-PD read; the comprehensive 6,000-word research record lives at project-aureus.html.

In 60 seconds.

Aureus translates UHNW private-banking fiduciary logic into a B2C mobile experience. Four AI modules, 31 screens, a working prototype. The thesis: the retail-fintech category serves users who are anxious about spending. Aureus serves the user who has stopped being anxious and is now asking for fiduciary-grade tools.

What's built

- 31 mobile screens · 4 AI modules · live React prototype at edwson.com/Aureus/

- Editorial light theme: bone white, oatmeal, Aureus gold — deliberate departure from institutional dark-mode neon

- 10-step KYC + AML onboarding flow citing FinCEN CDD 31 CFR § 1020.220 + FATF Rec 10

- Original IP, zero client overlap, working artefact not Figma mockup

What's deliberately not built

- No gamification, no streaks, no badges

- No crypto tab, no social feed, no share-your-gains

- No auto-trade execution — the sign-off is the entire architectural commitment

- No chatbot personality, no wealth-coach tone, no behavioural-nudge growth-hack

Status & honesty disclosure

- Self-initiated concept, not a client engagement

- Modelled lift figures (∼2× Velocity, ∼$1.15M projected wealth) are derived from behavioural-economics literature + ACY production patterns — not A/B-tested at retail scale

- Provenance line under each module in the comprehensive page labels production-derived vs. concept extension explicitly

- Read time: ~4 min here · ~12 min comprehensive

Private banking for the 1%. Cold budgeting apps for everyone else.

UHNW clients of J.P. Morgan Private Bank, UBS Wealth, and Pictet receive personalised risk modelling, liquidity stress tests, multi-generational tax planning, and a relationship manager who absorbs the analyst load while the client keeps the fiduciary sign-off. The retail investor receives a budgeting app that scolds them for buying coffee, or a robo-advisor that optimises a black-box portfolio they cannot see inside. The structural gap is not the asset class — it is the fiduciary logic. Aureus closes that gap by compressing four institutional patterns into three buttons and a single curve, without losing the regulatory rigour underneath.

Each module is one institutional pattern, compressed.

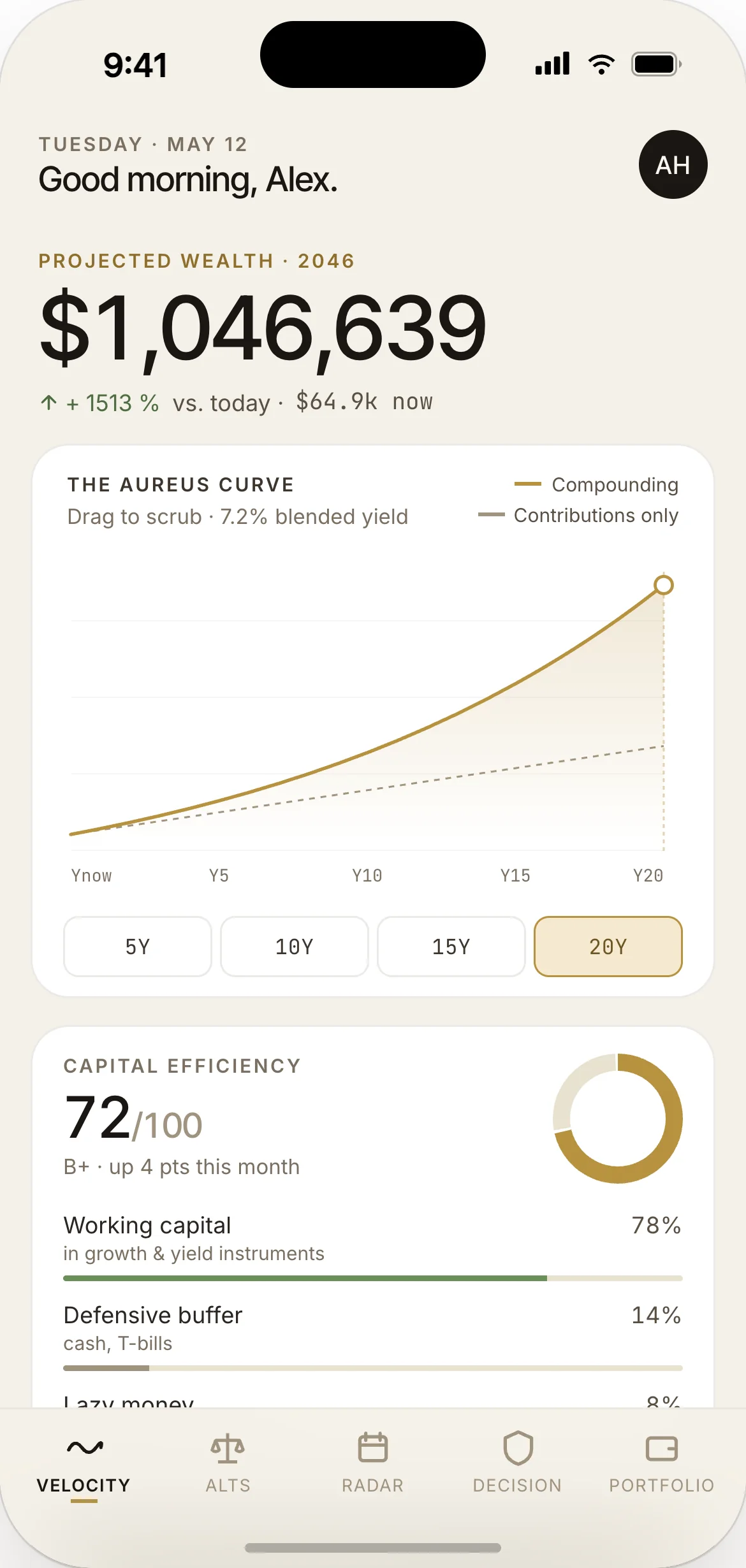

Module 01 — Velocity Dashboard

A projected wealth curve with explicit time-horizon controls (5 / 10 / 15 / 20 years), starting capital, monthly contribution, and blended yield. Replaces the budgeting app's "you spent $42 on Uber" with "your $42,000 in checking is costing you $1,148,200 over twenty years." Production-derived: the curve mechanic is ported from the UHNW relationship-manager quarterly cash-flow forecast tool I observed at ACY.

Module 02 — Alternative Finder

The opportunity-cost lens. User selects an amount and frequency; the AI projects 5 / 10 / 20-year compounding deltas across three preset risk profiles. Pure concept extension from behavioural-economics literature on hyperbolic discounting (Kahneman, Thaler) — the institutional version exists in PM strategy tools but is rarely surfaced to retail.

Module 03 — Event Radar

Forward-look at upcoming financial events (property tax, year-end RMD, RSU vest, distributor invoice cycle). Production-derived from UHNW RM cash-flow calendar; the retail extension automates the surfacing where the institutional version relies on the relationship manager keeping the timeline in their head.

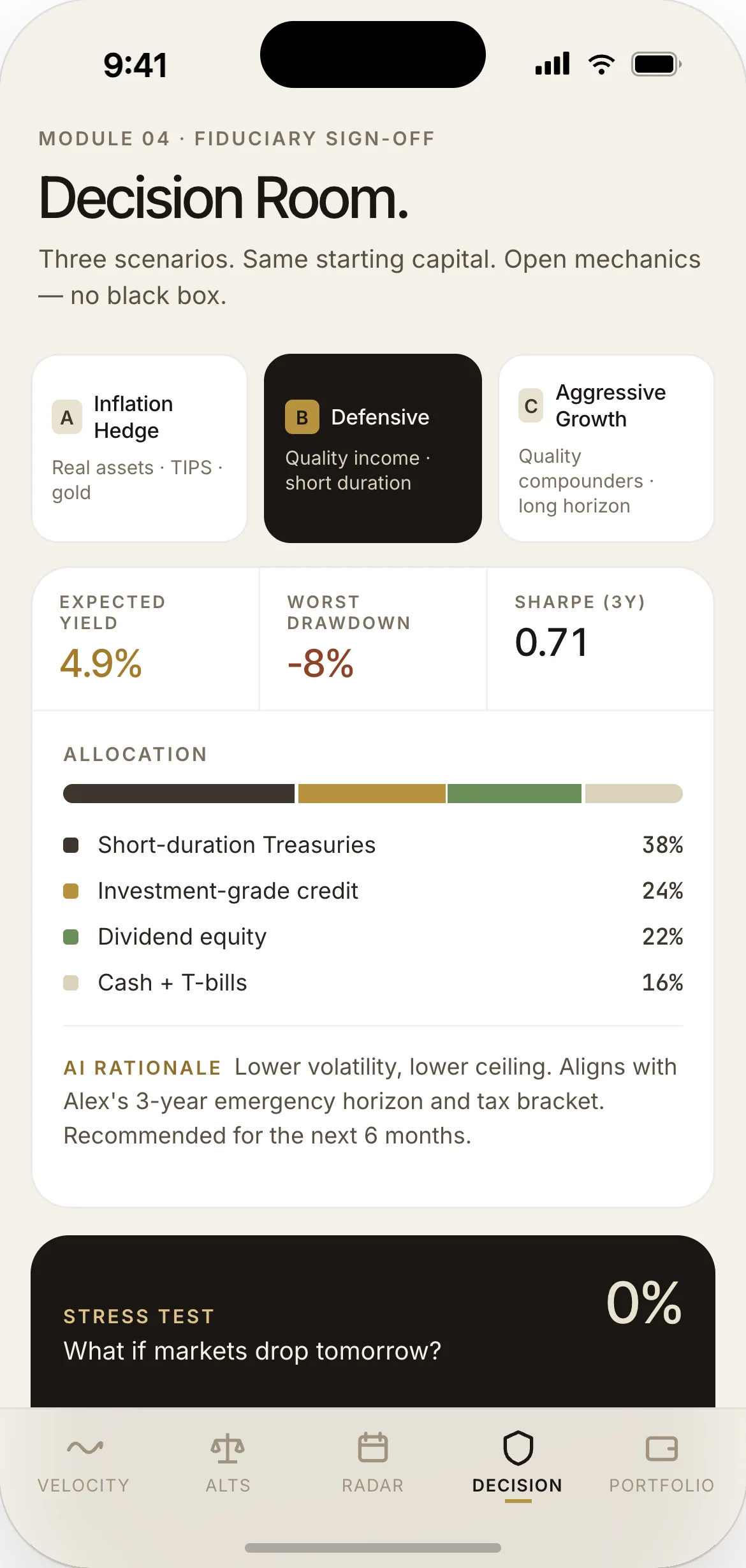

Module 04 — Fiduciary Decision Room

Where the human signs off. Every AI recommendation enters here as an option, not an execution. Typed confirmation anchored to SEC Reg BI Care Obligation 17 CFR § 240.15l-1(a)(2)(ii). The design move is to put the regulatory citation on the user's screen, not behind a legal disclaimer the user never reads. Production-derived from the institutional sign-off pattern; the retail translation is the typed-name commitment surface.

Each regulation maps to one UI guardrail.

SEC Reg BI Care Obligation (17 CFR § 240.15l-1(a)(2)(ii)) drives the Decision Room typed-confirmation pattern. SEC Reg BI Conflict of Interest (17 CFR § 240.15l-1(a)(2)(iv)) drives the "Why this recommendation" drawer on every AI proposal. FINRA Rule 2111 Suitability gates the risk quiz before bank-link unlocks Decision Room defaults. SEC Rule 17a-4 (17 CFR § 240.17a-4(f)) drives the SHA-256-chained Activity Log so every AI suggestion and every human sign-off is hash-sealed for the seven-year retention window. SR 11-7 Model Risk drives the user-facing Stress-Test Slider that exposes the model to the user, not just to the regulator — the slider is the effective-challenge surface the regulator requires, ported into the consumer product.

Five categories deliberately cut.

No gamification (streaks, badges, levels). No crypto tab. No social or share-your-gains feed. No auto-trade execution — the sign-off is the entire thesis. No chatbot personality or wealth-coach tone. Each cut serves the fiduciary register: adding gamification creates a behavioural conflict with the deliberation register required by SEC Reg BI Care Obligation; adding social features creates regulatory exposure under FINRA testimonial rules; adding auto-trade nullifies the sign-off premise. The discipline is that the system says no to features that look great in isolation but undermine the regulatory register.

Where each pattern came from, and where it didn't.

Patterns labelled PRODUCTION-DERIVED came from ACY's CDD/EDD sequence (10-step KYC + AML flow), Finlogix's UHNW RM quarterly cash-flow forecast, Xanthos's typed sign-off, or the Stress-Test slider pattern from SR 11-7 model-risk governance. Patterns labelled CONCEPT EXTENSION are extrapolated from behavioural-economics literature and have not been A/B-tested at retail scale. The 65–75% completion lift cited for transparent KYC is FinCEN public data, not measured on this prototype. Every claim on the comprehensive page carries the label. If a number is on this page, it is either externally citable or explicitly labelled as modelled.

For a Senior PD or Design Lead interview panel.

Regulation cited by section number, not by reference. Five concrete UI guardrails each tied to a specific regulatory clause. Concept work labelled as concept, never conflated with shipped production. Editorial restraint visible in the five deliberately-not-built categories. Fiduciary AI framing — humans hold the commit, AI surfaces options — consistent with the SR 11-7 effective-challenge pattern and the sister case study Double-Blind. Original IP, no client overlap. Working live React prototype, not Figma mockups. The Aureus visual departure (editorial light, bone white, gold) is a deliberate signal that retail fiduciary tooling does not have to mimic the institutional terminal aesthetic. This concept demonstrates the senior register without inflating its evidentiary weight beyond what a concept can carry.